Cern Basher@CernBasher

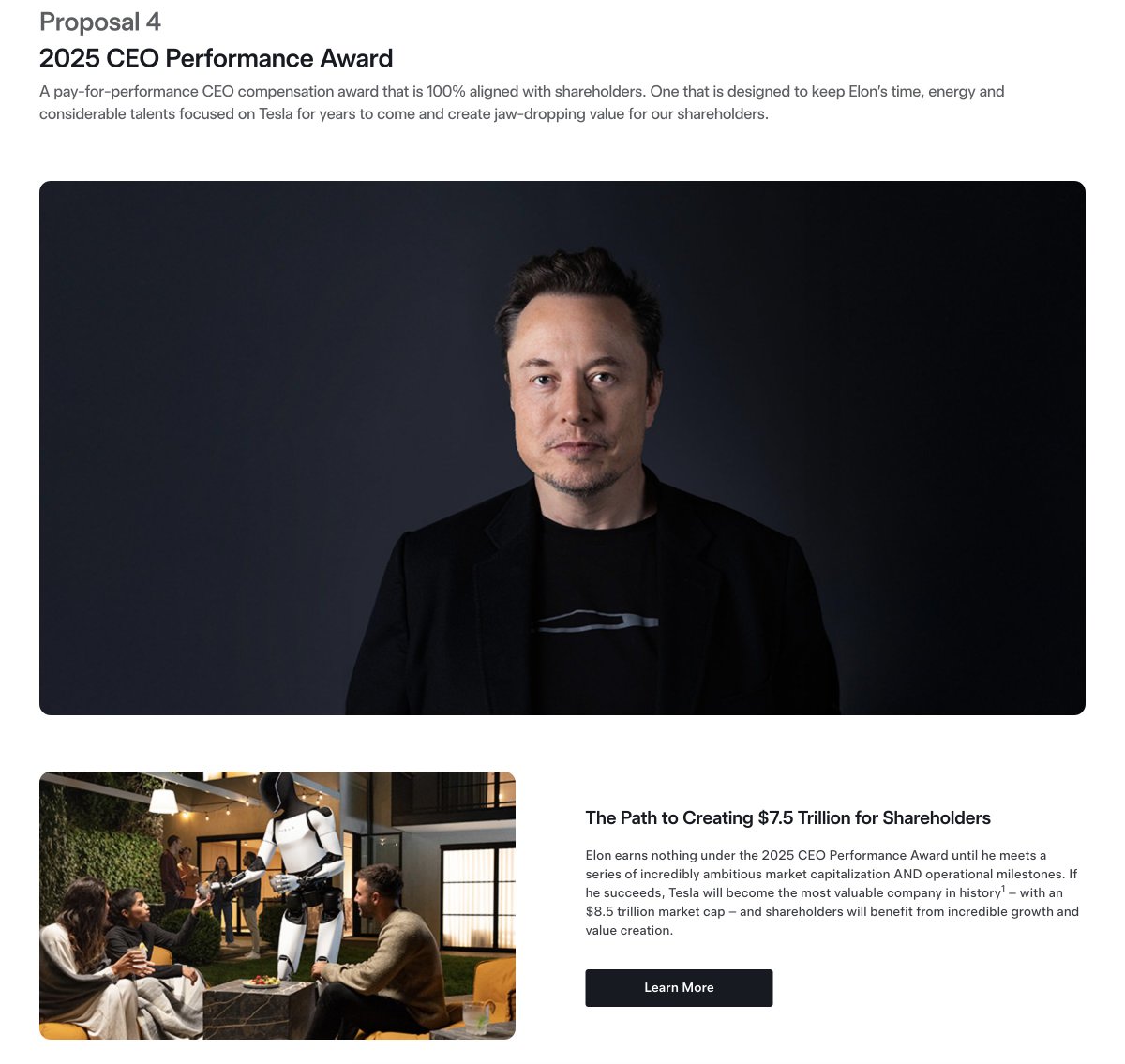

2025 CEO Performance Award for Elon Musk

Let’s design a new compensation plan for Elon Musk, modeled after the 2018 Tesla CEO Performance Award.

The 2018 plan was a 10-year, 100% pay-for-performance structure with no salary or bonuses, focusing on stock options tied to market capitalization and operational milestones.

We’ll adapt this framework to reflect Tesla’s current valuation, ambitious growth targets, and Elon’s role in driving innovation, while ensuring the plan incentivizes long-term value creation for shareholders.

Overview

Structure: 100% pay-for-performance, 10-year term (2025–2034), no salary, bonus, or time-based equity.

Compensation Type: Stock options, vesting in tranches based on achieving dual-trigger milestones (Market Capitalization + Operational).

Goal: Align Musk’s incentives with Tesla’s growth, aiming for a $5 trillion market cap by 2035 (a 5x increase), reflecting Elon’s vision of Tesla as an AI and robotics leader, not just an automaker.

Tranches

Number of Tranches: 12 stock option tranches, each equal to 1% of Tesla’s outstanding shares as of May 15, 2025.

Tesla has approximately 3.2 billion outstanding shares (with Elon's 410,794,076 shares being 12.8% of the total). Thus, 1% equals ~32 million shares per tranche, or 384 million shares total if all tranches vest.

At a current share price of ~$342 ($1.1 trillion market cap ÷ 3.2 billion shares), each tranche is worth ~$11 billion, totaling ~$131 billion if fully vested (though this value will fluctuate with stock price).

Market Capitalization Milestones

Starting Point: Tesla’s current market cap is $1.1 trillion.

Target: Reach $5 trillion by 2035, with milestones increasing in $333 billion increments (to evenly distribute across 12 tranches).

Measurement: Based on a 6-month trailing average and a 30-day trailing average of Tesla’s stock price (trading days only), consistent with the 2018 plan.

Milestones:

Tranche 1: $1.333 trillion

Tranche 2: $1.666 trillion

Tranche 3: $2.000 trillion

Tranche 4: $2.333 trillion

Tranche 5: $2.666 trillion

Tranche 6: $3.000 trillion

Tranche 7: $3.333 trillion

Tranche 8: $3.666 trillion

Tranche 9: $4.000 trillion

Tranche 10: $4.333 trillion

Tranche 11: $4.666 trillion

Tranche 12: $5.000 trillion

Operational Milestones

Requirement: For each tranche to vest, Elon must achieve 1 Market Capitalization Milestone and 1 Operational Milestone (dual-trigger). Full vesting requires achieving 12 of 16 operational milestones alongside all market cap goals.

Categories: Revenue and Adjusted EBITDA, reflecting Tesla’s growth in EV, autonomy, and robotics.

Baseline (2024):

Revenue: ~$97 billion (Tesla’s 2024 revenue, per recent reports).

Adjusted EBITDA: ~$14 billion (achieved in 2022–2023, per historical data).

Targets: Set to reflect ~15x revenue and ~21x Adjusted EBITDA growth over 10 years, mirroring the 2018 plan’s ambition (which used 2017 levels as a baseline).

Revenue Targets (15x $97B = $1.455 trillion, distributed across 8 milestones):

$150B, $250B, $350B, $500B, $650B, $800B, $1T, $1.5T

Adjusted EBITDA Targets (21x $14B = $294 billion, distributed across 8 milestones):

$20B, $35B, $50B, $75B, $100B, $150B, $200B, $294B

Measurement: Cumulative over four consecutive fiscal quarters, as in the 2018 plan.

Additional Conditions:

Holding Period: Elon must hold shares for 5 years after exercising options, ensuring long-term alignment with shareholders.

Clawback Provision: Options are subject to clawback if Tesla restates financials filed with the SEC, as in the 2018 plan.

Role Requirement: Elon must remain CEO, Executive Chairman, or Chief Product Officer for the duration, with the CEO reporting to him if he steps down from that role.

Adjustments: Market cap and operational milestones will be adjusted for significant acquisitions, spin-offs, or divestitures to ensure fairness.

Rationale:

Market Cap Goal: A $5 trillion target positions Tesla as a top global company (Microsoft and Apple are ~$3+ trillion). This aligns with Elon’s vision of Tesla reaching a $30 trillion valuation through robotics and autonomy, though this sets a more conservative 10-year goal.

Operational Goals: The 15x revenue and 21x EBITDA growth targets mirror the 2018 plan’s ambition, reflecting Tesla’s shift toward AI (e.g., robotaxis, Optimus) and energy solutions. Revenue of $1.5 trillion and EBITDA of $294 billion are aggressive but achievable if Tesla captures significant market share in autonomy and robotics.

Risk and Reward: The dual-trigger structure ensures Elon is rewarded only if Tesla grows both in valuation and fundamentals, protecting shareholders from speculative stock price inflation alone. The lack of salary or guaranteed equity keeps Elon’s compensation tied entirely to performance.

This plan incentivizes Elon to drive Tesla toward becoming a multi-trillion-dollar AI and robotics leader, while ensuring shareholders benefit from sustainable growth.

Note: this plan doesn't correct/address any injustice from striking the 2018 plan.