Pablo Campos

10.2K posts

Pablo Campos

@BullishBecker

Managing Partner at @CH1EFpartners Prev. Head of Market Intel at Bakkt, Ex SVP at Citi, Ex Visa. Digital Assets & Fintech Executive. Georgetown University MBA

Miami, FL Katılım Ocak 2021

1.4K Takip Edilen2.9K Takipçiler

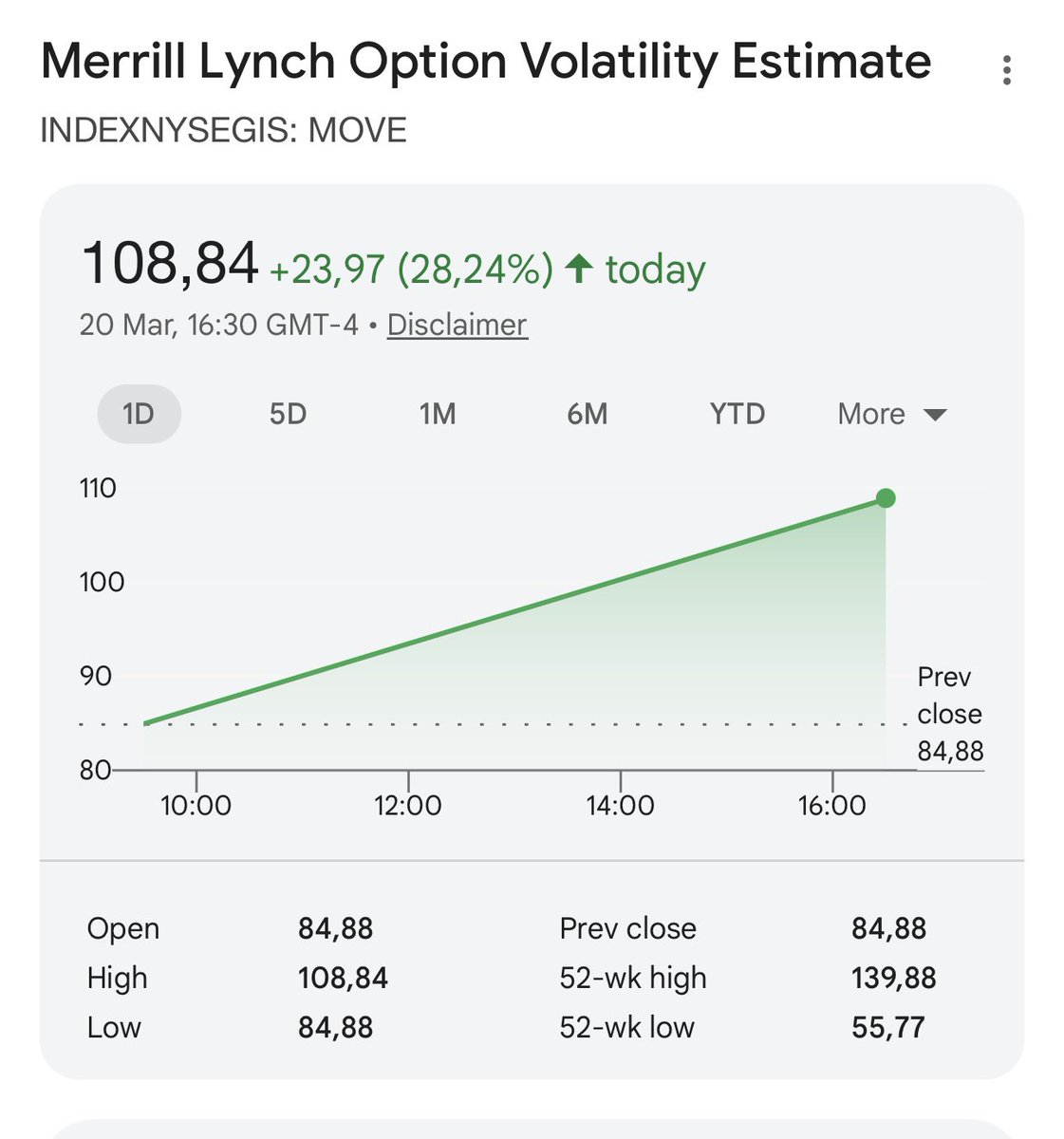

¡Estamos al limite! Esperaría un finde muy movido en una dirección o en otra. OJO a esto:

TRUMP DICE QUE ESTADOS UNIDOS CONSIDERA REDUCIR EL ESFUERZO MILITAR DE IRÁN

Español

Pablo Campos retweetledi

Credit to @SenThomTillis and @Sen_Alsobrooks for bridging the partisan divide to tackle a difficult issue. More work to be done to close out this and other outstanding issues, but this is a major milestone toward passing the CLARITY Act.

POLITICO@politico

Senators, White House strike ‘agreement in principle’ to resolve bank-crypto clash dlvr.it/TRcFBS

English

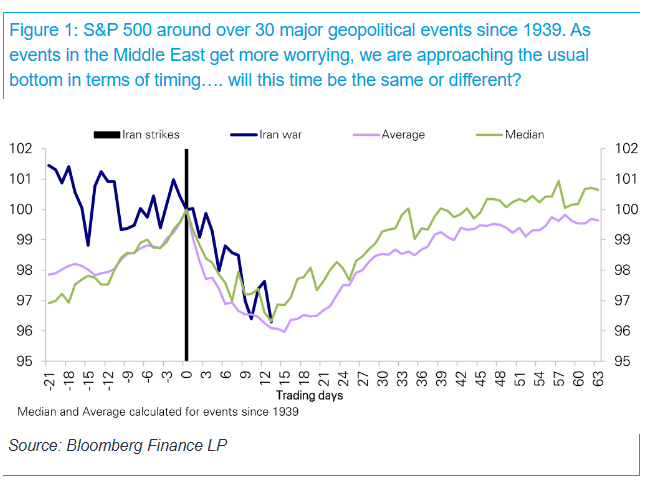

Se espera fin de semana movidito... En una dirección o en otra.

Según la trayectoria geopolítica histórica de las acciones estadounidenses, nos estamos acercando al punto en el que, en promedio, los mercados suelen tocar fondo.

Gráfico vía DB

Español

@DBATTAGLIAYtube Unlike Gold, Bitcoin has no counterparty risk

English

El oro desplomándose a nuevos mínimos 🚨

Bitcoin no 🫣

Que esta pasando? 👁️

Español

Al hilo: El 2Y de UK se ha pegado 100 bps en 20 dias…mas del doble que el americano!

Pablo Campos@BullishBecker

A lot of attention on US 10Y spike but the rest of the world should Blink much sooner

Español

A lot of attention on US 10Y spike but the rest of the world should Blink much sooner

GoldSilver HQ@GoldSilverHQ

🔥Europe, we have a problem. 🇫🇷 French 10-year government bond yield jumps to highest level since the European debt crisis 2011/12. 🇩🇪German and 🇬🇧UK 10-Y bond yields to follow suit very soon. This is fine...

English

@DBATTAGLIAYtube Exacto. No hay un exceso de demanda. Lo que hay es supply shock y high rates no ayuda en nada. Al contrario. Empeora

Español

Esto es muy grave ⚠️

Una subida de tipos no soluciona el problema del petróleo ⛽️

Todo esto es continuación de 2020.

Lo dije: la FED retraso lo inevitable con las subidas de tipos mas absurdas de la historia.

Esa inflación tiene que volver por algun lado.

Vamos a tener un crack en los bonos con altos tipos.

El peor escenario posible para todas las monedas fiat del mundo.

Bitcoin esta barato 🚀

Español

@WuBlockchain Yes, that and not been elected as next fed chair

English

Fed Governor Christopher Waller said he was initially open to rate cuts after weak February jobs data, but rising inflation risks and geopolitical uncertainty led him to support holding rates. He added policy is already restrictive, does not favor hikes, and rate cuts could still be possible later in 2026 if inflation eases and the labor market weakens.

English

No os disteis cuenta de este pedazo de patinazo ayer de Powell?

Le fallo el subsconciente…

Español

Cleveland Fed’s Nowcast updated

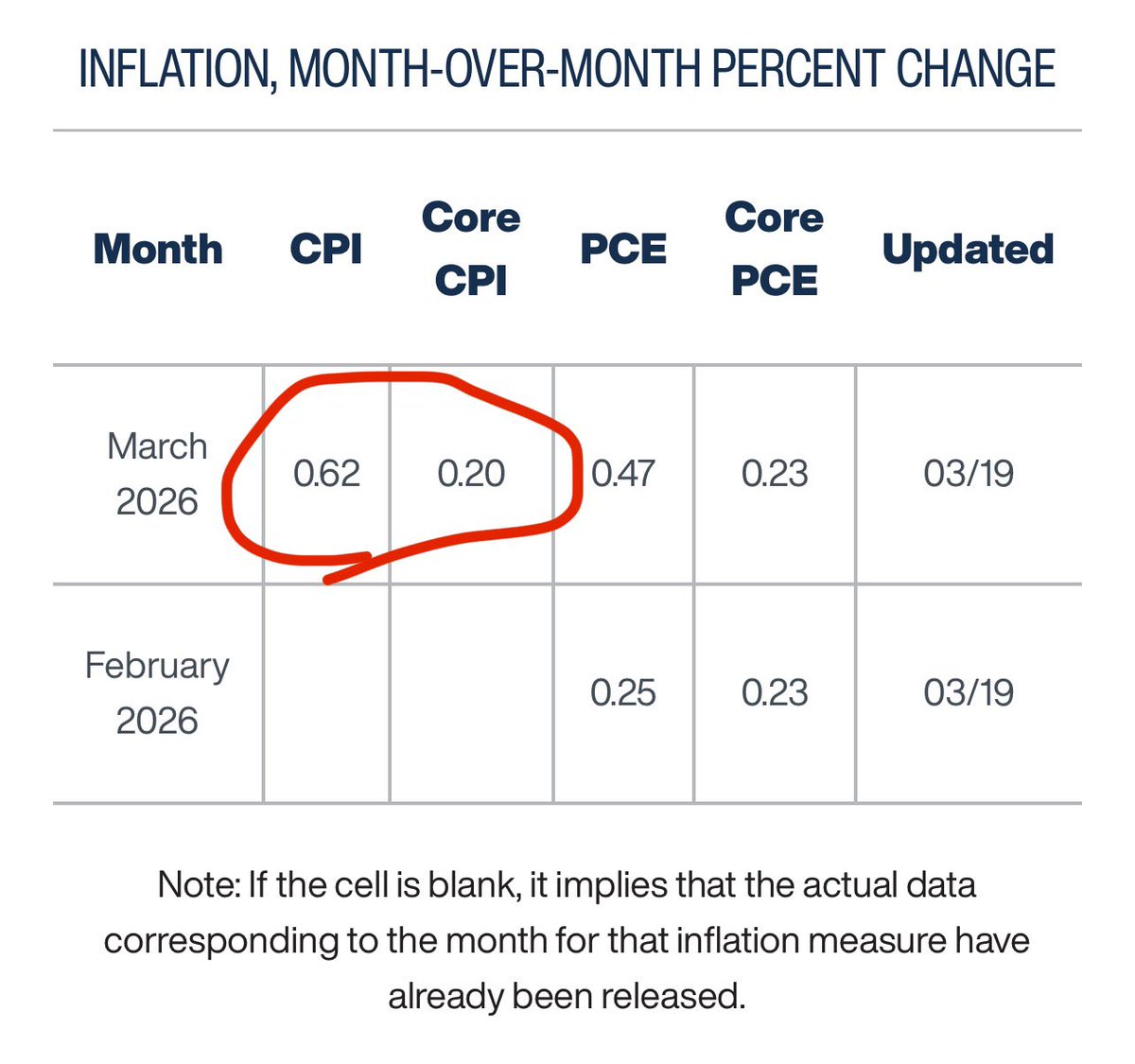

Nominal CPI MoM up from 0.47% to 0.62% (we started the month at 0.22%)

Interestingly, Core CPI est staying flat at 0.20%.

Mr. VIX@yieldsearcher

Cleveland Fed’s Nowcast just updated its March forecast for CPI. Headline CPI up from 0.22% to 0.47%. Core CPI remains at 0.20% for now.

English

Another reason why they are rushing to tokenize everything on the Blockchain!

zerohedge@zerohedge

Private Credit Panic Spreads: Consumer Loan Fund Gates Investors, JPMorgan Pulls Deal, Apollo Sees 20 Cent Recoveries zerohedge.com/markets/privat…

English

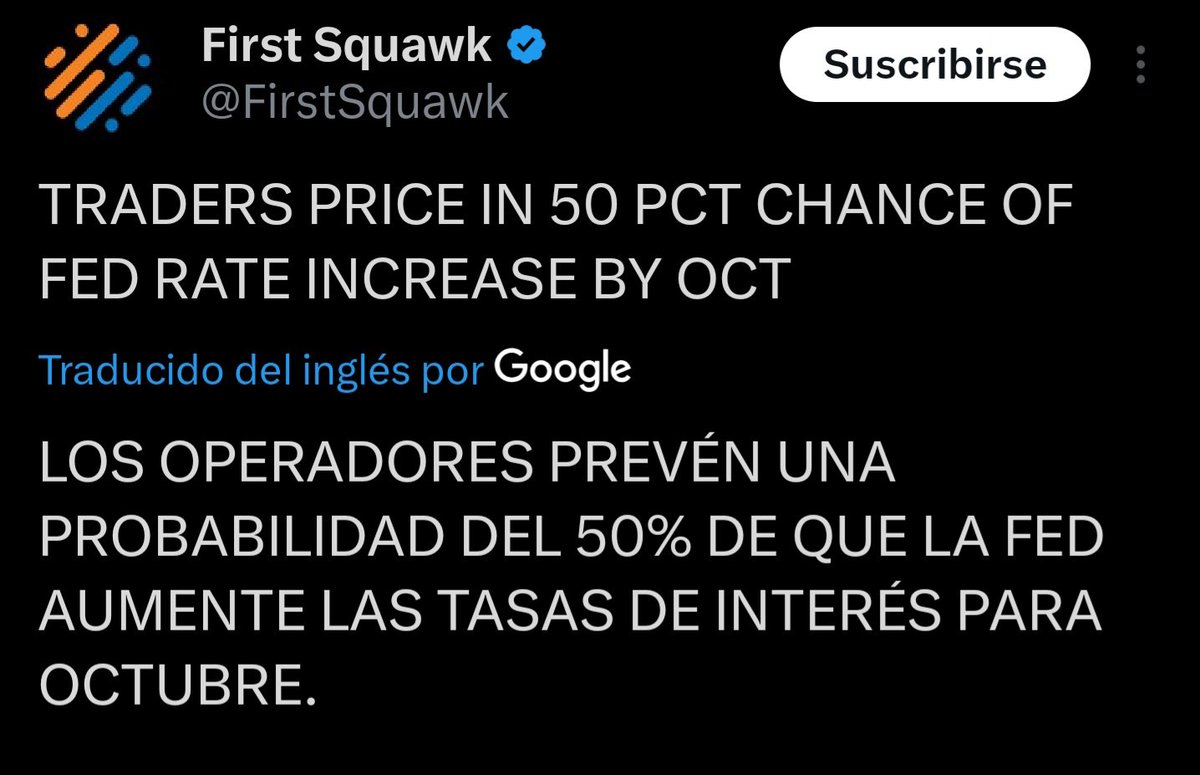

@Josevizner Yo creo q la cosa va por aqui x.com/firstsquawk/st…

First Squawk@FirstSquawk

US TREASURY SECRETARY BESSENT: WE'LL SEE IF KHARG ISLAND EVENTUALLY BECOMES A US ASSET

Español

Se han acojonado. Ya os decía que estaban locos de hacer eso.

Ya aceptan lo que les dice Trump. Ojo que España no está.

Español

La bajada del Oro y Plata y el repunte del 10Y te dice todo

Se estan quedando sin USD en Middle East

#liquiditycrunch

Español

@KevRGordon @carlquintanilla Unemployment itself takes care of inflation. You don’t need anything else

English

The dilemma for this Fed:

*Unemployment rate still in an uptrend over the past couple years

*National average price of gasoline about to reach its highest since 2022

English

@DeItaone As soon as Oil falls fast cuts will go up again to 2

English

*FED MAINTAINS PROJECTIONS FOR ONE RATE CUT IN 2026, ONE IN 2027

English

Repeat with me

There is NOT an Excess of Demand Problem with Oil

There is a LACK of Supply

Rate hikes does NOT solve that.

English

Mucha expectación con el Dot Plot de la Fed mañana pero no sabía que además de ir detras de la Curva los gobernadores de la Fed eran tambien expertos en Geopolitica

Nothing 🍔

Español

A few thoughts ahead of FED TOMORROW:

You hike rates primarily to restrain demand & help guide inflation sustainably toward the 2% objective.

That said, high oil prices-driven by recent geopolitical developments in the Middle East-can act as both an inflationary supply shock (pushing up energy and related costs) and a form of demand restraint (by reducing households' real purchasing power and potentially curbing spending).

Whether oil's net effect is disinflationary or inflationary depends on the shock's persistence and magnitude; at present, prices have spiked notably but remain volatile and highly uncertain.

The labor market has cooled meaningfully over 2025 and into early 2026: job growth slowed sharply (with 2025 annual gains revised down significantly in some reports), payrolls showed weakness or outright declines in some recent months, and the unemployment rate has risen to around 4.4% (near multi-year highs, though still historically moderate).

This softening in employment has also contributed to reduced demand pressures and helped bring inflation lower.

Headline inflation has stabilized around 2.4% recently (with core measures near 2.5%), close to but still somewhat above target, and shelter and other persistent components remain sticky but report with a Lag.

Bottom line: while domestic demand destruction from softer employment and potential oil-related headwinds reduces the need for additional tightening-and could even warrant patience or eventual easing— further rate hikes in 2026 appear unlikely IMO in baseline scenarios unless inflation reaccelerates materially (e.g., from a sustained energy shock or other factors).

English