amanda | ayoki

1.1K posts

amanda | ayoki

@AyokiRoll

survived 4 filler arcs. main plot loading ✨ Previously: @sushiswap / @shoyu_nft, @acrossprotocol

Katılım Mart 2021

474 Takip Edilen2.5K Takipçiler

@pvmihalache @LevxApp veryyy well haha very well rested, ready to lock back in

hope you've been ok PVM 🤠

English

🤯

new delta neutral vaults on hyperliquid

~30% APY (even in the bear... wtf)

Congrats @LevxApp 🤠

xDFi@xd_protocol

xDFi Genesis Phase Deposits are now LIVE! We’ve just opened up the 100K cap for xDFi deposits.

English

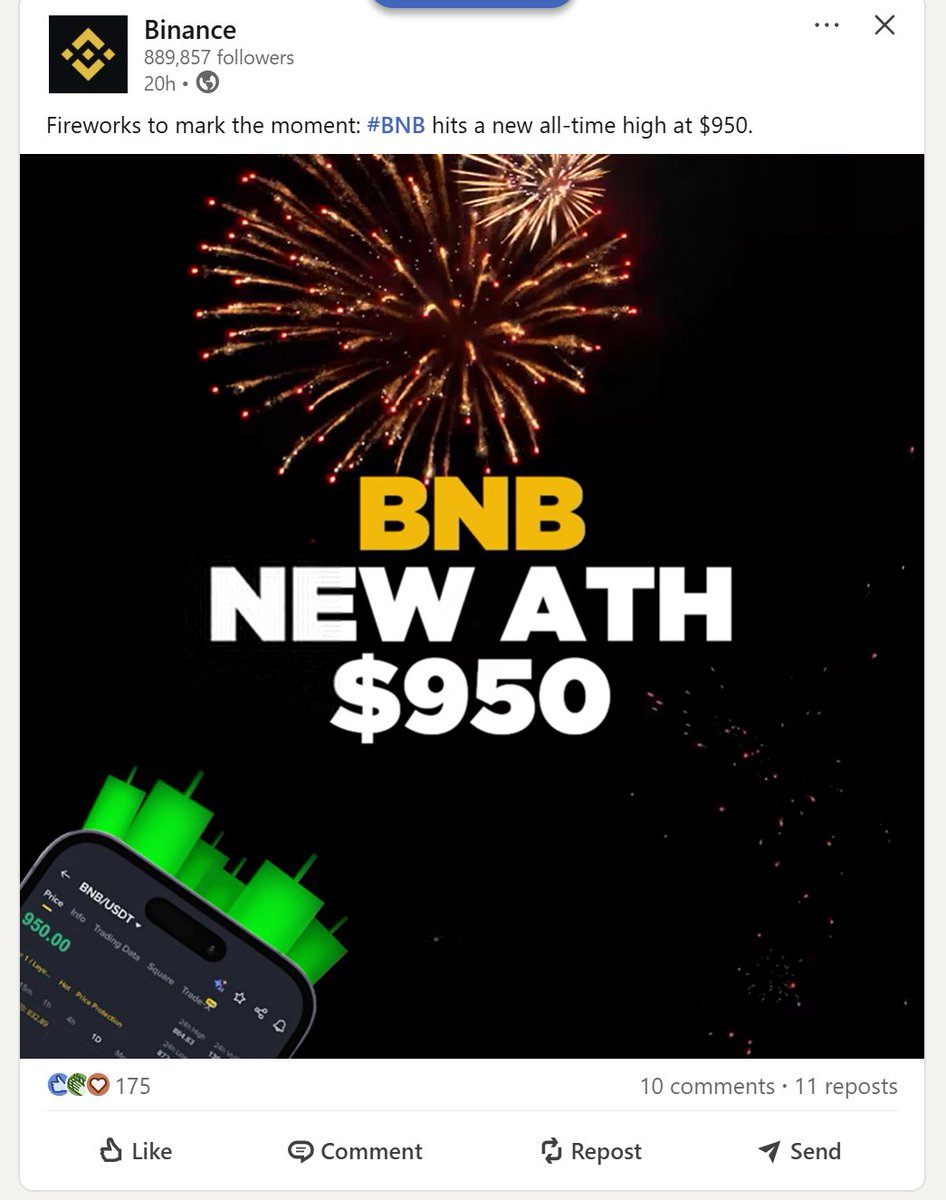

wait, so companies can post about price now? or is this a linkedin only thing?

English

@mrcampbell @ydanwashere tell me about it!

good on you aydan 👏

English

Few years back I was fighting to get @ydanwashere on the team at UMA because I could see how much potential he had.

Today it is very, very cool to see him making stuff like this.

UMA@UMAprotocol

What is the truth?

English

English

Huge news.

Excited to announce that I've joined @Sei_Labs as technical marketing lead.

The job is simple: help @jayendra_jog & the incredible research and engineering teams to ship groundbreaking blockchain tech.

English

English

Back in Japan for @WebX_Asia after some time. A few takeaways:

-Queues to enter were over 3 hours. Attendance looked almost 50 percent higher than last year. Unlike many conferences where the focus is networking, people here were glued to the sessions. You can feel the retail hunger to learn.

-On policy, the Prime Minister and two ministers showed up. Clear signal that Japan wants to position itself as East Asia’s crypto hub. The tax shift from 55 percent misc to 20 percent unified financial rate will unlock a massive retail market.

-Japan also has deep roots in gaming and IP, along with strong KOL influence and community-driven tokens like ADA and XRP. With tax reforms, this potential could be amplified further.

- Also caught up with old friends from @skylandvc, one of the few early-stage investors active in Japan. Early-stage capital here is still relatively scarce, but with regulatory improvements, I expect to see more quality founders emerging from Japan.

Japan feels truly different this time. I expect more global projects to leverage its retail base as the wedge into global growth.

English

Always great coming back to Taiwan. See you at Taipei Blockchain Week. 🇹🇼

English

TBW 2025 is kicking off!

so excited not only for the main conference, but also for the side events, including a Taipei tour! @TaipeiWeek

English

@SOCKETProtocol (chain abstraction protocol, chain abstraction protocol)

English

As of last year, we've been heads down building the SOCKET chain abstraction protocol.

Time to provide an update on where we stand and why we're building a chain abstraction protocol👇

English

this is giving crypto conference speaker list vibes

90% is sorry, who?

ZachXBT@zachxbt

NEW LEAK: Price sheet of 200+ crypto influencers and their wallet addresses from a project they were recently contacted by to promote. From 160+ accounts who accepted the deal I only saw <5 accounts actually disclose the promotional posts as an advertisement.

English

I want to extend the discussion to the settlement and clearing behind expiring futures

Keone’s thread emphasizes that expiring futures are superior to perpetuals, especially for Occasionally Priced Assets (OPAs, such as stocks or commodities). The expiring mechanism requires cash settlement at expiry, which in crypto relies on on-chain settlement and clearing: clearing involves trade confirmation and risk management, while settlement is the actual transfer of assets. Keone mentions that “expiry is an elegant way to establish the relationship between futures and the underlying asset,” implying the use of on-chain smart contracts to handle automatic rollover and cash settlement (e.g., via oracles for price feeds)

The key point is that on-chain settlement enables decentralized futures for OPAs, avoiding centralized clearing like in TradFi (e.g., CME), but requires high-performance chains (like Monad) to support order books and risk computation. It highlights that clearing/settlement in crypto is blockchain-controlled, unlike traditional systems—Keone’s perspective paves the way for such mechanisms

Why is on-chain settlement important?

On-chain settlement is critical in crypto futures/derivatives because it enables instant, transparent, and automated processing, improving efficiency. It allows near-instant trading, faster than traditional derivatives, with blockchain records enhancing transparency and reducing fraud. By combining digital assets and smart contracts, it can reshape clearing/settlement, eliminating systemic risks such as counterparty default. For developers/traders: this unlocks real-world assets (e.g., OPAs) on-chain, enables permissionless markets (as Keone described, “an exchange for everything”), and supports leveraged trading. It shows that tokenization transforms collateral management in derivatives clearing, offering 24/7 global access and censorship resistance

On-chain settlement and clearing represent a major market opportunity I discussed years ago with Chris Yu, founder of @SignalPlus_Web3 (whose team came from Goldman Sachs’ largest futures and derivatives trading desk in Hong Kong), when I invested. However, due to significant implementation challenges, related projects never officially launched. Now, with Monad’s high TPS and reliable oracles (e.g., Chainlink), starting with prototype testing could make this feasible

Key challenges for builders pursuing this:

While on-chain settlement has great potential, it faces multiple hurdles:

- Technical challenges: network congestion causing delays; oracle risks (e.g., price manipulation; Keone noted that funding rates are error-prone); hybrid off-chain relay + on-chain settlement architecture requiring precise pricing to prevent amplified losses from leverage

- Regulatory challenges: complex KYC/AML requirements; regulatory uncertainty in DeFi, which may lead to project shutdowns

- Liquidity and risk management: instant settlement makes secured financing difficult; liquidation requires circuit breakers, which are tricky on-chain

- Others: data reliability (on-chain vs. off-chain); high gas costs affecting small-value settlements

Keone Hon@keoneHD

Occasionally Priced Assets and Futures Markets Futures markets are better than perpetuals for many use cases, but nobody in crypto realizes it. There is a massive opportunity for someone to build an Exchange for Everything, powered by futures settlement. Crypto participants are primed to think that perpetuals are the only way to create a delta-one (i.e. linear-exposure) derivatives market. However, for most products that lack 24/7 pricing -- and more generally for any Occasionally Priced Assets -- expiring futures are actually a better fit. Combining this with order books on a high-performance blockchain will produce a future killer product. Background Perpetuals markets generally require 24/7 pricing data in order to implement the funding rate mechanism which keeps the perpetual future tracking the underlying asset. In the funding rate mechanism, the perpetual's price is compared to the spot price and, if this deviation is systematically positive (negative), longs (shorts) pay shorts (longs). Although elegant, this mechanism requires continuous pricing. It is also subject to errors in measurement - for example, there are well-documented cases of traders making tiny trades in order to bias funding rates. Meanwhile, traditional finance is dominated by futures markets. Futures track spot prices because futures positions ultimately expire, at which point a short position must deliver the underlying asset (or an equivalent amount of cash) to a long position. Expiry is an elegant means of creating a relationship between the futures and the underlying. If the futures price deviates too much, an arbitrageur will put on a position that fades the deviation. For example, if the futures price is too high, the arbitrageur will go short the future and long spot. The arbitrageur can then wait for it to converge, or worst case wait until expiration. The expiration mechanism is what holds futures prices in line with spot prices. In practice, very few positions are actually held into expiration and delivered, but the threat of it is what creates the linkage to the value of the underlying asset. Why crypto derivatives are mostly perpetuals Crypto participants are hard-wired to think that perpetuals are the only kind of derivative that works in crypto. We all tend to imitate what they know, which in the case of crypto is perpetual futures. And perpetual futures do make sense for cryptoassets because there is a plethora of spot data to power the funding rate mechanism. But one of the benefits of crypto is that it enables the creation of permissionless markets. It would be silly if the only permissionless markets that can get created are markets on data that already is crypto-native. Expiring futures allow financial markets to extend themselves to trade completely new products. In TradFi, for many asset classes, such as corn, wheat, lean hogs, crude oil, gasoline, or natural gas, futures are the only liquid market. Each of those markets was bootstrapped from basically nothing using the expiration mechanism. Occasionally Priced Assets I would like to advocate for another class of assets, which I'll call Occasionally Priced Assets (OPAs). Many assets are OPAs. Physical commodities are OPAs. Equities are OPAs. In some sense, the topics of most prediction markets are OPAs. Anything that has a price occasionally-but-not-always is an OPA. OPAs fit most naturally as expiring futures. An OPA only needs the price at expiration, at which point it can be cash-settled. Futures are the lowest-friction way of bringing all Occasionally Priced Assets, including major real-world assets like equities and commodities, on chain. What about expiry management? We can borrow lessons from traditional finance. Futures exchanges list calendar spread ("roll") contracts that represent a position of +1 (near calendar month), -1 (far calendar month). Anyone with a long (short) position in the near month sells (buys) a calendar spread position to convert the position into a long (short) position in the far month. Instructions to auto-roll could be encoded in a smart contract. Managing open interest across calendar expiries as an exchange may sound daunting, but in practice it's a known problem. What about margin? Risk management is one of the biggest jobs for any exchange. This is true regardless of whether or not exchange assets have external data sources to mark to, but it is made more clear when a market can only be marked to itself. As an exchange operator, you need to know the max % that any of the assets may move in one day. Margin limits are set accordingly. For example, on CME, if corn prices are expected to not change by one day by more than 10%, then a roughly 10:1 margin is allowed. In TradFi, exchanges also implement circuit breakers to temporarily halt trading if price deviates from the start-of-day price by more than expected. This gives traders time to reconsider or add margin. As with the calendar spread problem, we can lean on TradFi for inspiration. Order books Order books are the intuitive mechanism for liquidity providers to express their markets. AMMs require a liquidity provider who doesn’t mind being picked off, which requires high emission-based incentives for liquidity providers, or (in the case of memecoins) requires part of the genesis supply of the memecoin itself to be locked into the AMM. Order books allow for sustainable liquidity provision, where liquidity providers quote precisely according to their fair values, earning spread from the deviation between fair value and their quotes. Order books also force liquidity providers to compete the spread down, thus leading to better markets for takers. Order books especially fit well for futures. Futures prices drift over time as time-to-expiration shortens, and it’s most intuitive for the liquidity provider to simply price that accordingly, rather than trying to encode it into a complicated AMM formula. More generally, derivatives need extreme precision in pricing, since leverage magnifies the impact of gains or losses. Conclusion Crypto offers many benefits - borderless access to tools for personal finance, and censorship-resistant asset ledgers. However, these tools are not being utilized at all to their full potential if the only investable assets are other cryptoassets. Anything that has an occasional price is a great target for creation as a futures market. In some senses, a futures market can be thought of as a prediction market with leverage. As someone who, in a prior life, traded between 10 and 50 billion dollars of daily notional in futures volumes, I can attest that futures contracts unlock immense efficiencies, and that details like the expiration were only top of mind a few days per year. With futures, anything that can be eventually priced can be traded now. Whoever solves the challenges introduced by expiring futures will capture a huge opportunity.

English

web3 marketers farming the ‘crypto marketing bad’ meta so well that they might just market themselves out of a job

English

記得來解10週年任務、簽到

Test Your DeFi Summer 2020 Knowledge

etherscan.io/points

1. Which protocol's rebase function mistakenly omitted a division of 10^18, causing a massive over-mint of governance tokens into the treasury?

Yam Finance

2. Which DeFi project had its governance token contract deployed early by someone outside the team?

Curve Finance

3. What did Compound do that became one of the most memorable catalysts of DeFi Summer 2020?

Introduced Comp Rewards

4. As of now, roughly how many UNI tokens remain in the Uniswap Token Distributor contract deployed on September 16, 2020?

12 million

5. What was the approximate total value locked (TVL) in DeFi by the end of 2020?

15 billion

English

GIF

Scallop@Scallop_io

💧Introducing @SuiNetwork, Co-Host for Taipei DeFi Round happening during @TaipeiWeek 2025! Sui is a L1 blockchain, aiming to provide creators and developers with an easier-to-build experience for the next billion Web3 users. Want to meet the Sui Team? Register for Taipei DeFi Round here: lu.ma/taipeidefiround

ZXX

@GenzioCo @charlesdhaussy @dydxfoundation @bcgame @LevxApp had an idea 4 years ago at SushiSwap to introduce "franchised pools" that allowed CEX users to access DeFi yield from their CEX wallet.

Users are happy because high yield

CEXes are happy because users keep assets on their platform

DEXes are happy because more liquidity

English

🌐 @charlesdhaussy, CEO of @dYdXfoundation explores how DeFi and CeFi interact, and what the future of that relationship could look like.

This video is sponsored by @BCGame. Use code GENZIO when you sign up to get started today!

English