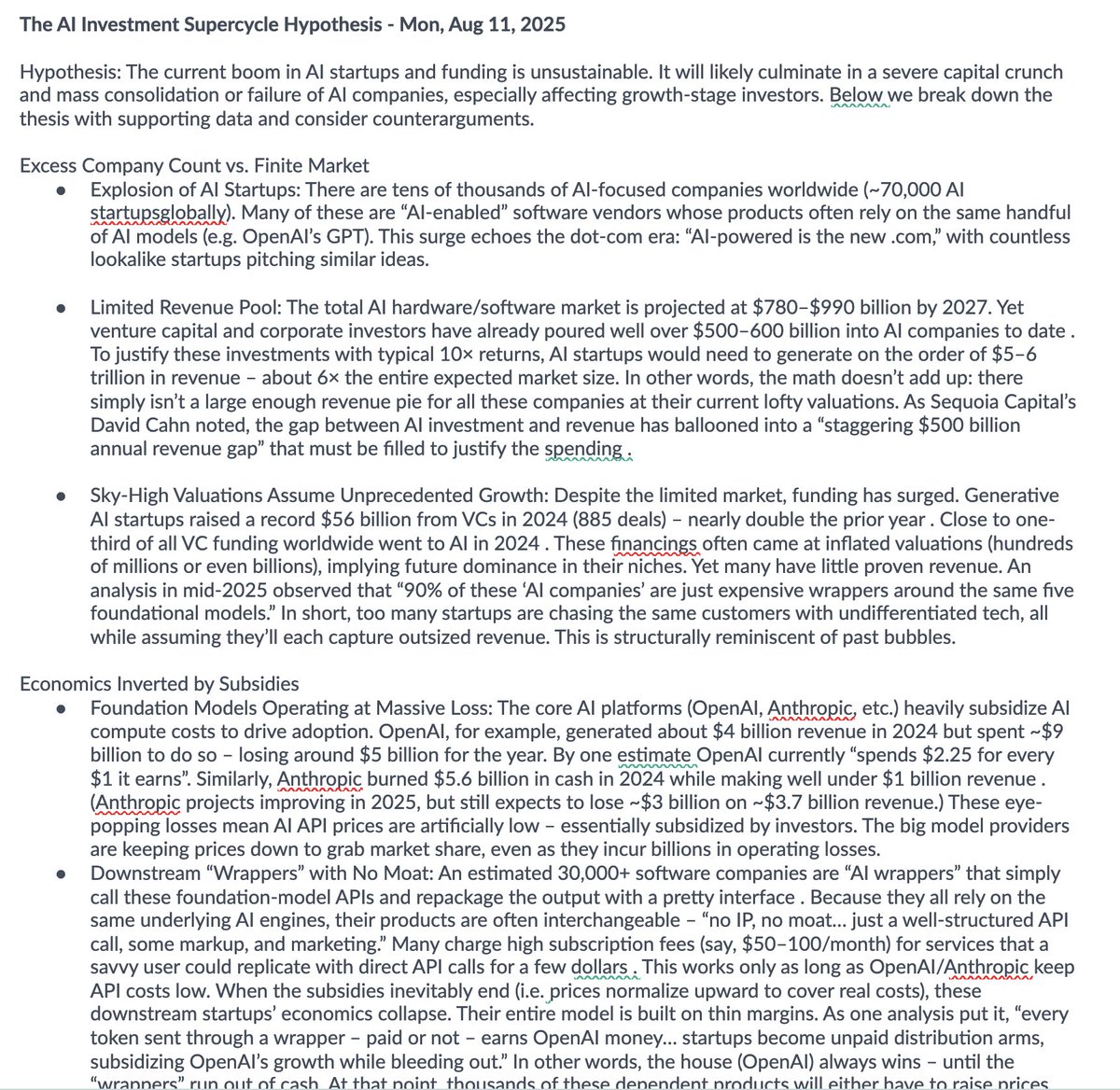

In August, I wrote this but never sent it. Publishing it felt like bad business. The very funds I was warning might lose were, and still are, key clients for Crossover Research. So I stayed quiet. But staying quiet no longer feels right. With software multiples down more than 30% across the board, and analysts calling this the SaaSpocalypse, the reckoning I expected has arrived. This is not a macro correction. It is not rates, inflation, or demand softening. It is structural. AI is not just competing with enterprise software; it is replacing it. The per‑seat model that powered twenty years of SaaS growth is collapsing as agents bypass the interface entirely and operate directly on the data. Salesforce, ServiceNow, Adobe, and Workday are all down 40% or more from recent highs. Thomson Reuters fell 16% in a single session after Anthropic released its legal agent. The room I once hesitated to rattle has already been rattled. The math has not changed since August. Only my willingness to say it out loud has. The Thesis AI acceleration is collapsing the cost of creation and narrowing the gap between “build” and “buy.” The winners will be those that: > Own mission‑critical workflows: controlling the system of record where business logic and risk live. > Capture proprietary, permissioned data feedback loops: continuously refreshed, high‑signal data that compounds advantage over time. > Convert trust and embeddedness into pricing power: turning reliability, compliance, and integration depth into premium retention. Everything else will be repriced toward zero. Four structural realities: 1. Commoditization crushes undifferentiated software. Vendors competing on price or easily cloned features face accelerating margin compression as AI drives time‑to‑parity toward zero. Only those with differentiated ROI, deep workflow embed, or regulatory trust sustain pricing power. 2. Enterprise exposure is a time moat, not a permanent one. Integration and compliance slow churn but do not stop it. As agentic AI removes implementation friction, retention will flow toward vendors that own the workflow, not those that simply serve large customers. 3. Build‑cost compression redefines survival. Stand‑alone tools and UX‑first point solutions are first to fall. Platforms that control data, compliance, and execution layers, the true systems of record, will outlast the rest. 4. Proprietary data feedback loops are the modern moat. Durable software compounds advantage through exclusive, self‑reinforcing data capture that directly improves outcomes and compliance intelligence. Raw data volume is no longer defensible; uniqueness, context, and feedback velocity define resilience. What this means for diligence This is exactly the question Crossover Research was built to answer for PE and growth investors: not whether a vendor looks sticky on paper, but whether customers prove the moat through workflow embeddedness, data defensibility, pricing leverage, and displacement risk. We have built a Voice of Customer diligence engine to make that visible [crossoverresearch.com]. If you want to read the full piece I wrote in August ("The AI Investment Supercycle Hypothesis - Mon, Aug 11, 2025") DM or email me: brad@crossoverresearch.com