ChrisM

4.4K posts

ChrisM

@CMoise51

Investor, Former Enterpreneur, Licensee of TEDxNashville

Franklin, TN Katılım Ekim 2008

643 Takip Edilen299 Takipçiler

@NoahWeiskopf Well Michael Jordan played 3 seasons. Look how is career was in the NBA

English

Caleb Wilson’s comment on #UNC basketball’s recent Instagram post, noting he earned First Team All-ACC honors:

“run it back? 😕”

English

@SaasStocks @AndreasSteno Agree. Market bots are reacting, no logic just playing the news.

English

@AndreasSteno It‘s not AI. It‘s hysteric investors not realizing that $NET $CRWD $OKTA make their money with other types of products. A Claude security scanner as threat for them? Come on…

English

And AI caused a new victim today

Claude@claudeai

Introducing Claude Code Security, now in limited research preview. It scans codebases for vulnerabilities and suggests targeted software patches for human review, allowing teams to find and fix issues that traditional tools often miss. Learn more: anthropic.com/news/claude-co…

English

@thomasrice_au Not sure how this replaces cybersecurity software that is geared toward preventing breaches, not just identifying patches.

English

$CRWD -8%, $GTLB -8%, $OKTA -9%

Not sure if generalists are going to be wading back into software anytime soon.

Claude@claudeai

Introducing Claude Code Security, now in limited research preview. It scans codebases for vulnerabilities and suggests targeted software patches for human review, allowing teams to find and fix issues that traditional tools often miss. Learn more: anthropic.com/news/claude-co…

English

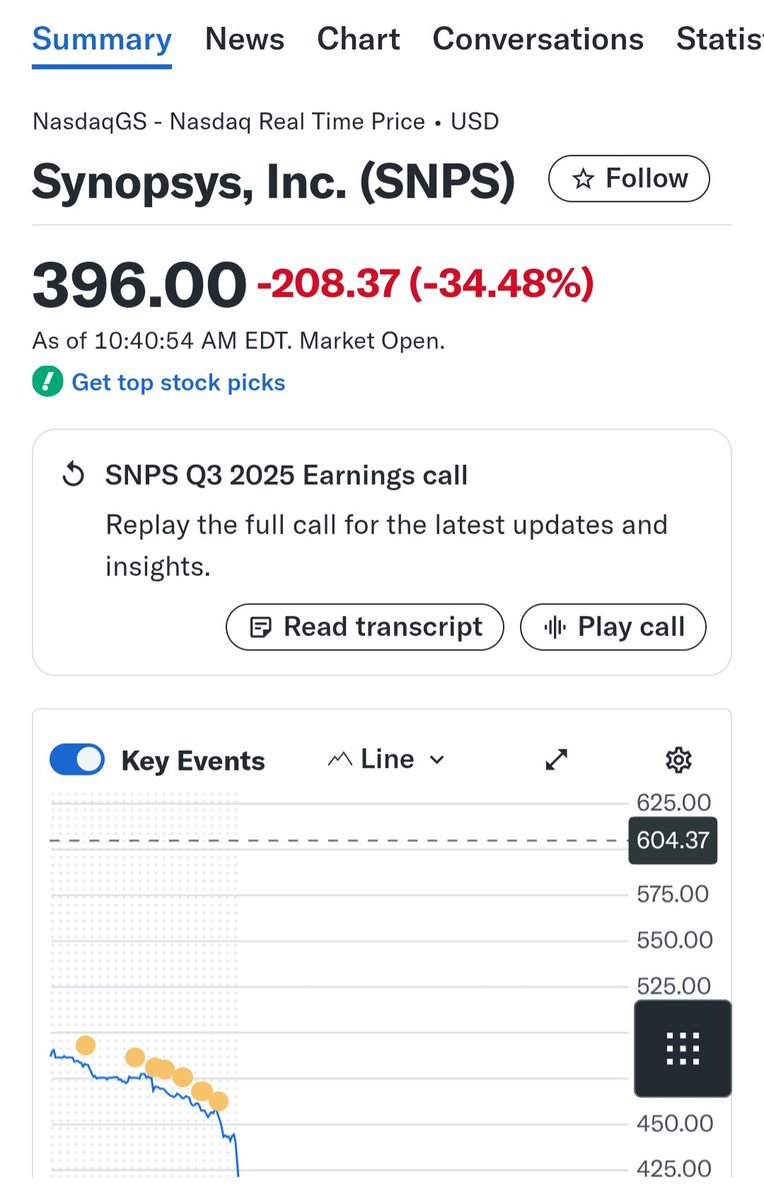

I know there was frustration on $SNPS, but listening to CEO Sassine Ghazi talk at the Goldman conference, they certainly understood what happens, are clear-eyed on what assumptions were missed (understandable), and how to fix.

English

@charliebilello #5 and #6 appear to be driving this party. Sure...easier money makes sense only if you own assets.

English

1. Stocks: all-time high

2. Home Prices: all-time high

3. Bitcoin: all-time high

4. Gold: all-time high

5. Money Supply: all-time high

6. National Debt: all-time high

7. CPI Inflation: 4% per year since Jan 2020, 2x the Fed's "target"

8. Fed: cutting interest rates next week

English

@hataf_capital Would you buy now its at ~$400, below your fair value price?

English

Synopsys: A Transformational Deal With Ansys, But Still Too Expensive

When Synopsys $SNPS announced it had finally closed its $35 billion acquisition of Ansys, I couldn’t help but pause. On paper, this is the kind of deal that reshapes industries. Combining Synopsys’ dominance in electronic design automation (EDA) with Ansys’ simulation expertise creates a powerhouse that stretches from silicon to full-system design. In other words, Synopsys isn’t just selling software to chip designers anymore it’s stepping into aerospace, industrial engineering, and beyond.

That sounds like the kind of pivot that should send the stock soaring. And to be fair, the market rewarded it: Synopsys’ shares jumped after the deal closed. But here’s where I step back. Even as the company boasts about its “transformational milestone quarter,” I still see cracks that the market seems eager to ignore.

The Quarter Beneath the Headlines

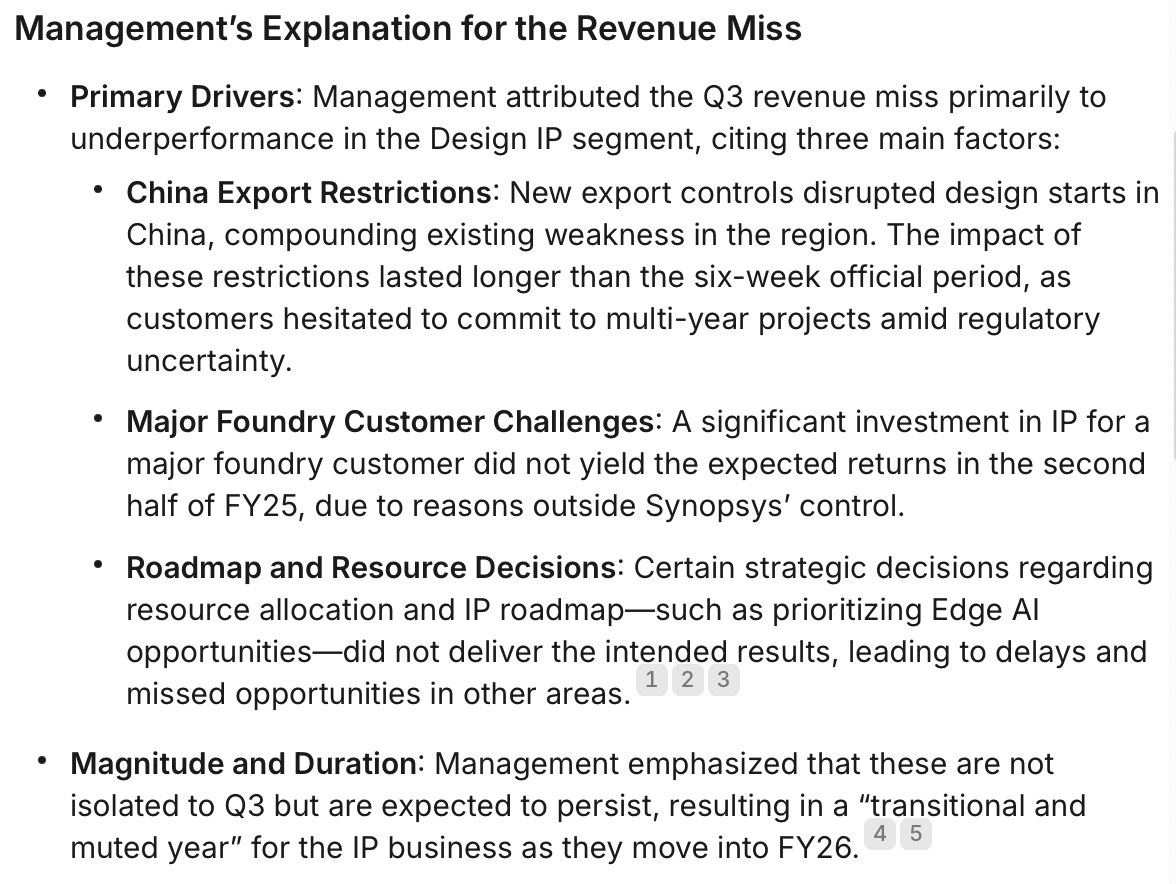

Synopsys delivered Q3 revenue of $1.74 billion with non-GAAP EPS of $3.39, in line with guidance. The standout: design automation revenue jumped 23% year-over-year to $1.31 billion, powered by AI and HPC chip demand. But the weak spot was unmistakable — design IP revenue fell 8%, hit by three forces:

1. Export restrictions to China stalling design starts.

2. A major foundry customer pulling back.

3. Internal missteps in road map and resource allocation.

In other words, Synopsys’ most scalable business line stumbled right when it should have been thriving. Management admitted this isn’t a one-quarter hiccup 2025 will be a “muted year” for the IP segment. That’s not the kind of language you want to hear when a company is trading at a premium multiple.

The Ansys Bet

Now, let’s talk about the Ansys integration. This deal does more than bulk up Synopsys’ revenue base. It positions the company at the intersection of semiconductors and broader engineering. Ansys brings simulation expertise used everywhere from aircraft design to renewable energy systems. Pair that with Synopsys’ automation software, and you get a suite of tools that customers can use to go from blueprint to physical product faster than ever.

That’s a compelling strategic vision. It also explains the $10.1 billion backlog Synopsys reported this quarter a number inflated by Ansys’ inclusion but nonetheless a reminder of the company’s stickiness with customers.

Still, big acquisitions come with big risks. Integration is messy, cultures clash, and the financials get clouded. Synopsys’ debt has ballooned to $14.3 billion, and management’s guidance for Q4 GAAP EPS in the red suggests near-term pain as they absorb Ansys’ costs.

Valuation Still Stretched

Here’s where my caution kicks in. Even if I’m impressed with the strategic logic, I can’t justify the stock’s valuation. I estimate fair value at $459 per share, well below where it trades today. My model assumes 12% revenue growth in FY25 (helped by Ansys) before normalizing to 15% annually, with modest margin expansion from pricing and efficiency. Using a 10.2% WACC and a 6% terminal growth rate, the numbers don’t add up to the current market price.

In plain terms: Synopsys is priced for perfection, and I don’t see perfection in an IP business that’s losing steam, a China market clouded by geopolitics, and the uncertainties of digesting a $35 billion deal.

Risks To My Bearish View

Of course, there are upside risks. The U.S. Department of Commerce recently loosened export restrictions, which could help Synopsys recover some lost China revenue. Its hardware-assisted verification platforms (HAPS-200 and ZeBu-200) are seeing strong traction, particularly in AI chip design a secular tailwind that could offset near-term IP weakness. If these trends accelerate, Synopsys could surprise on the upside.

But I’d rather not bet on policy swings and hardware adoption curves when the stock is already priced like everything will go right.

My Take

Synopsys deserves credit for taking bold strategic steps. The Ansys acquisition is the kind of move that can reshape an industry and extend its leadership beyond semiconductors. The company is deeply embedded in AI and HPC chip design, which is exactly where you want to be in 2025.

But investing is ultimately about price versus value. Right now, I see too much optimism already baked in. With an overvalued stock, lingering IP headwinds, and integration challenges ahead, I’m holding firm on my Sell rating, with a fair value of $459 per share.

English

@MandhirSingh5 Good write up and have to agree. Hard to get into these high quality companies. You have to take advantage of these types of down drafts.

English

🚨 $SNPS just executed a classic kitchen-sink quarter, the print is ugly, but the setup is cleaner.

1️⃣ There is Near-term pain - China exports are hit + foundry business wobbling + IP roadmap missteps → IP -8% YoY, cautious Q4, ~10% headcount reduction by FY’26.

2️⃣ But the growth engine is intact - the company closed ANSS, Design Automation is up +23%, backlog is now $10.1 Billion, hardware wins (ZeBu/HAPS), and 20 customers piloting Synopsys.ai.

3️⃣ The Noise is amplified by tariff chatter, Intel foundry confusion, ANSS integration, and guidance reset = expectations miss.

4️⃣ The thesis is simple - EDA is a duopoly (picks-and-shovels for AI). With ANSS cross-sell + subsystem/chiplet IP (including royalties), long-term revenue/EPS can 2–3× in around 3 yrs if execution improves.

$SNPS just dropped the ball… but for patient investors (3yrs+), this could be the moment to lean in before the rebound. #ManuInsights

English

@OmerCheeema Don't you think this is machine trading on the news? Strong return on invested capital. PE is now reasonable. Mutiple of cash flow to stock price could be better. But I bought some for the first time today.

English

$SNPS is down 35% on a narrow miss. There is something wrong with the capital market. EDA is the most stable segment in semiconductors. There are three main companies. They address a broad market. There is no threat of new competition. Semiconductor industry is growing. This much volatility in an established market is odd.

English

''A bet on the fat'' - My $NVO Thesis!

If there is one company that is out of favor on X right now, it's Novo Nordisk.

But underneath this negative sentiment, is a high margin, cash generating business that's perfectly set-up to benefit from the obesity trend.

🧵A big thread -Let's dive in 👇

English

@DougWahl1 TACO is all over financial media. People are trading off of it. Why not ask the President? He is probably trading it as well.

English

OUR HERO OF THE DAY IS...

Mary Cassella. She is the reporter for CNBC who asked the "TACO" trade question today.

Was it a fair question?

Your thoughts?

English

@RetroAgent12 It is only grift if Democrats do it. Republicans just close their eyes to the obvious. But then, Republican hands were forced with Nixon and Democrats didn't throw out Clinton. So maybe the game has not changed, Trump just showing them how to really profit being President.

English

While I very much appreciate the antipathy toward those wailing about the meltdown in the stock market and the impact on the economy of a long overdue imposition of fiscal discipline, it is an absolute fantasy to imagine that we can undertake this transition without a recession…. and a nasty one at that.

English

@JDVance You are now starting to look like a child with this response. Let’s keep in mind your boss wormed out of multiple calls to serve and your job as a journalist didn’t put you on the tip of the spear. Democrats have learned taking the higher road may be the winning road.

English

Hi Tim, I thank you for your service.

But you shouldn't have lied about it. You shouldn't have said you went to war when you didn't. Nor should you have said that you didn't know your unit was going to Iraq.

Happy to discuss more in a debate.

x.com/Acyn/status/18…

Acyn@Acyn

Walz: I firmly believe you should never denigrate another person's service record. Anyone brave enough to put on that uniform for our great country, including my opponent, I just have a few simple words. Thank you for your service and sacrifice

English

That is not what the SPR was created for.. unjustifiable

President Biden Archived@POTUS46Archive

Gas prices are down $1.40 from their peak after Russia’s war, but they’re still too high. My Administration is releasing 1 million barrels of gasoline from the Northeast Gasoline Supply Reserve ahead of July 4th, which will lower prices at the pump when folks need it the most.

English

@HeelIllustrated These bowl games are like preseason NFL games. Why would anyone want to go watch second stringers play in a meaningless game? Add in the Tar Heel play and we know why WVA dominated the crowd.

English

@spomboy @grossm130 I like living in a democracy. Prefer no chaos, no Trump, no Clinton. Maybe No Labels will make a difference.

English

@krassenstein @pjampaganza They are. Trump and his followers are the RINOS, not Mitt.

English

BREAKING: Mitt Romney said that he would vote for “anybody" running in the Republican primary except for Donald Trump or Vivek Ramaswamy, and that he would turn to support "a number of Democrats".

What do republicans think of this? How many Republicans feel the same as Mitt Romney does?

English

@QCompounding Tried your 7 day trial. Decided there was not enough new content there for me. In process of trying to end trial, I clicked on change plan. Substack automatically billed me with no confirmation to bill & no recourse for refund. So having to dispute. Not good biz.

English

@RudyHavenstein @SteveScalise Feel like I am flashing back to the late 1930s with American's view of the US and world order.

English

Hey, um, @SteveScalise - there are the issues at home we probably should address before we fix the world.

English

I keep thinking about this.

Rudy Havenstein, Senior Markets Commentator.@RudyHavenstein

"Ukraine is a mild concern in Scranton...locals say something about the nation doesn’t work any more — inflation is soaring, wages aren’t keeping up, labor shortages appear everywhere, government is dysfunctional & the American dream seems out of reach." archive.ph/hiqEp

English