Sabitlenmiş Tweet

The end of the war is being delayed: Who will be pushed back to the Stone Age?

Last night’s speech by Donald Trump was essentially a repeat of everything we’ve been hearing so far — along with yet another promise of a total defeat of Iran within the next “2–3 weeks.” Talk of negotiations has disappeared. Global energy markets reacted as expected — prices surged again today. The end of the crisis is nowhere in sight, and the last tankers (except Iranian ones, which never stopped) that left the Gulf have already reached their destinations. A new wave isn’t coming anytime soon. The world should prepare for physical shortages.

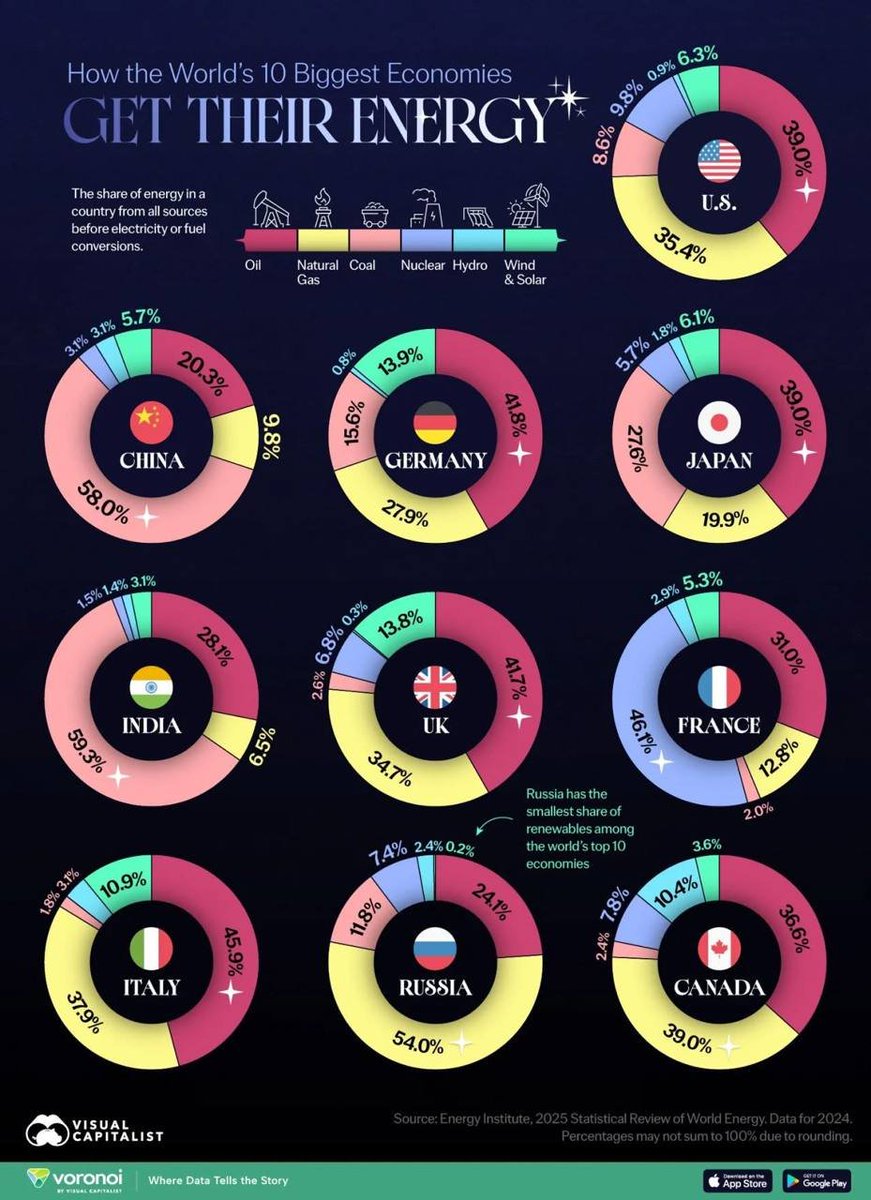

Using a powerful visualization from Visual Capitalist, showing the energy mix of the 10 largest economies in 2024, a few things stand out clearly:

Oil and natural gas play a dominant role across all major economies. Only in China and India do coal surpass them, while nuclear dominates in France.

The structure of the energy mix isn’t heavily influenced by import/export balances, especially in open Western economies (including Russia and Japan). Only China and India are aggressively maximizing domestic resources — coal.

Only the U.S., Canada, and Russia are net exporters of energy and fuels. It’s no coincidence oil and gas dominate their mix. In a prolonged Gulf crisis, they naturally become the biggest beneficiaries. Trump keeps repeating that closing the Strait isn’t his problem — and he has real grounds for saying so.

China is a major importer of oil and gas but has massive reserves and enormous capacity to convert coal into fuels, chemicals, and fertilizers. China is prepared for what’s happening and will feel the pain last. India, despite its coal, is far more vulnerable — physical shortages are already appearing.

Italy, Germany, and France are among the most exposed in a prolonged conflict. They import around or over 95% of their oil and gas. The UK has slightly more domestic production but is also a major net importer. Worse, these economies lack sufficient refining capacity, leaving them vulnerable not just to crude shortages but to finished fuels as well. Gas storage is depleted after winter. The only good news: they currently hold about 3 months of petroleum product reserves — for now, no physical shortages. This applies to almost the entire EU.

Japan is also highly dependent on imports but can relatively quickly restart nuclear plants, switch from gas to coal, and source oil and gas from Russia, Australia, and Canada.

Despite political support and trillions in investments, renewables (including hydro, solar, and wind) still play a relatively minor role in the overall energy mix. Even in Germany and the UK, they barely exceed 10%. Claims that renewables will “save the day” are, at this stage, unfounded.

If the U.S. is truly aiming to send Iran “back to the Stone Age” by destroying its energy infrastructure, the war will likely drag on, and Gulf exports won’t recover anytime soon. The first direct casualties will be energy-importing countries in Southeast Asia — among major economies, India stands out. Next will be poorer nations (with no strategic reserves) and countries like Australia, New Zealand, and Taiwan, all heavily dependent on Gulf exports. Europe will feel the shock later — but when it does, the impact will be severe.

And remember: about a year ago, Brussels agreed to purchase $750 billion worth of oil, gas, nuclear fuel, LNG, and semiconductors from the U.S. over three years. At the time, most of us dismissed this as unrealistic due to insufficient demand. But at $200 oil and €200/MWh gas, those numbers suddenly look achievable — and not at all unrealistic if the Strait of Hormuz remains closed for another month.

That’s the situation.

English