Sabitlenmiş Tweet

Aurea

131 posts

Aurea

@AureaHub

🔗 Bridging Banking, Crypto & AI-powered DeFi ||🤖 All in one seamless app||🏦 Building the world’s first meta bank 🌍 Milano |🇮🇹 Italy

Italy Katılım Şubat 2023

68 Takip Edilen28 Takipçiler

7/7 The wallet of the future doesn't just hold value; it creates it. 🌊

Turn your financial platform into a productive ecosystem with Aurea. 🚀 Explore the vaults: aureahub.com

English

1/7 Is your client's capital just sitting there? 💤 In the digital age, idle money is a wasted opportunity.

Introducing Aurea’s Passive Yield Vaults: the engine that transforms any wallet into a high-performance financial asset. 🏦💸 #DeFi #PassiveIncome #AureaHub

English

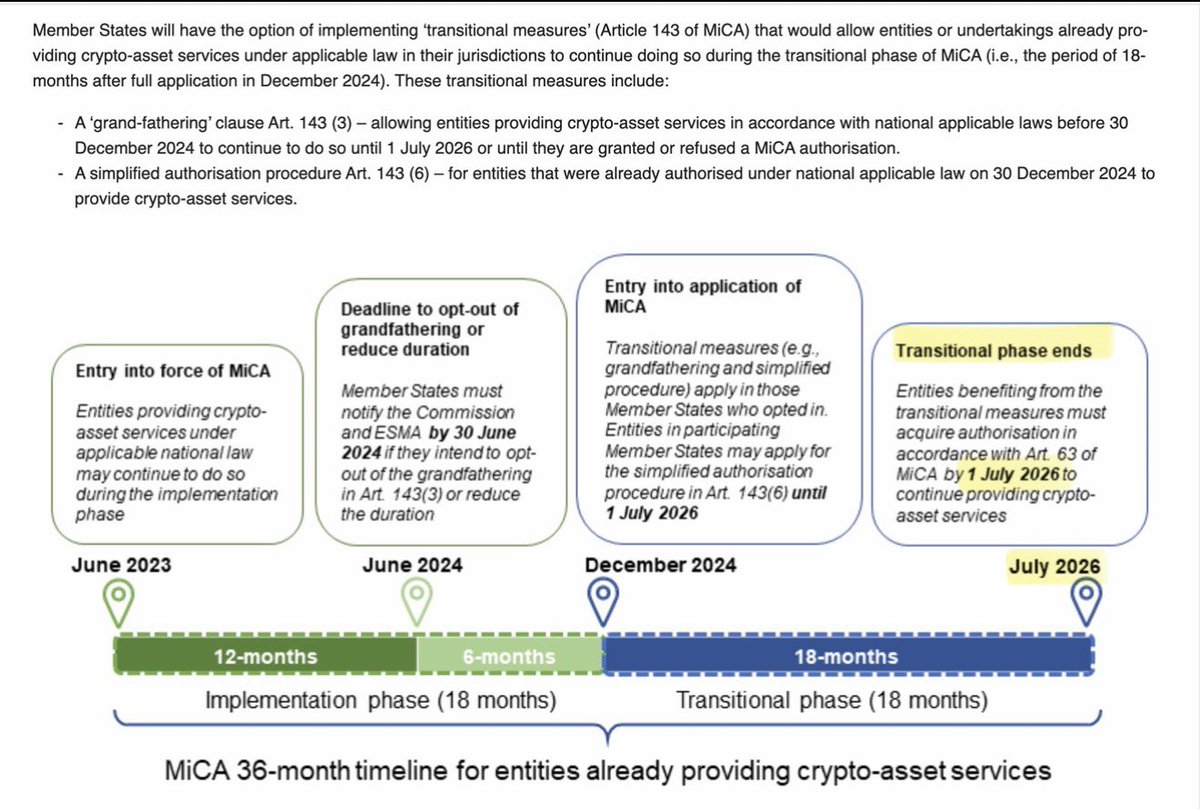

@SternDrewCrypto The invisible backbone thesis applies beyond Ripple.

At @AureaHub we're building that same layer for EU banks & fintechs: MiCA-compliant, tokenized RWAs, stablecoin flows — white-label, single API, live in 1–3 months.

The winners own the rails. 🏗️

English

🇨🇭 Follow the money trail. Ripple's Swiss partner AMINA Bank is burrowing DEEP into Europe's tokenized future.

First bank globally to custody and trade $RLUSD. Now first in Europe running full Ripple Payments for instant cross-border fiat-stablecoin flows.

But here is the real red pill: AMINA is cozy in the Web3 Alliance and partnering directly with 21X. That is the EU's VERY FIRST fully regulated DLT Trading & Settlement System (DLT TSS). On-chain order books, tokenized securities, atomic settlement, BaFin/ESMA/ECB blessed.

Coincidence? Or are we watching the slow merge of Ripple's XRPL/RLUSD rails straight into Europe's official tokenized capital markets infrastructure?

Ripple is positioning to become the invisible backbone of regulated tokenization in the EU. When 21X + AMINA + RLUSD connect for real (liquidity? settlement? bridging?), the old SWIFT dinosaurs are toast.

English

✨ Why DeFi Yield Became My Job!

Still farming double-digit APYs on my dry powder. So DeFi yield isn’t gone, it just stopped being a free lunch for anyone willing to click 3 buttons.

Short-term Treasuries are printing ~3.5-3.7% rn. Makes sense why normie sees 2% on vanilla Aave USDC and thinks DeFi is cooked. But they don’t see this:

– Ethereum still anchors ~$54B TVL across DeFi

– Pendle has 200+ pools, ~6–7% avg APY, ~$2.2B TVL

– Basis trades have been hovering ~4.5-6% annualized even in choppy conditions

Yield now is just fragmented across tokenized yield markets, basis legs, PT/YT splits, LSD + options stacks, credit vaults, and RWAs.

Most people can click “supply USDC.” Very few can:

– Split yield-bearing assets into PT/YT

– Loop PT as collateral

– Manage liquidation bands

– Avoid MEV leakage

– Simulate unwind paths under stress

TradFi solved this complexity with productization. Hedge funds → structured notes → robo-advisors.

DeFi is about to go through the same arc.

– Yearn sharing performance fees with strategists

– Ribbon packaging options yield

– @pendle_fi monetizing yield trading with revenue routed to vePENDLE

– now @Infinit_Labs helping users multi-farm with a prompt

It's pretty obvious that yield intents are the next meta.

Instead of “deposit here, borrow there, bridge here, stake there,” users are going to express “give me 6–8% stable yield with low liquidation risk.”

To get there, devs have to build compilers, simulation engines, risk scoring, deterministic execution, and post-trade monitors, not just basic vault code.

The real DeFi yield revolution is productization, and the biggest winners are the platforms that own the flow.

They’ll be the layers that can:

– Simulate and preview risk deterministically

– Prove execution quality

– Manage unwind paths

– Attract top strategy creators

– Lock in wallet-level distribution

But when strategy execution goes mainstream, trades get crowded. Millions of users unknowingly running the exact same leverage loop leads to synchronized liquidation cascades.

Another moat is trust and safety at scale: deterministic construction, monitoring, MEV minimization, and actually surviving stress without socializing losses.

In that endgame, the winners fall into a few clear buckets:

→ Base primitives (deep liquidity + structurally necessary). Every strategy pays them a tax.

→ Venues with explicit value capture to holders

→ Risk, analytics, and parameter tooling that institutions and agents rely on

→ Whoever owns the user’s default earn button becomes the toll booth (wallets, CEXs, neobanks)

DeFi yield became a job. The next wave of winners are the ones who turn it back into a button.

We are going to see this yield accessibility shift play out very soon.

English

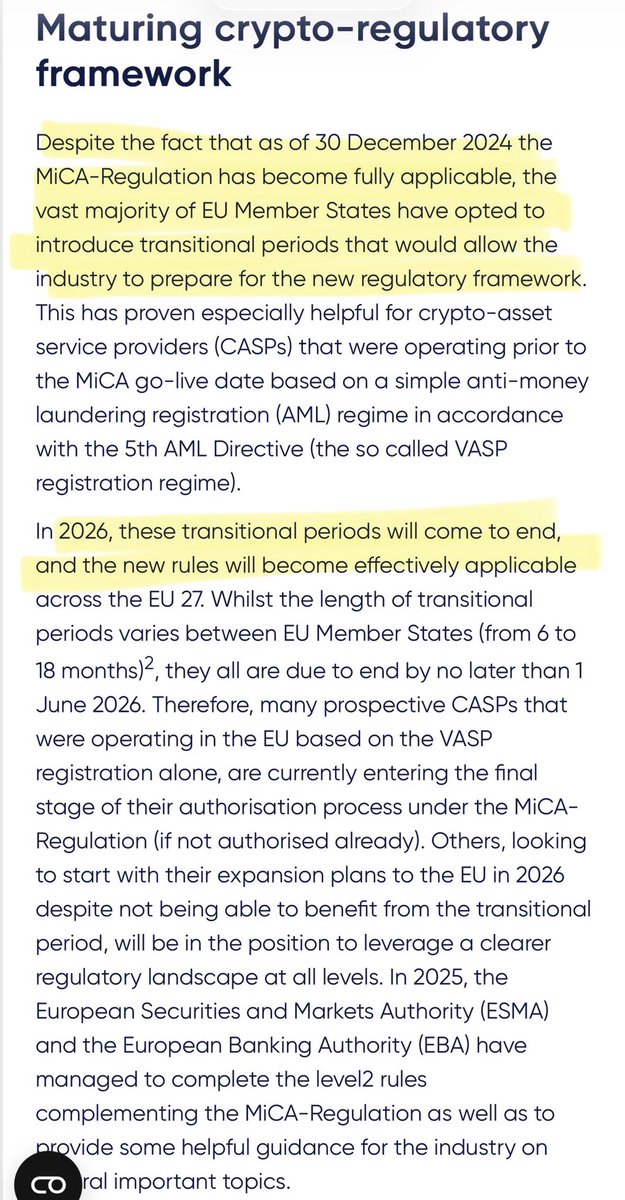

@thecryptobasic Banks finally admitting legacy rails are broken 🏦

@AureaHub built the alternative: white-label BaaS + WaaS infra replacing slow, costly intermediaries.

Single API, multi-currency, cross-border, MiCA-compliant. 1–3 months to integrate.

The shift is happening ⚡

English

Deutsche Bank Taps #Ripple to Revolutionize Global Payments.

Traditional cross-border payments are facing criticisms for being slow, costly, and heavily dependent on intermediaries.

Deutsche Bank is signaling a decisive shift away from that model by deepening its use of blockchain infrastructure built within the Ripple payment system.

Additionally, Deutsche Bank is modernizing processes that historically relied on legacy networks such as SWIFT

English

@swiftcommunity The future of cross-border payments is programmable, tokenized and compliant 🌍

@AureaHub already gives banks & fintechs white-label infra to do exactly this — single API, multi-currency, cross-border + tokenized value settlement.

EU-native, MiCA-compliant. The rails exist 🔗

English

BNY is among the global institutions collaborating with us to help design our blockchain‑based ledger for cross‑border payments and tokenised value.

Through close collaboration, we’re building a more connected, secure and interoperable financial ecosystem.

English

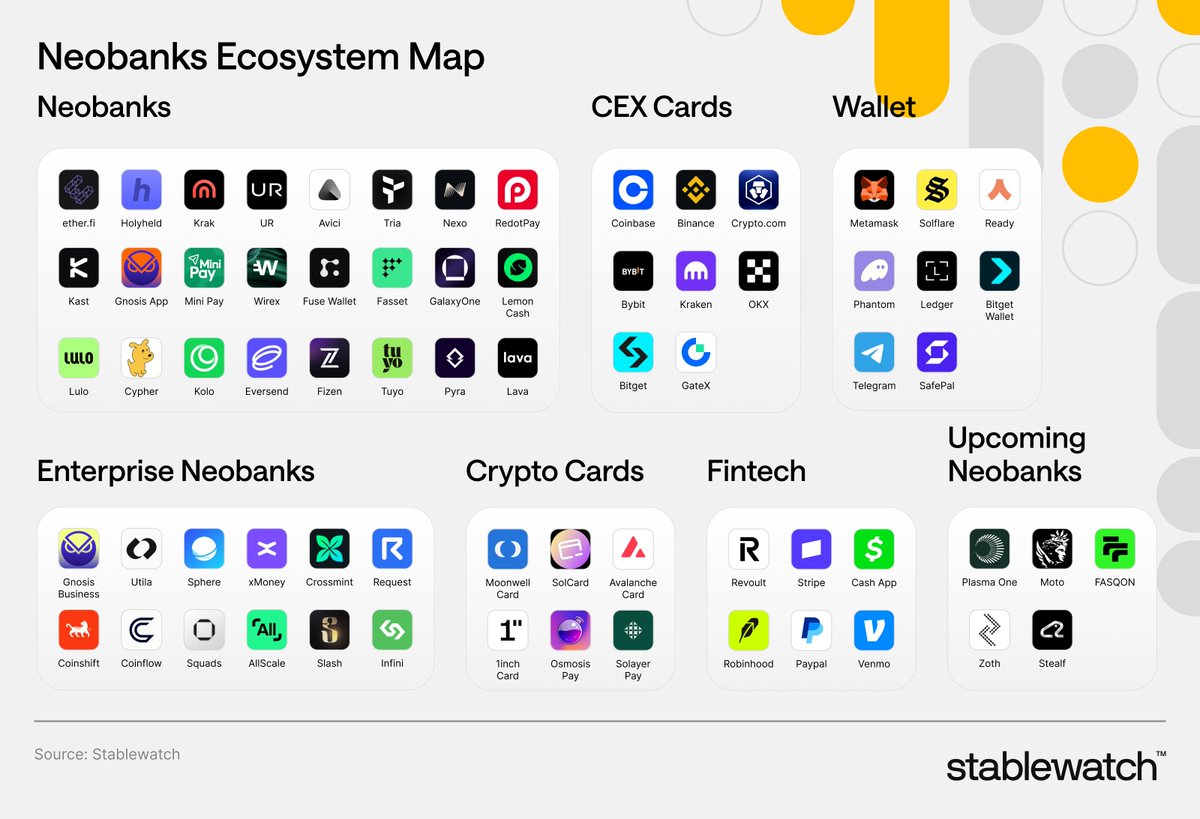

@stablewatchHQ Great map 🗺️ Notice the "Enterprise Neobanks" section is still tiny — that's the biggest opportunity.

@AureaHub is exactly that: white-label BaaS + WaaS infra for banks & fintechs.

Single API, 1–3 months to go live. EU-native, MiCA-compliant 🚀

English

@tokenterminal RWA tokenization is crossing the $300B mark — and the infra layer is now critical 🏗️

@AureaHub gives banks & fintechs white-label tools to issue, settle and manage tokenized RWAs natively.

EU-native, MiCA-compliant, single API. The next winner is whoever owns the rails 🔗

English

🆕🥇 The issuers & chains that are actually winning in RWAs 👇

🏦📈 Leading issuers: Tether, Maple Finance, & Ondo Finance

▪️ Stablecoins are at an all-time high of $307.2b; Tether is the leading issuer of stablecoins, with 61.1% market share.

▪️ Tokenized funds are at an all-time high of $14.4b; Maple Finance is the leading issuer of tokenized funds, with 14.8% market share.

▪️ Tokenized commodities are at an all-time high of $4.4b; Tether is the leading issuer of tokenized commodities, with 56.5% market share.

▪️ Tokenized stocks are at an all-time high of $441.2m; Ondo Finance is the leading issuer of tokenized stocks, with 54.4% market share.

⛓️📈 Leading chains: Ethereum & Solana

▪️ Stablecoins are at an all-time high of $307.2b; Ethereum is the leading chain for stablecoins, with 61.5% market share.

▪️ Tokenized funds are at an all-time high of $14.4b; Ethereum is the leading chain for tokenized funds, with 53.3% market share.

▪️ Tokenized commodities are at an all-time high of $4.4b; Ethereum is the leading chain for tokenized commodities, with 98.7% market share.

▪️ Tokenized stocks are at an all-time high of $441.2m; Solana is the leading chain for tokenized stocks, with 38.8% market share.

English

@Cryptic_Web3 @swiftcommunity @BNYglobal The institutional adoption of tokenized assets is accelerating fast 🏦⛓️

At @AureaHub we already give banks & fintechs the infra to settle tokenized RWA + cross-border payments via a single white-label API.

EU-native, MiCA-compliant. The rails are ready 🚀

English

🚨NEWS: @swiftcommunity and @BNYglobal are developing a blockchain-based ledger to upgrade cross-border payments and support settlement of tokenized assets within regulated financial markets.

English

@crowdfundinside Exactly why we built @AureaHub — white-label BaaS + WaaS infra for banks & fintechs.

Single API, 1–3 months time-to-market. EU-native, MiCA-compliant, MPC-secured.

24+ clients, €2Bn volumes managed 🚀

English

Fintech focused Banking as a Service Is Reshaping Bank Stability and Consumer Expectations : Analysis crowdfundinsider.com/2026/02/263387…

English

@richardchen39 Building exactly in the "uncrowded" lane 👀

@AureaHub integrates non-USD stablecoins (e.g. EURY) + onchain FX + programmable credit natively into banks via white-label API.

EU-native, MiCA-compliant. Happy to connect 🔗

English

Overcrowded stablecoin opportunities:

- Consumer neobank

- Stablecoin orchestration

- Merchant accounts

Uncrowded stablecoin opportunities:

- Non-USD stablecoins

- Onchain FX

- Programmable credit (e.g. trade financing)

English

@brian_armstrong This is exactly the gap we're closing at @AureaHub 🏦

We give banks & fintechs the infra to embed DeFi yield natively — white-label, single API, 1–3 months to go live.

EU-native, MiCA-compliant. The "DeFi without complexity" layer for institutions 🔗

English

Now you can lend your USDC and earn more (up to 10.8% currently).

It’s simple to use, and gives users the benefits of DeFi without the complexity. Rolling out now in multiple countries, including the US (ex. NY).

English