Sabitlenmiş Tweet

Most people try to budget by tracking every dollar they spend.

It's exhausting. And it usually doesn't stick.

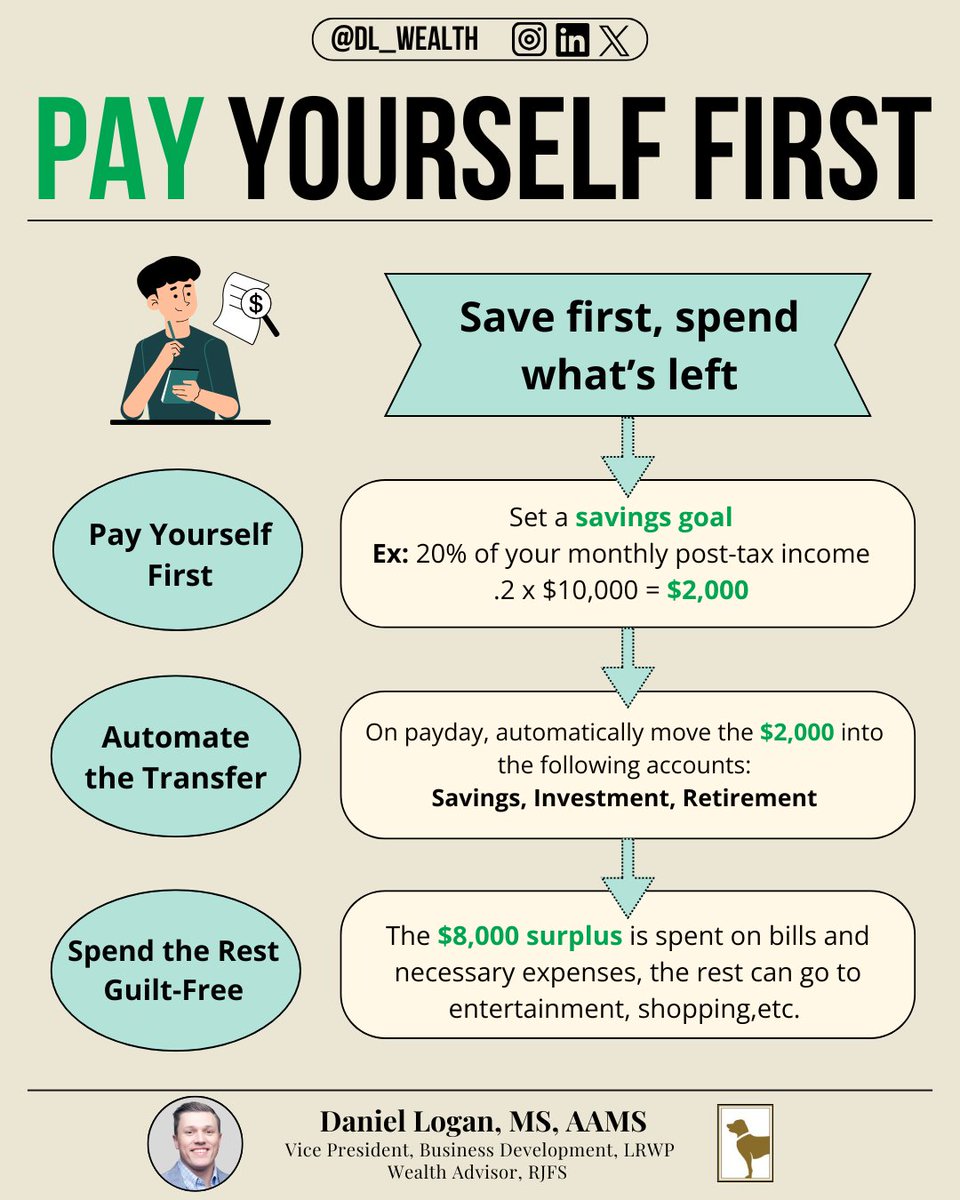

Reverse budgeting flips the script...

Instead of tracking what you spend, you automate what you save first. Then spend the rest guilt-free.

Here's how it works

1.) Identify your savings goals upfront. Retirement, brokerage, real estate, whatever matters to you.

2.) Automate contributions on payday.

3.) Spend what's left how you want.

No spreadsheets. No guilt. No micromanaging.

The simplest financial habit change you can make.

English