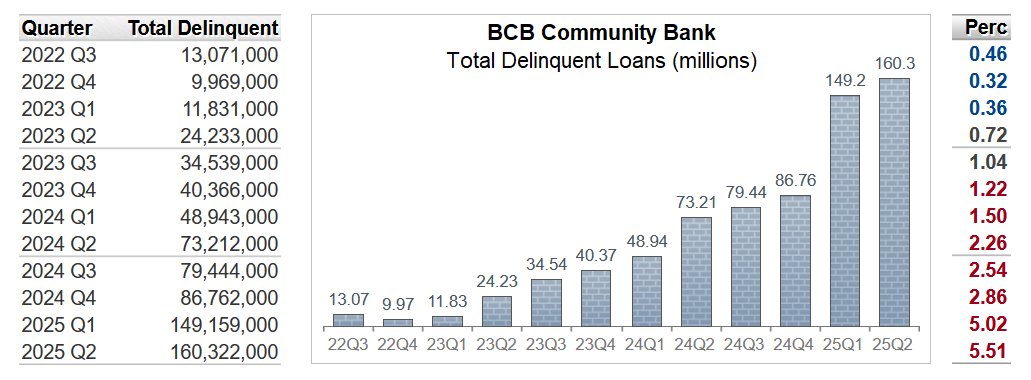

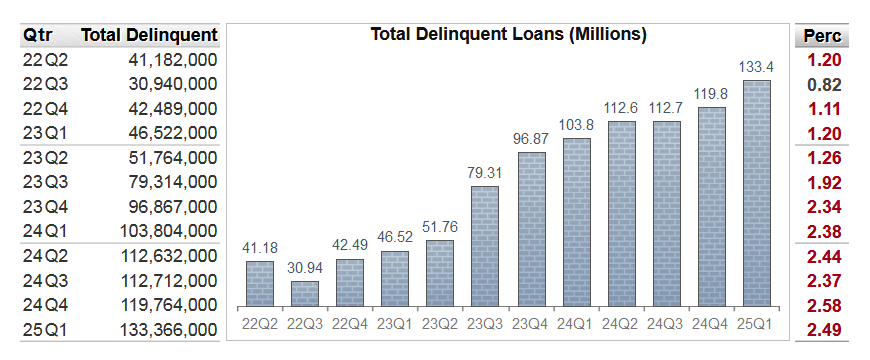

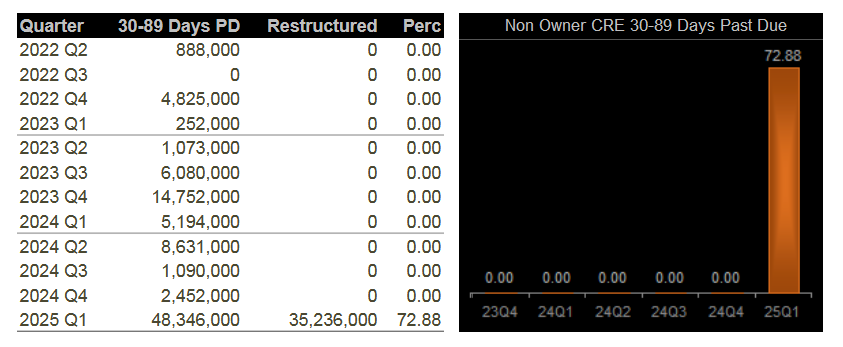

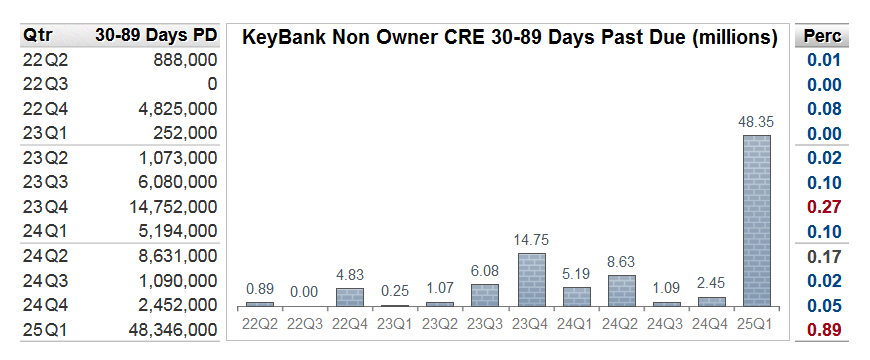

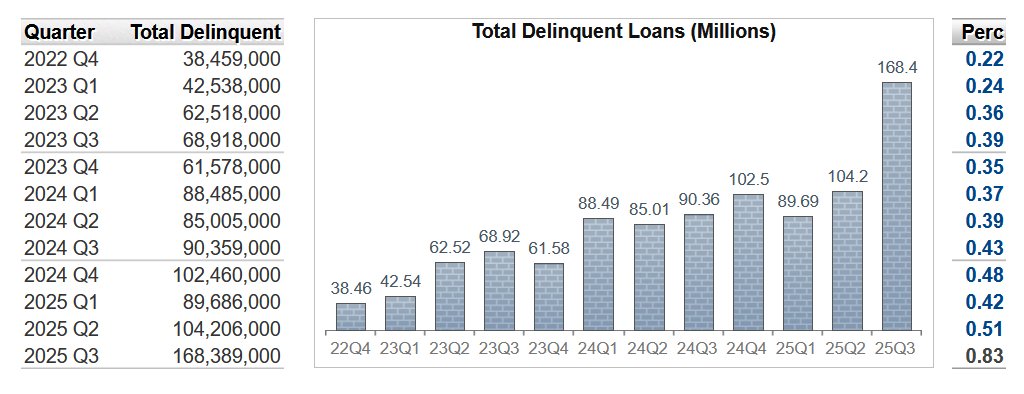

WaFd Bank (Washington Federal) delinquencies jumped $64.18 Million in 2025 Q3 resulting in their delinquency rate climbing to 0.83% from 0.51% in Q2.

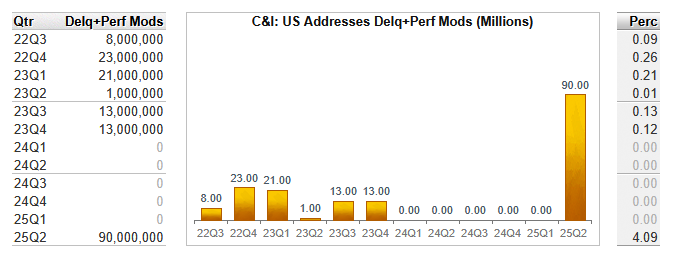

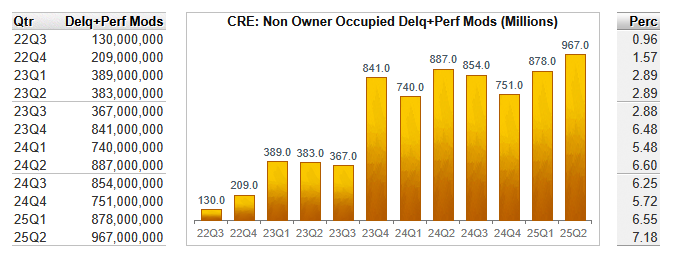

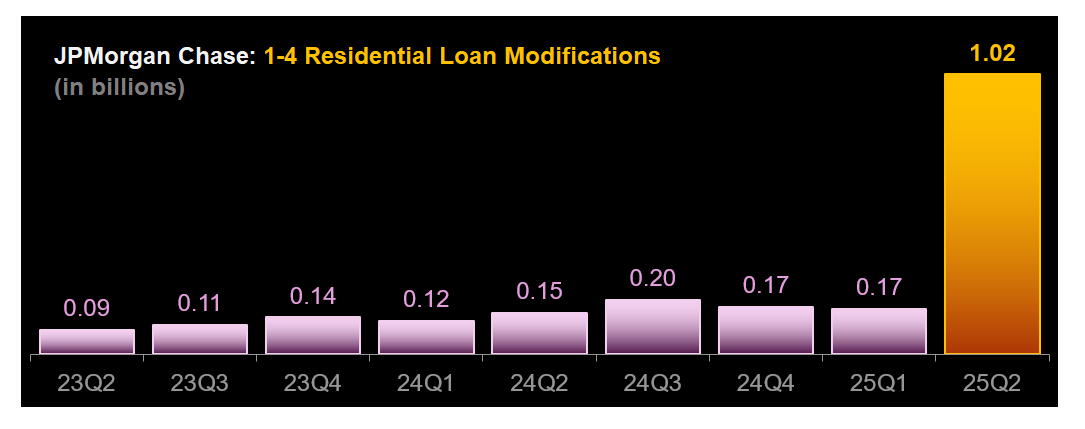

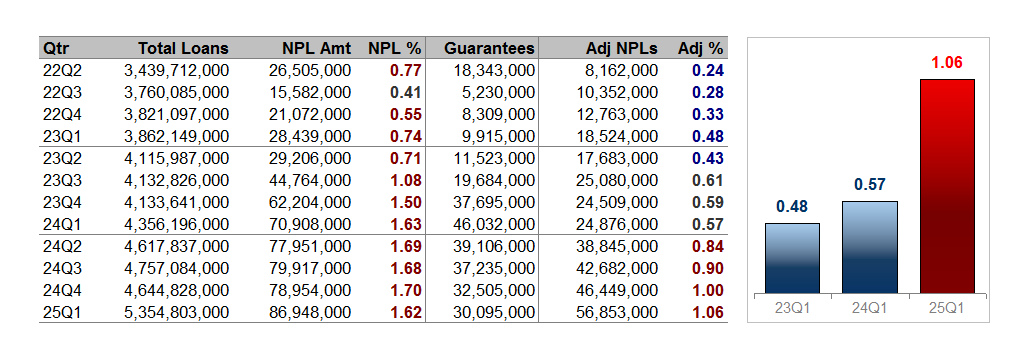

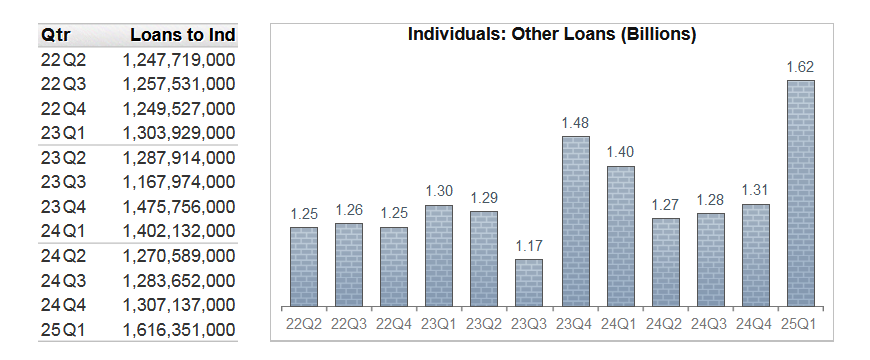

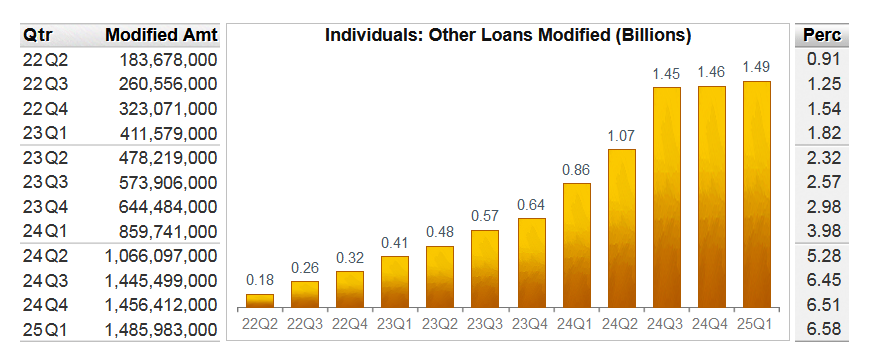

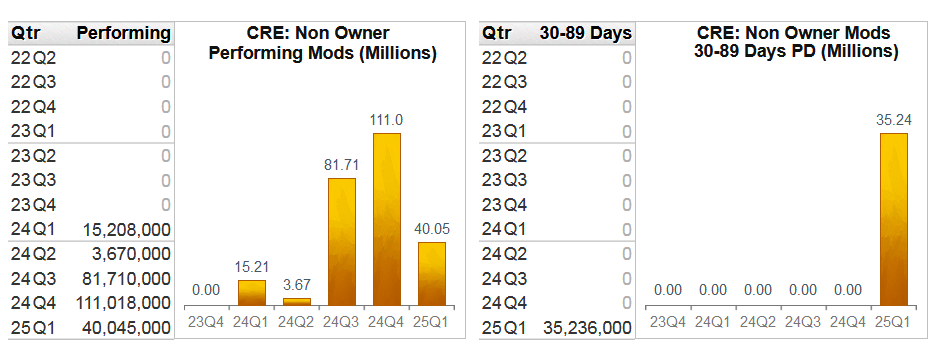

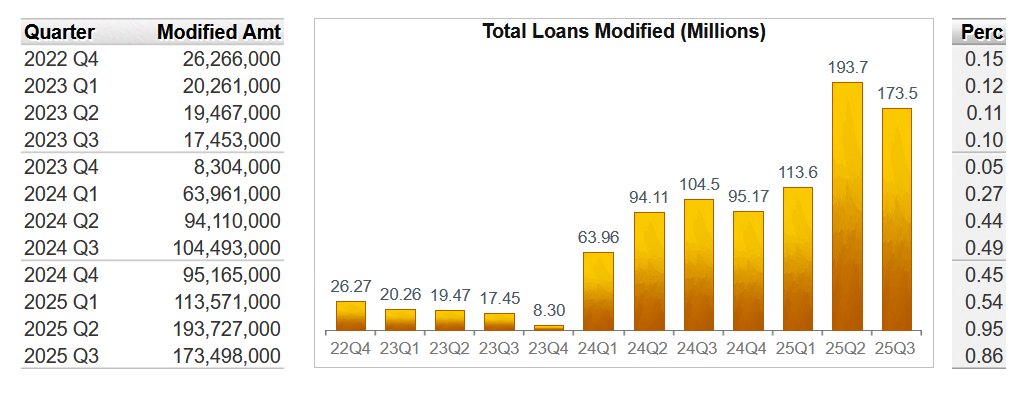

Loan modifications are elevated and are likely higher if not for the recent permanent rule change allowing banks to remove loans from modification reporting provided they make 12 consecutive payments.

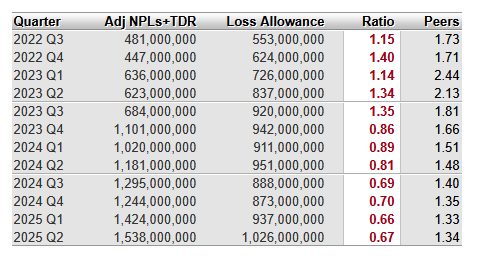

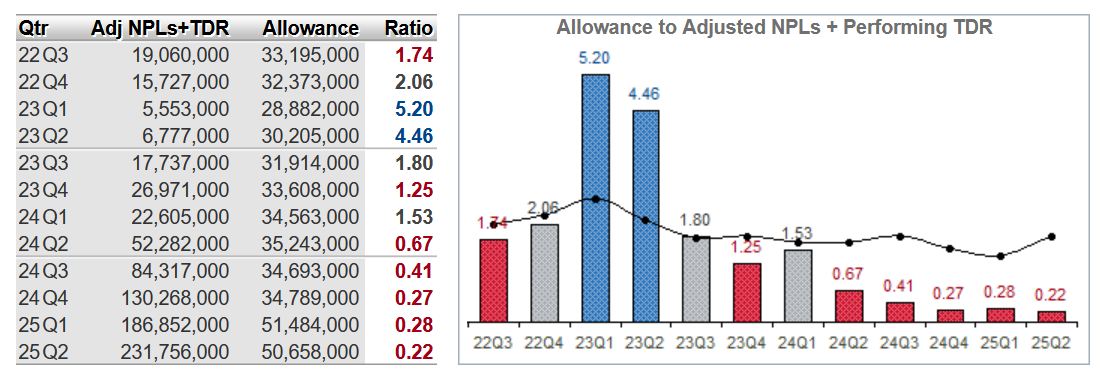

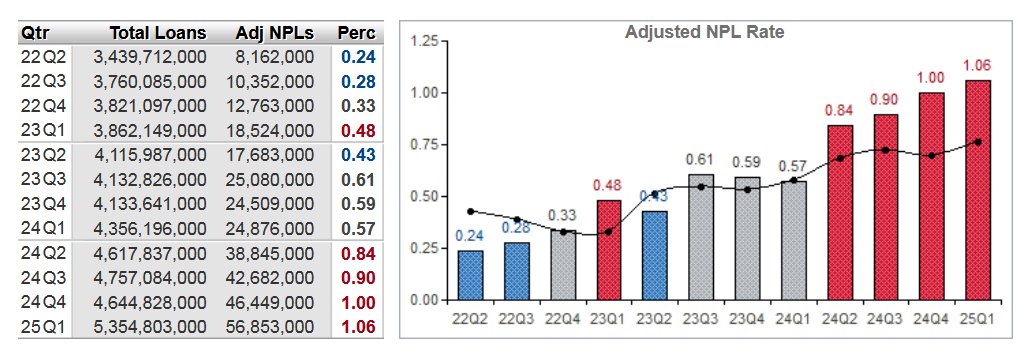

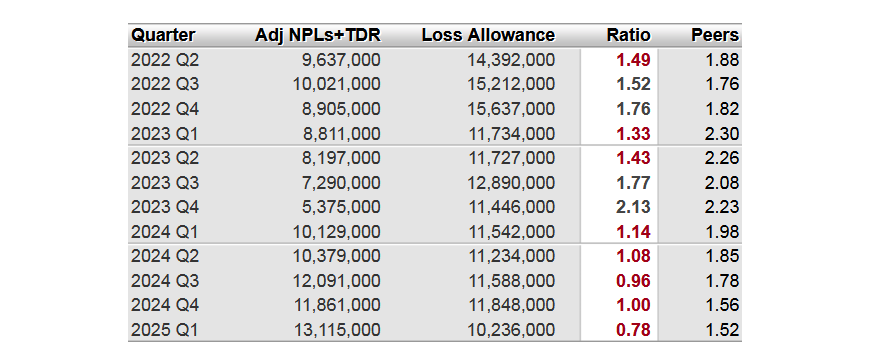

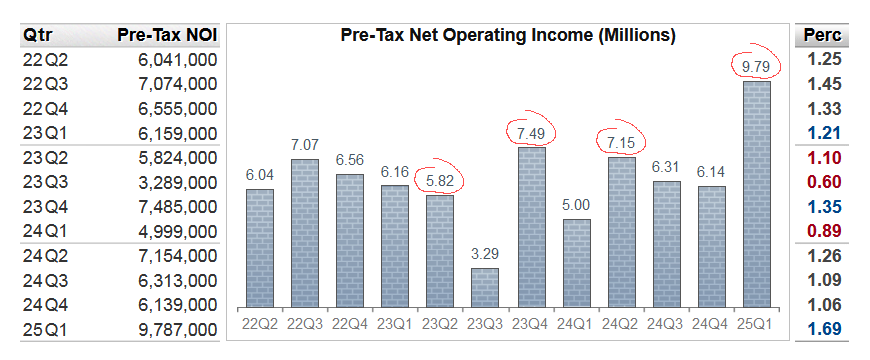

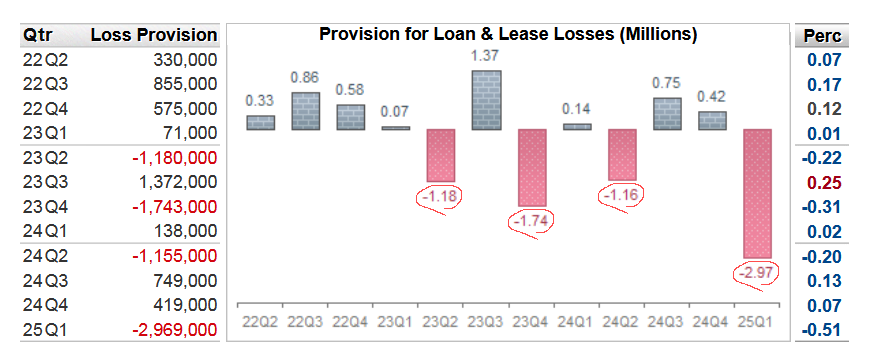

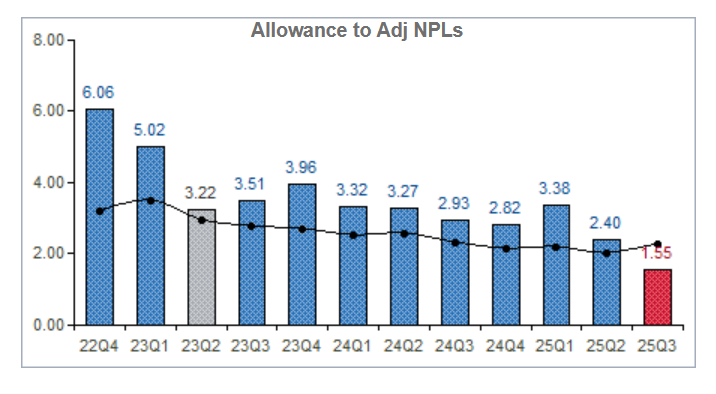

Looking at WAFD's Coverage Ratio it's clear they are managing earnings through lower Provision expenses. Reserves compared to NPLs reveal that WAFD is not well reserved.

English