Studybro

1.3K posts

社区群里真是卧虎藏龙,这两天跟群里一个老哥学会了Vibe Mining,一直靠手搓的我,瞬间觉得自己像个原始人。这两天可能是我今年来最兴奋和开心的时间了,保持谦逊,持续向牛逼的人学习。

100ⓧ 观察@100XInsight

后台好多人喊我开群,那我就试着开一个。先把丑话说在前面,免得后面有误会: 1.我会尽量抽时间看群消息并回复,但我的回答仅供参考,不构成任何投资建议。我自己挖矿跑节点也经常亏钱,很多项目都是暂时(甚至永远)无法变现的实验性垃圾币。如果你目前债务压力很大,或者需要稳定可靠的收益,强烈建议不要跟着我搞,风险极高。 2.我每天主要精力还是自己看项目和研究,时间有限。基础问题和手把手教学我很难一一回复(不是不想帮,是真的忙不过来)。如果你确实需要系统性辅导,可以考虑付费方式,我会认真对待,当一份工作来做。但我这个人天性散漫,最怕被“必须完成的任务”压着,所以尽量别选这条路,大家一起轻松交流更好。 电报群:t.me/+xRbmUptcK-E4N… 欢迎真正对低市值 DePIN、PoW、隐私/量子方向感兴趣、能接受高风险的游侠矿工加入。我们一起观察、一起学习、一起记录踩坑经验。群里也欢迎分享优质信息,但禁止广告、喊单和恶意攻击。

中文

Studybro retweetledi

On Grvt, every dollar does more.

We’re building a platform where capital can trade, earn yield from real-world assets, and work harder through capital-efficient products.

Together with @BinanceWallet, we’re launching a Booster Campaign.

🗓 10 July 2026, 07:00 UTC - 17 July 2026, 23:59 UTC

💰 1,500,000 $GRVT token, distributed on TGE day

No trading required. No deposits required.

How to join 👇

1️⃣ Open Binance Wallet → Discover → Booster

2️⃣ Complete the missions

3️⃣ Rewards unlock on TGE day

#Grvt $GRVT

English

@rialto_xyz @RobinhoodCrypto Hey, why isn't there a built-in wallet? It seems like I have to authorize every transaction once

English

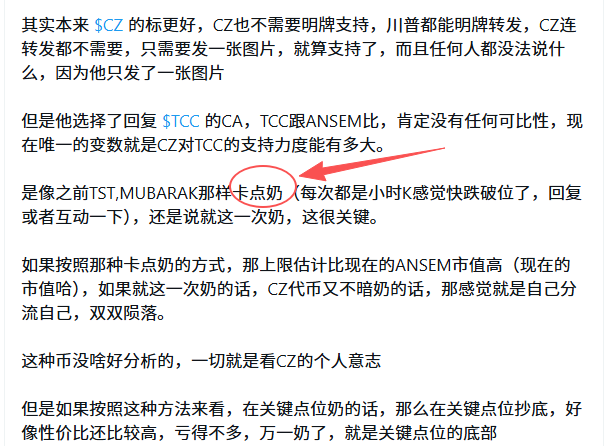

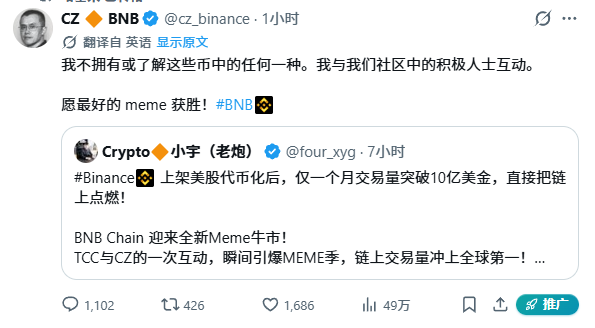

要说 $CZ ,就得回顾历史, MUBARAK,TST,我踏马来了,当时但凡有实时关注小时的K的都知道,绝逼的卡点奶的(互动);没有任何例外,都是小时K快跌位了,立马奶(互动)一口。

现在的CZ,何一跟币安不是不想搞MEME,而是既想把MEME搞起来,但又要避免掉一些其他层面的风险,比如川普那边的法律风险,所以你让CZ自己站出来说,我把70%的 $CZ 用来空投或者干其他的这种明牌支持,肯定不可能(时间仅限于当前阶段)。

CZ的话,深度解读:

1. CZ不拥有,也不了解这些代币(你们要买,就要学会自己了解风险,别赚了笑嘻嘻,亏了MMP)

2. CZ并没有单独支持 $TCC 的意思,我只是跟你们这些社区互动,今天可以互动TCC,明天也可以再次互动CZ,后天还可以互动AB或者其他的代币,千万不要以为CZ要把TCC用来打造品牌。

3. CZ 小时K又快跌破了,但是我卡点奶了,别说我看不上MEME,但是我有我的苦衷,我不能明牌支持,剩下的自己领悟。

4. CZ希望BSC有MEME的长期建设和长期生存周期,而不是昙花一现,所以他说 (愿最好的 meme 获胜!)

综合理解,又暗奶了一口 $CZ ,而且自己看小时K,不瞎吹,是不是小时K快跌破位了,有点稳不住了,奶了一口。(关键点位奶一口)

其次,晦暗的表达了还是会支持MEME,但是绝对不是明牌支持哪一个,而是哪一个牛逼就支持(暗奶、互动)哪一个,哪个有社区,就互动哪一个,你们不要搞道德绑架,我只是跟社区正常互动,别动不动赚了笑嘻嘻,亏了MMP。

那么接下来,就看跑出来的代币,谁是“建设者”了,那些经常能跟CZ保持过互动历史记录的“建设者”,在这里就充当了社区的角色;说句扎心的,你一般的小卡拉咪,你的推文都不会出现在CZ的推文时间线,你建设个JB毛。

如果深层次的思考 $CZ 的话 ,就是如果,我是说如果,有没有那么一种可能:

CZ喜欢做慈善,所以做了GIGGLE这款教育产品,当初 $SHIB V神拿去捐款30%还是50%给一个国家。

CZ这个代币如果未来能够持续上涨,当未来达到某个高度,可能CZ也会拿出50%去捐给某个国家或者国家级水准的大影响力组织;这种可能只有1%的机会,因为首先要保证代币不归零,其次要保证代币长期处于高市值,而且要稳住很久不崩盘,才可能实现这个设想。

最后就是说当下,这次CZ快跌破位了,又被奶了一口,如果下次再来一口,估计就要快速的ASTER,alpha,合约这些安排就位了。

0x7a848a5a8169aa6a2f603d056a749f924f504444

Writer@zhuilong888

其实本来 $CZ 的标更好,CZ也不需要明牌支持,川普都能明牌转发,CZ连转发都不需要,只需要发一张图片,就算支持了,而且任何人都没法说什么,因为他只发了一张图片 但是他选择了回复 $TCC 的CA,TCC跟ANSEM比,肯定没有任何可比性,现在唯一的变数就是CZ对TCC的支持力度能有多大。 是像之前TST,MUBARAK那样卡点奶(每次都是小时K感觉快跌破位了,回复或者互动一下),还是说就这一次奶,这很关键。 如果按照那种卡点奶的方式,那上限估计比现在的ANSEM市值高(现在的市值哈),如果就这一次奶的话,CZ代币又不暗奶的话,那感觉就是自己分流自己,双双陨落。 这种币没啥好分析的,一切就是看CZ的个人意志 但是如果按照这种方法来看,在关键点位奶的话,那么在关键点位抄底,好像性价比还比较高,亏得不多,万一奶了,就是关键点位的底部 0xa4390b901a63641c92327e5793b45fcb46954444 0x7a848a5a8169aa6a2f603d056a749f924f504444

中文

@rialto_xyz suggest changing the logo,otherwise, LV will sue you ass😄

rialto@rialto_xyz

We're excited to be a @RobinhoodCrypto Chain launch partner. We've worked closely with the team on stock token mechanics, onchain liquidity, and execution, and will soon offer 24/7 trading of stock tokens to eligible users and geographies.

English

x.com/youyou5202/sta…

类似我说的这样,但这是无许可的。任何DEV都可以基于这些标准去创建。让玩家来领空投。命中标准的玩家看公不公平,项目好不好决定要不要领。这样。

但BN ALPHA是审核制的

标准,定期更新。以保证公平性。

而紧跟BSC上各个优质项目或者热点的人,就可以定期领空投。

但不是领一次。是一直领。一直到下一次空投规则刷新。

所以很简单,一直研究BSC就行了。

糖十一、Don11@CS_Don11

@youyou5202 读下来,怎么感觉有点像变种的币安alpha 比如增加时间维度,项目维度,tx维度

中文

Studybro retweetledi

Exclusively on Binance Wallet: the Catapult Trade campaign is now live

🎁 Join to earn your share of a 1,666,667 PULT token reward pool

📜 Campaign Period: June 24th 15:00 UTC – July 1st 23:59 UTC

Details in comment!

English

Studybro retweetledi

1,666,667 $PULT up for grabs

Catapult Trade x @BinanceWallet are running a 7-day social airdrop campaign open to Binance Wallet users. 10,000 participants will be selected to share the full reward pool, with each winner receiving an equal cut.

To qualify, you need to complete social campaign tasks.

Selection is based on Binance Chain Hash Value, so the process is transparent and on-chain.

$PULT tokens will be distributed to winners by Binance shortly after token launch.

Campaign window: June 24th 2026 - July 1st 2026

Full details on participation: blog.catapult.trade/binance-wallet…

English

单号接近万u这一切都是因为会选择项目

作为一个普通学校大学生,我是怎么做到0投入参与 @Arcium A6 收入的。

我没有什么高深的理论,也没有内幕消息,更没有投入资金买筹码。我做的事情其实很简单:混 Discord、做社区贡献、做项目任务。最后拿到的最高角色,在 TGE 后对应的价值已经接近万u。

回头看这一年多的经历,我觉得最重要的并不是运气,而是在大部分人放弃的时候坚持了下来。

2025 年 4 月,我第一次接触Arcium。 那个时期市场上的项目很多,但 Arcium 给我的感觉和大多数项目完全不同。 当时申请 Apprentice(学徒)角色并不容易,审核标准非常严格。社区负责人会亲自审核成员提交的内容,甚至会指出推文中的错误并要求修改后重新提交。 很多人觉得这种审核流程太麻烦,但恰恰是这种严格,让我觉得这个项目和传统空投项目不一样。

社区当时存在两条成长路线: 第一条是身份路线:Apprentice → Adventurer → Confidant → Umbra 第二条是 Chad 路线:Emerging Chad → Growing Chad → Proven Chad → GMPC Chad 那时候项目方一直强调没有空投计划。

但与此同时,白皮书中又明确写着社区拥有 20% 的分配份额。 因此大量社区成员开始围绕角色体系进行建设,希望未来能够获得对应奖励。

第一阶段,大家最关注的是 EC 积分。 很多人每天完成任务、互动、发内容,不断累积积分。 我也投入了大量时间。 但随后发生了一件让整个社区震动的事情。 项目方宣布调整机制,大量依赖刷任务获得的 EC 被直接清零。 说实话,当时我也非常不理解。 辛苦积累数月的成果突然归零,换成任何人都会产生情绪。

但后来我逐渐意识到,这其实是 Arcium 社区治理最重要的一次转折。 如果继续按照积分数量决定最终收益,那么社区最终会演变成纯粹的刷分工厂。 项目方希望筛选的是长期建设者,而不是最擅长机械化完成任务的人。 从结果来看,他们确实坚持了这个原则。

进入第二期 RTG 后,我最大的担忧并不是任务量,而是不确定性。 因为经历过第一次规则调整后,没有人知道未来是否还会继续变化。 但最终我还是选择继续参与。 写文章、帮助新人、参与讨论、研究项目技术路线。 很多时候并不是因为我确定会获得回报,而是觉得已经投入了这么多时间,至少应该坚持到最后。

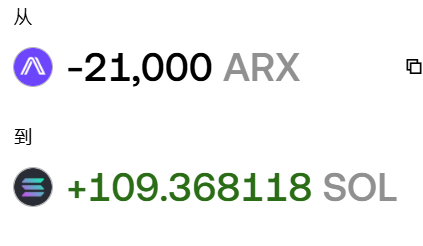

查询开放前的一段时间,社区里出现了大量 FUD。 有人认为所有份额都会流向 Alpha 用户。 有人认为普通 Builder 不会获得多少分配。 还有人认为角色体系最终不会有太高价值。 受这些声音影响,我对自己的预期不断下调。 最保守的时候,我甚至认为自己能够获得 5000 ARX 就已经不错了。 然而查询开放当天,结果远远超出了我的预期。

我的最终分配数量为 21000 ARX。 看到数字的那一刻,我甚至怀疑是不是看错了。 后面的事情大家都知道。

ARX 上线后从 0.2 美元附近一路上涨,最高接近 0.48 美元,我觉得可以达到0.8或者1$

对于一个没有投入本金、仅依靠社区贡献获得分配的人来说,这已经是一份非常可观的回报。

感谢狗哥 @jiamigou 提供的机会,让我在wb3中赚到了第一桶金

中文

Studybro retweetledi

Arcium × @BinanceWallet Booster Campaign is live.

Eligibility: Binance Wallet MPC Wallets with at least 2 Alpha Points.

Rewards: 1,500,000 ARX for 50,000 Winners

To join, go to Binance Wallet App - Discover - Booster - Arcium Booster Campaign.

English

@BigLLLG @renaissxyz 🎥 抽卡高光时刻记录

在抽卡过程中,提前录制视频并成功捕捉到 级卡牌触发的专属动画瞬间

额外奖励一枚「Mystic Luck SBT 」,用于记录这玄学抽卡时刻。

中文

Studybro retweetledi

自从币安上了美股之后,现在hip-3市场,币安,TradFi之间的波动也越来越大,最后都变成了meme的模样。

今天的大剧除了“无限增发”的 $WOK,还有老黄点石成金的 $MRVL 。

$MRVL 是少数支持隔夜交易的标的。可以看到刚才的新闻发出后,大家相对容易入场的 @binance 和 @tradexyz 相比传统券商的隔夜交易溢价最高到了 $15(+6%)

这也受到不同交易所之间的规则的影响(比如hip-3的oi上限)

加密韋馱|Skanda 🔶@thecryptoskanda

挺好,这样直接激活了链上对于美股价格的期现套利了 尤其是一些小盘股会逐渐开始受到crypto合约funding rate的影响,并且逐渐变成现货对合约1:9 看似是Binance券商化,实则是链上游资抢夺股市定价权的第一步。现货特洛伊木马里,装着的是永续合约的大胖子和小男孩 谁能卖得出去,谁就有定价权 一切终将币圈化 One market a time

中文