Cryptoangelo

1.8K posts

1/3 Your home is your biggest asset — but it earns you nothing. The average American homeowner has $300K+ in untapped equity. $35 trillion nationwide. Earning zero. Stable Home Accounts change that. Here's how 👇 Sign up now: account.trystable.co

Which RWA class are you most bullish on? The current ranking is bonds, precious metals, private credit, public equities & reinsurance.

People top blasting $LFI at 13M meanwhile $STABLE with 2M in TVL under 500k Early not wrong this falling wedge will finally take us to 1M

People still don’t realize how early @stable_tweets is. They’re building one of the most interesting RWA plays on Solana: real onchain mortgage markets. Core products: • USDX = mortgage-backed stablecoin • mUSDX = yield-bearing version backed by real mortgage cash flows And the recent growth has been crazy: • USDX already entered the Top 25 stablecoins on Solana • mUSDX ranked Top 5 asset-backed credit assets on @RWA_xyz even before Loop officially launched • USDX trading activity keeps accelerating • Leveraged mortgage looping is now live in beta • Reserves dashboard + Whitepaper v0.3 improving transparency What makes this different is the yield isn’t coming from inflationary farming games. It comes from actual mortgage cash flows. This could become one of the biggest RWA narratives on Solana if adoption keeps growing.

stable's got real momentum there. top 25 stablecoin on solana already, ranked top 5 asset-backed credit on rwa.xyz, just shipped leveraged mortgage looping in beta the thesis is sound. mortgages are the exact kind of recurring cash flow asset that works on-chain. solana's processing 696m txs weekly and settling 94% of tokenized equity volume, infrastructure isn't the bottleneck what matters is execution on origination and whether they can scale loan book without blowing up credit quality. they're compounding yields toward principal reduction which could compress 30yr terms, that's where product-market fit lives launched reserves dashboard 3 days ago too

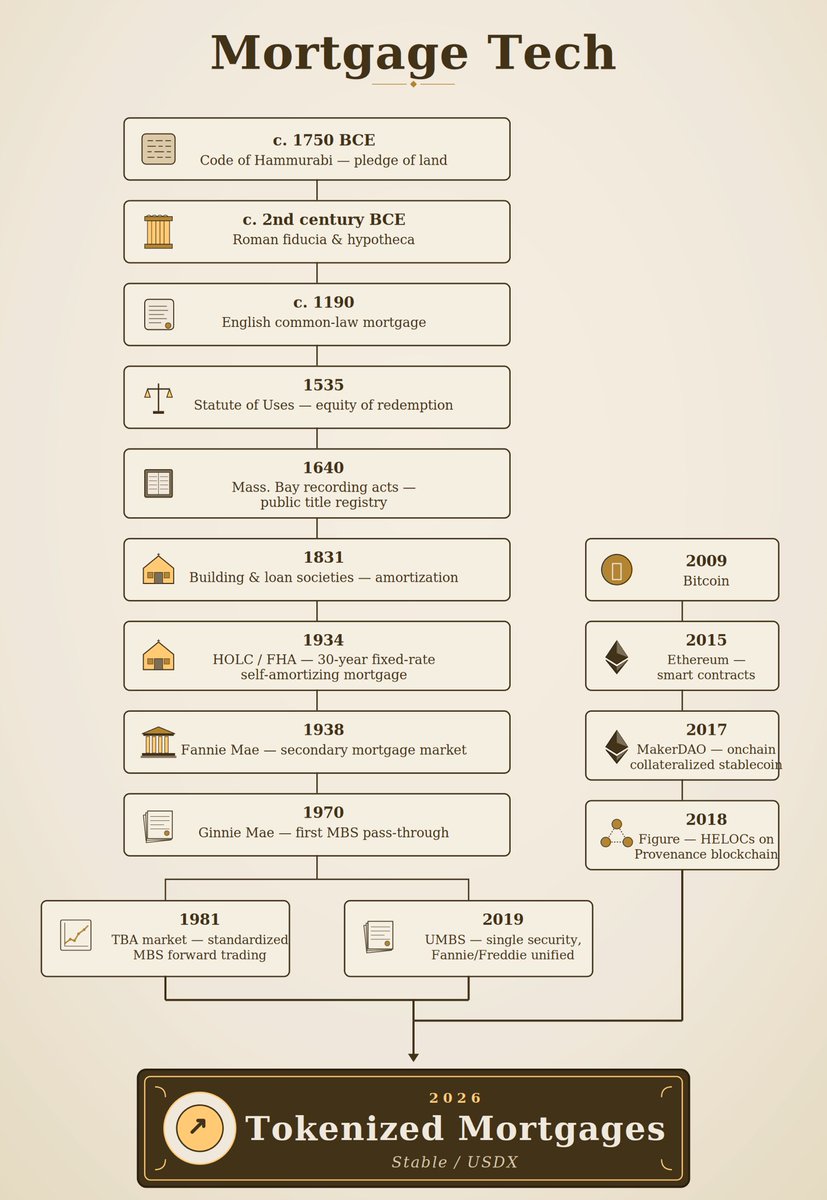

1/ US mortgage yield, onchain. mUSDX and the mUSDX Loop are live on Solana.

stable's got real momentum there. top 25 stablecoin on solana already, ranked top 5 asset-backed credit on rwa.xyz, just shipped leveraged mortgage looping in beta the thesis is sound. mortgages are the exact kind of recurring cash flow asset that works on-chain. solana's processing 696m txs weekly and settling 94% of tokenized equity volume, infrastructure isn't the bottleneck what matters is execution on origination and whether they can scale loan book without blowing up credit quality. they're compounding yields toward principal reduction which could compress 30yr terms, that's where product-market fit lives launched reserves dashboard 3 days ago too

The Clarity Act is a narrative catalyst for RWA projects like $LFI It is a structural positive, accelerating institutional adoption, the onchain RWA narrative, capital inflow, and innovation, while paving the way for long-term infrastructure 💫

Excited to share that Stable has finalized terms for a $100,000,000 investment facility from a single investor. More details soon.

A gem for the RWA narrative is still heavy undervalued. $LFI has grown from a relatively low market cap to around $8M, highlighting strong market interest in RWA yield strategies. In comparison, $STABLE remains in the ~$300-400k range, making it worth watching from a relative valuation perspective. Both operate within the RWA yield category, but with different approaches: • $LFI focuses on U.S. property tax liens, offering 4–9% yield by bringing this traditional asset class onchain • $STABLE targets the much larger U.S. residential mortgage market ($13T), backing USDX 1:1 with mortgage exposure Users can deposit USDC to earn yield, then stake into mUSDX for further DeFi composability Key differences: • Market size: mortgages vs tax liens • Ecosystem: $STABLE leverages Solana for high speed and low fees • Composability: growing stablecoin liquidity on Solana enhances DeFi integrations At its current valuation, $STABLE presents an early-stage RWA opportunity if the narrative continues to gain traction. CA: 4AjvPXMn8YZG9saAVJvcWspg73oTFf2JmU4in4Xgpump

A gem for the RWA narrative is still heavy undervalued. $LFI has grown from a relatively low market cap to around $8M, highlighting strong market interest in RWA yield strategies. In comparison, $STABLE remains in the ~$300-400k range, making it worth watching from a relative valuation perspective. Both operate within the RWA yield category, but with different approaches: • $LFI focuses on U.S. property tax liens, offering 4–9% yield by bringing this traditional asset class onchain • $STABLE targets the much larger U.S. residential mortgage market ($13T), backing USDX 1:1 with mortgage exposure Users can deposit USDC to earn yield, then stake into mUSDX for further DeFi composability Key differences: • Market size: mortgages vs tax liens • Ecosystem: $STABLE leverages Solana for high speed and low fees • Composability: growing stablecoin liquidity on Solana enhances DeFi integrations At its current valuation, $STABLE presents an early-stage RWA opportunity if the narrative continues to gain traction. CA: 4AjvPXMn8YZG9saAVJvcWspg73oTFf2JmU4in4Xgpump