CY

1.8K posts

Purely hypothetical: Why shouldn’t Anthropic acquire $IREN?

Iren currently controls 5GW+ of grid-connected power, likely scaling past 10GW in the next few years. Iren is also verrtically integrated.

They’re already globally diversified across Canada, the US, Europe, and APAC, and more to come.

Anthropic seems to be moving vertically into infrastructure to own their own compute. Bolting on Anthropic’s massive capital could hyper-accelerate IREN’s data center buildout.

If a buyout actually went down, would u accept that, and at what premium/price target do you think IREN shareholders would realistically accept? 👇

Hardik Shah@AIStockSavvy

📢 𝐉𝐔𝐒𝐓 𝐈𝐍: Anthropic Raises $𝟔𝟓𝐁 in Series H at $𝟗𝟔𝟓𝐁 Valuation - $AMZN $GOOGL $AVGO $MU $MSFT 👉 𝐊𝐞𝐲 𝐇𝐢𝐠𝐡𝐥𝐢𝐠𝐡𝐭𝐬: ➤ Anthropic secures $𝟔𝟓𝐁 Series H funding at $𝟗𝟔𝟓𝐁 post-money valuation. ➤ Round led by 𝐀𝐥𝐭𝐢𝐦𝐞𝐭𝐞𝐫, 𝐃𝐫𝐚𝐠𝐨𝐧𝐞𝐞𝐫, 𝐆𝐫𝐞𝐞𝐧𝐨𝐚𝐤𝐬, and 𝐒𝐞𝐪𝐮𝐨𝐢𝐚. ➤ Annualized 𝐫𝐞𝐯𝐞𝐧𝐮𝐞 run rate surpassed $𝟒𝟕𝐁 earlier this month. ➤ Funding will expand 𝐂𝐥𝐚𝐮𝐝𝐞 compute capacity, safety, and AI research efforts. ➤ Amazon committed $𝟓𝐁 within $𝟏𝟓𝐁 hyperscaler-backed investments. ➤ Anthropic signed multi-gigawatt compute agreements with 𝐀𝐦𝐚𝐳𝐨𝐧, 𝐆𝐨𝐨𝐠𝐥𝐞, and 𝐁𝐫𝐨𝐚𝐝𝐜𝐨𝐦. ➤ SpaceX to provide additional 𝐆𝐏𝐔 𝐜𝐚𝐩𝐚𝐜𝐢𝐭𝐲 through Colossus infrastructure. ➤ 𝐌𝐢𝐜𝐫𝐨𝐧, 𝐒𝐚𝐦𝐬𝐮𝐧𝐠, and 𝐒𝐊 𝐡𝐲𝐧𝐢𝐱 joined as strategic infrastructure partners. ➤ Claude available across 𝐀𝐖𝐒, 𝐆𝐨𝐨𝐠𝐥𝐞 𝐂𝐥𝐨𝐮𝐝, and 𝐌𝐢𝐜𝐫𝐨𝐬𝐨𝐟𝐭 𝐀𝐳𝐮𝐫𝐞.

English

@Cantal_Capital Cantal is holding 4000 shares of onds at 10.70 a strong position?

English

I have just went long Harmonic Inc. $HLIT

Here’s my thesis:

As you may know by now $NVDA recently invested in $NOK to upgrade telecommunication networks to run AI at the edge on cell towers

They are using Nokia’s anyRAN software to turn their cell towers into mini data centers to monetize AI

This method completely overhauls the need to physically rebuild all of the current physical infrastructure companies like T-mobile already have in place with just a simple software update

Why does this matter for Harmonic?

Well broadband/cable companies have been left in the dust for the longest due to their network infrastructure being stuck in the 90's where they aren't able to process the massive amounts of data that AI generates

At GTC 2026, Comcast and Charter (the 2 biggest broadband companies) confirmed they are moving $NVDA RTX 6000 Blackwell GPUs out of distant data centers and into their local neighborhood hubs

They are transforming their networks into a distributed AI Grid

You can't just put an NVIDIA GPU in a hub and expect it to work with a 30 year old cable network

Harmonic has a monopoly on what's called "vCMTS" which modernizes broadbands network infrastructure with a simple software upgrade just like NOK

This means broadband companies like Charter & Comcast will finally be able to monetize AI in business and residential areas using $NVDA GPU's to do things like offer personalized commercials to individual customers using AI at the edge in real time

Here is the huge opportunity for Harmonic..

As of 2026, broadband companies have gone into a state of emergency because they are unable to monetize AI like they want so they are going through a MASSIVE CAPEX cycle specifically for 'Network Evolution'

Comcast and Charter are spending $22 billion combined over the next few years to build a "Smart Grid." with 2026 being the most aggressive as they aim for over 50% of their capex to be spent to speed up the process

This is reflecting in Harmonics book as they now have a record $570M in backlog, up 77% YoY and recorded a 3.5 book to bill ratio in Q4 2025 ALONE 🤯

A $1.2B market cap with a $570M backlog which is probably at $600M+ now since this was announced months ago

Underneath the hood you may notice that the numbers look horrendous, however this is because they just sold their old legacy video business to go all in their "Virtualization" high margin SaaS business which is now growing at 33% YoY at a 55% margin showing off some serious operating leverage

The TAM for Cable Modem Termination Systems (CMTS) is estimated at $5.18 billion for 2026 with only 15%-20% of the entire global broadband infra virtualized giving them a HUGE runway for growth in the coming years

Harmonic is currently only doing $450M in revenue. This means they have only captured less than 10% of their immediate SAM, despite having a monopoly..

However, I expect this to grow even faster because now there are actual government incentives behind this

1st)

Starting May 8th, the FCC is starting an initiative called "Delete, Delete, Delete" which is a legal mandate for cable companies to stop wasting billions maintaining 30 year old copper wires & old hardware hubs

This is freeing up tens of billions in maintenance CapEx being redirected to upgrading their network

2)

The gov is currently handing out $42B in BEAD grants for rural high speed internet. To win these grants, operators have to deploy fast. You can’t build a physical hub in a month, but you can deploy Harmonic’s software in days essentially paying broadband to upgrade their network

For the longest the biggest risk was their customer concentration risk

but as of May 2026, rest of world revenue grew 33% YoY and now makes up 41% of their business

Meaning they are no longer just a USA merchant, they are becoming the global standard for the AI Grid with Comcast & Charter leading the way for the rest of the world to follow suit

Lastly, the chart looks absolutely stunning

It is clearly inflecting as management is making it clear that they are no longer a boring video business, but a pure play global AI infrastructure enabler

Now trading above all monthly moving averages which are starting to curl up and now breaking out of this massive bull flag

I really like this name going forward and think the cat comes out of the bag in their next earnings

NFA.

English

@aleabitoreddit Just curious, what is your highest conviction sector bet other than AI

English

Just a fun observation: the only people you see complaining about free research.

Typically have massive paywalls.

And get upset others are disrupting their business models.

I get tons of institutional/hedge fund offers.

But instead of doing things for institutions only or through heavily paywalled subscriptions.

I just publish my ideas to retail investors for free.

I think it’s about time retail has a level playing field?

English

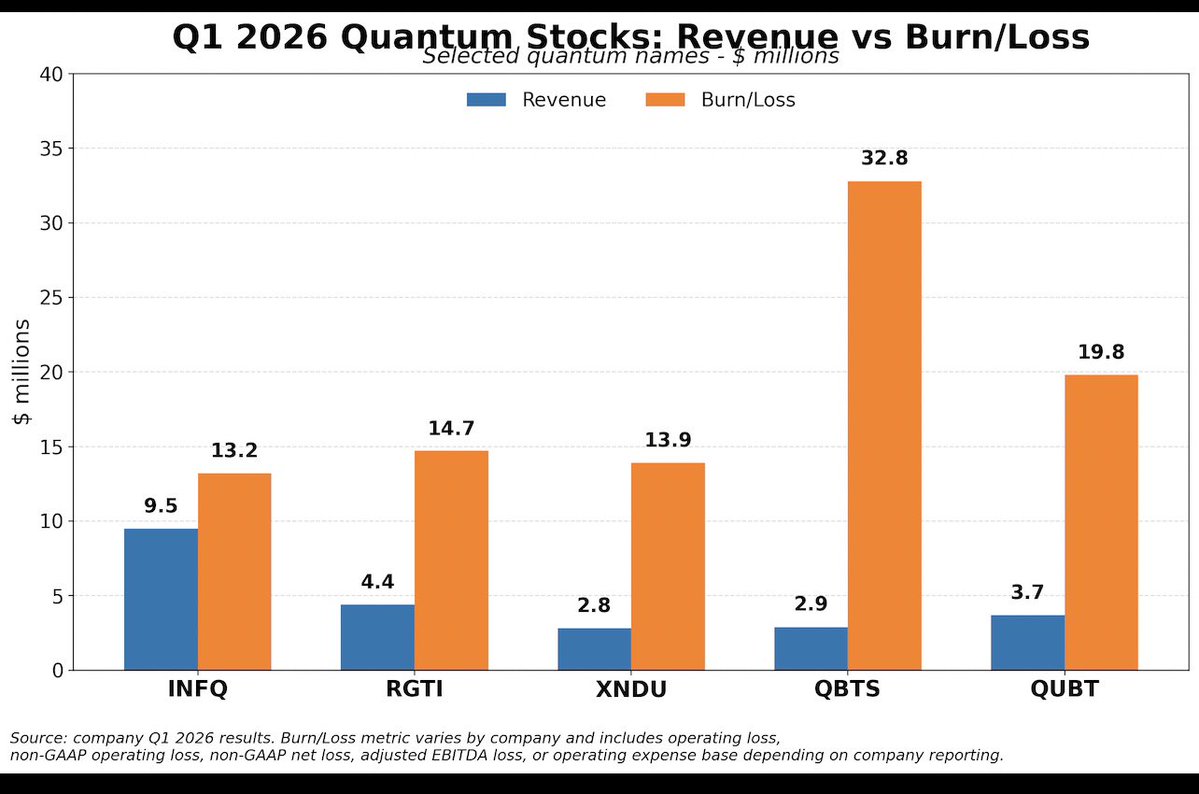

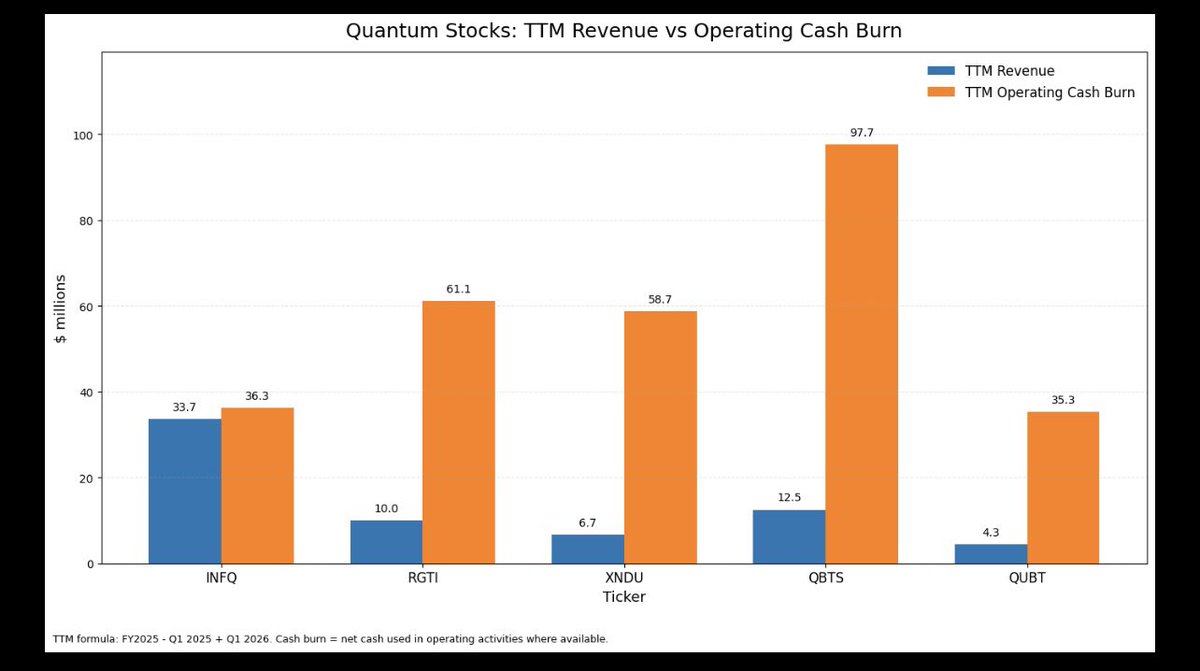

$IonQ $Qbts $Rgti $Infq $HQ

This Saturday I’m releasing the most comprehensive independent analysis of the quantum computing industry ever published outside a major institution.

Unlike anything I’ve ever shared. Substantially different in every capacity. In my view there’s this report — then there’s everything else I’ve shared.

This report took over a month to research and write, assisted by several incredible, extraordinarily knowledgeable individuals. The depth shows.

Written from the eyes of a CEO and a CTO — covering every aspect of what a company considering quantum must address. Strategy. Capital. Talent. Risk. Vendor selection. Security. The hard questions that never appear in a brochure.

Every stakeholder in the quantum sector — supply chain operators, system integrators, end users, investors — will want to carefully consider what’s in this.

Enterprise quantum is no longer a research project. The window for first-mover advantage is 2027–2030.

Saturday. Stay tuned.

Meanwhile - my sincere apologies to my friends here who have written directly or shared a comment that I have yet to respond to. The past week has been incredibly busy but I will catch up tomorrow.

Good night everyone.

English

@miscomputate Thanks for highlighting this. Building a small position of INFQ.

English

$INFQ If you get anything out of this post, look at the graphs at the bottom.

I excluded $IONQ from this comparison because it is already the larger, more established quantum name. This is focused on the smaller public quantum names where the re-rating debate is less settled.

Now that $INFQ @infleqtion has its first quarterly report out, let’s talk quantum re-rating.

I finally feel comfortable saying it:

Some of this valuation spread is bullshit.

Barron’s recently highlighted analyst coverage calling $IONQ and $XNDU top quantum picks, with $XNDU getting targets in the $40s.

Fine. But now compare this public quantum group on basic Wall Street stuff:

Q1 revenue vs burn/loss proxy:

$INFQ: $9.5M revenue / $13.2M non-GAAP operating loss

$RGTI: $4.4M revenue / ~$14.7M non-GAAP net loss

$XNDU: $2.8M revenue / $13.9M adjusted EBITDA loss

$QBTS: $2.9M revenue / $32.8M adjusted EBITDA loss

$QUBT: $3.7M revenue / ~$19.8M operating expense base

This is not about which modality has the sexiest story. This is revenue today, burn discipline, commercial traction, balance sheet strength, and path to scale.

On that basis, $INFQ looks mispriced.

More revenue than several peers. Better revenue-to-burn efficiency. $569M in cash/securities. 100% organic quantum revenue. 2026 guide updated to “at least $40M.”

Not risk-free. Not guaranteed. Not moon tomorrow.

But if analysts can justify premium targets on quantum names with lower revenue and similar or worse burn, then $INFQ sitting in the penalty box makes less and less sense.

The re-rating argument just got a lot stronger.

Graphs:

1. Q1 only — revenue vs reported Q1 burn/loss proxy.

2. Trailing 12 months — revenue vs operating cash burn, using FY2025 - Q1 2025 + Q1 2026.

3. No guidance chart included — because none of the other names here gave formal 2026 revenue guidance in their Q1 releases. $INFQ is the exception, as they are the only one formally guiding, and guiding to at least $40M.

Not perfect apples-to-apples.

But the point is clear:

$INFQ is much closer to revenue/burn balance than the market is pricing.

English

You can usually tell what someone believes by what they own.

$ONDS

$IREN

$KRKNF

$ASTS

$RKLB

$SIVE

$ASPI

$DGXX

Defense. Power. Space. Autonomy. Compute. Bitcoin.

Yeah, that sounds about right.

English

@CY40236170 Palantir only good because of government contract..u take those..large portion of their revenue will gone

English

$NOW vs $PLTR vs $CRM

Three AI software kings. One question:

Which one actually belongs in your portfolio?

Let's let the numbers decide.

$NOW — ServiceNow The silent compounder

→ Forward P/E: 21.7x — cheapest of the three

→ Revenue growth: 22% YoY — consistent and predictable

→ FCF Margin: 44% — cash printing machine

→ AI adoption: Now Assist customers +130% YoY

→ Avg analyst target: $144 — 58% upside from here

→ Net cash: $2.75B — fortress balance sheet

The verdict:

Highest quality. Lowest risk. The default AI control tower for enterprises — and still the most underrated of the three.

$PLTR — Palantir The hypergrowth monster

→ Forward P/E: 97x — yes, it's expensive. Keep reading.

→ Revenue growth: 85% YoY — the fastest in enterprise software

→ FCF Margin: 57% — more profitable than most "cheap" companies

→ AI adoption: 206 deals worth $1M+ in Q1 alone

→ Avg analyst target: $194 — 41% upside from here

→ Net cash: $7.8B — zero debt, unlimited runway

The verdict:

Insane valuation. Insane growth. When a company raises guidance to 71% and still beats — the market eventually has to pay up. This is the asymmetric bet.

$CRM — Salesforce The sleeping giant

→ Forward P/E: 13.8x — by far the cheapest

→ Revenue growth: 12% YoY — boring, but re-accelerating

→ Agentforce ARR: $800M — +169% YoY→ RPO backlog: $72.4B — visibility for years

→ Avg analyst target: $279 — 54% upside from here

→ Net debt: -$8.15B — the one balance sheet risk

The verdict: The value play nobody talks about. 14x forward with the biggest installed base in enterprise software and Agentforce scaling faster than anyone expected. The "safe" way to own agentic AI.

The real question isn't which one to pick.

It's which combination fits your conviction.

💬 Which of the three are you most positioned in right now? 👇

English

$HIMS quarter was awful

Avoided.

Pivoted to $RDDT last week.

English

For those of you that have asked, here are the current positions I hold in my brokerage account:

$CIFR - 1800 shares

$BMNR - 900 shares

$PLTR - 100 shares

$IBIT - 290 shares

$MP - 110 shares

$SOFI - 400 shares

$VOO - 3.09 shares

Feeling pretty good about this portfolio. What do you guys think?

English

$IREN is now cheaper than it was before the $NVDA deal was announced.

Wow.

English

English

Overnight, $IREN traded almost AUD $10 billion in a single session on the NASDAQ - more than the entire @ASX's on-market daily turnover of AUD $7.5 billion.

I'll be honest. That number is humbling. But it also stings a little.

Because two and a half years ago, we were told we weren't welcome on the ASX.

The rejection was disappointing - not just for what it meant for us as a company, but for what it said about Australia's willingness to back next-generation technology at scale. We believed then, as we do now, that the future of digital infrastructure and compute deserved a place in Australian capital markets. Apparently, the feeling wasn't mutual.

But we never gave up on Australia.

We have continued to try and do business here. We have several large-scale data centre development sites across the country, and our commitment to building world-class, renewable-powered infrastructure on Australian soil has never wavered.

Australia has everything it needs to be a global leader in AI infrastructure - the land, the renewable energy, the engineering talent.

The permitting and regulatory process remains our biggest challenge - and I won't pretend otherwise. It is slow, complex, and at times deeply frustrating for a business operating at the speed that AI demands.

What it needs now is the regulatory and policy environment to not miss out on this opportunity.

But we are working through it, and when we get to the other side, we are ready to accelerate.

English

$IREN closed above $60 today, so my shares will be called away tonight. With that, I’m completely out of $IREN at around a 40% profit.

This trade was made because I saw a better opportunity in $ASTS, not because my thesis on $IREN is broken.

In my opinion, $IREN still has significant upside, but the road to get there won’t be easy. The company needs a lot of capital to buy GPUs and build data centers. That said, they have access to substantial power capacity, so things could work out very well if management executes properly.

My primary thesis was around selling compute to hyperscalers, but with the recent acquisition, it looks like they’re also pursuing software-layer ambitions. I’m not sure how well that plays out against $NBIS, which I think is currently doing a much better job delivering full-stack AI services to smaller customers.

English

@growthrapidly Stopping complaining, it’s exactly them doing the stupid things we make our profits.

English

🚨 BREAKING: DEUTSCHE BANK LOWERS $HIMS PRICE TARGET TO $25 FROM $28, MAINTAINS HOLD RATING

English

Example of an extremely solid portfolio till 2030.

$DRAM - 25% > Memory cycle.

$NBIS - 25% > AI-native cloud infrastructure.

$LITE / $MRVL / $TSEM - 25% > Lasers, optical DSPs, and silicon photonics foundry.

$SIVE / $M7U / $IQE / $SOI / $LPK - 25% > The European photonics supply chain.

English

Which stock has the greatest upside potential right now

$NBIS or $IREN?

English