Cheng

798 posts

Cheng

@ChengTrading

Long term holder of $BW Babcock & Wilcox Enterprises Information shared on this account does not constitute financial advice. DYOR.

Katılım Ocak 2021

831 Takip Edilen245 Takipçiler

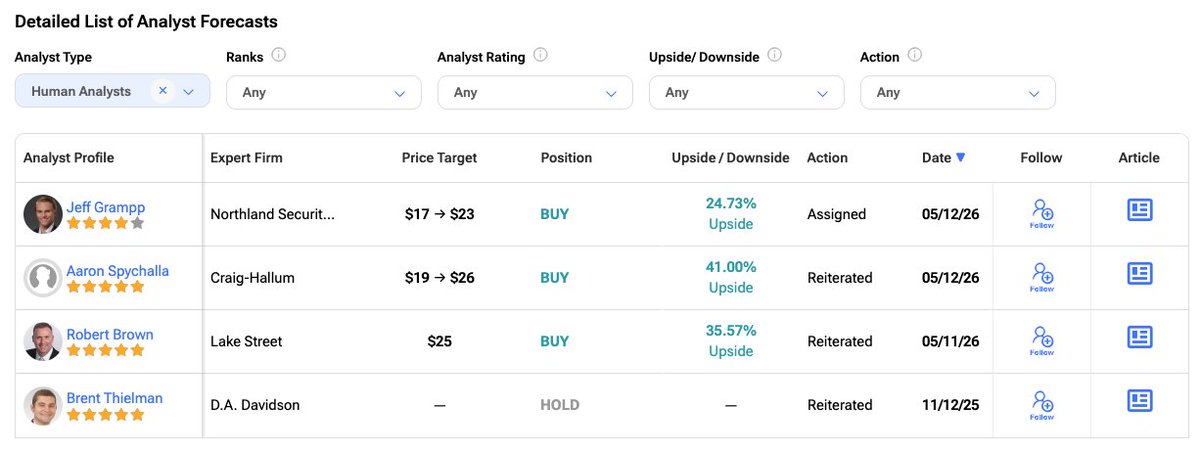

$BW Babcock and Wilcox Enterprises Inc

Jeff Grampp from Northland Securities freshly assigned a Buy rating yesterday (05/12/26), raising his price target from $17 to $23, implying 24.73% upside from the last price of $18.36. A new assignment signals Northland is initiating formal coverage of the stock.

Aaron Spychalla from Craig-Hallum reiterated his Buy on the same day (05/12/26), lifting his price target from $19 to $26 the highest target on the street reflecting 41% upside. Craig-Hallum has been one of the more bullish voices on the name.

Robert Brown from Lake Street reiterated his Buy a day earlier (05/11/26), holding his $25 price target steady, implying 35.57% upside. Lake Street confirmed conviction ahead of the earnings call.

The consensus picture: 3 Buy, 0 Hold, 0 Sell among active analysts, with an average price target of $24.67 representing 34.35% upside from current levels. The fact that two firms raised their targets on the day of or after Q1 earnings suggests the results gave analysts additional confidence rather than reason for concern.

D.A. Davidson's Brent Thielman remains on Hold from November 2025 but has not updated his rating since.

English

@ChengTrading I think a capital increase will be carried out before a licensing deal is secured

English

Smoltek $SMOL Annual general meeting today May 12, 2026

No surprises. No dividend. Board re-elected unchanged.

The one thing to note: the board is now authorized to issue shares, warrants & convertibles without shareholder approval until the next AGM up to 723M shares, vs. today's 180M. Significant dilution risk for current shareholders.

The AGM doesn't change the thesis in either direction it's a holding pattern. The technology de-risking (2,000-hour life test) is the real story, and the authorization suggests management is positioning for a capital raise, likely tied to the next step in commercialization. The next truly catalytic event remains a named commercial deal or a concrete licensing announcement.

English

Nobody knows the timing that´s the honest answer. The 2,000hr life test extension by an unnamed major manufacturer is encouraging, but there's no deal yet. The technology is real and de-risking fast. But a capital raise looks imminent, which could push the share price down before any deal is announced.

I cannot tell you if its worth buying. Investing involves risk, including the potential loss of capital. The information shared is for informational purpose only and does not constitute financial advice.

English

@ChengTrading When will the license agreement be announced? Is it still worth buying?

English

Institutions holds 73,58% and insiders 3,51% of the total shares of Babcock & Wilcox. $BW

Cheng@ChengTrading

$BW I have never checked which institutions own Babcock & Wilcox until now

English

Jeff Currie @CommodMkt, a renowned commodities economist and strategist, is now on X and is a must-follow.

English

$BW Babcock & Wilcox Enterprises’ quarter ended March 31, 2026 showed much stronger revenue but a sharply higher loss. Revenue rose to $214.4 million from $148.6 million, driven mainly by large project activity, including $31.0 million from the new Base Electron power plant contract linked to AI‑driven electricity demand.

Despite the top-line growth, the company reported a loss from continuing operations of $79.6 million, compared with $15.6 million a year earlier. The wider loss was largely due to a non‑cash $70.2 million increase in the fair value of customer warrants tied to Applied Digital/Base Electron as the share price rose, plus higher stock‑based compensation and tax expense. Excluding these and other adjustments, Adjusted EBITDA improved to $16.1 million from $4.0 million, reflecting stronger underlying project performance.

Cash, cash equivalents and restricted cash totaled $194.8 million, and management states that substantial doubt about the company’s ability to continue as a going concern has been alleviated. Backlog reached $2.7 billion, with revenue expected over multiple years, while stockholders’ deficit stood at $172.1 million and total liabilities at $929.9 million.

English

No account should be under 1K followers

Say hello, I will boost you

English

Back-of-envelope numbers for 1 gigawatt data center:

All-in Capex: ~$50 bn

Enterprise revenue generated: ~$25-30 bn/year

Electricity cost: $1-2 bn/year

~2 year payback.

The boom is real.

English

I take pride in the fact that I don’t talk about 200 stocks a year. Conviction matters. I share deep research on 15-20 names a year. The market is about how much money you make when you’re right, and how much you lose when you’re wrong. Not about how many good “ideas” you have.

English