Dabburi ✨Special 26✨

5K posts

Dabburi ✨Special 26✨

@DSR26S

Stock Market Learner Forever | Fundamental Analysis | Technical Analysis | Price Action | Volume | Open Interest | Momentum Investment .

Hyderabad Katılım Mayıs 2010

317 Takip Edilen651 Takipçiler

Good one, try to understand.

Suresh K@SureshKBN

how kirlpnu connected to coal gasification FY28-FY30

English

Worth knowing ....

Rohan Tantia@rohantantia

India’s Data Center Supercycle - Full Value Chain Play!! 👉This isn’t just about data centres - it’s a ₹10L Cr+ capex cycle across 10 layers 👉AI → Data Centres → Power → Grid → Equipment → Cooling → Cables → Connectivity → Compute → Software 👉This is not one sector - it’s a multi-layer industrial + tech supercycle 👉Follow the value chain, not just data centre operators → The real winners are spread across infra, manufacturing & tech 👉Follow @rohantantia for more deep dives!! Bookmark it for future reference!! 👉Checkout the below quoted tweet for each layer deep dive Disclaimer: Do not consider it as a buy/sell recommendation, just for information!! Do your own due diligence. #StocksToWatch #StocksInFocus #StockMarketIndia @DhawalDoshi5 @vishan_29 @TrendSpark420 @Anvith_ @Dynamicinvstr @Prabinmen

English

@parksmarthq : Do you bother the accounting frauds that your employees are doing ?

Its high time for you to look into the accounting frauds and the sufferings customers are facing.

All illogical practices and pathatetic explnations.

@iamvishvasharma your attention appreciated.

English

@Parksmart : You really worry about the Accounting Frauds that your employees are doing ?

I am one of the victims of your employee's accounting frauds.

They collected money n giving cooked up stories about the accounts and the quality of the work.

Its a shame on you.

English

Good info.

Shreenidhi P@nid_rockz

Covering few high growth companies concall highlights that were conducted over over the last 3 days #Q4FY26 #UshaMartin #RRKabel #KajariaCeramics #Emmvee #Acutaas Usha Martin #UshaMartin Q4FY26 was a historic quarter with big margin expansion Highest ever revenue, EBITDA, PBT and PAT in comps history Highest ever margins At 21.6% vs 15.6%⏫600bps Value added mix improving Should continue similar momentum for FY27 Margins are structurally changing to higher range/bands Confident to maintain high margin levels Increased OPM guidance from 18-19% to 20%+ going forward Debt reduced from 337cr to 145cr Steep reduction 457cr FCF generation Rope capacity utilization at 75% Wires at 78% Guides to do 12-14% volume growth for FY27 with better margins RR Kabel #RRKabel Historic quarter Highest ever revenue, EBITDA, PBT and PAT in comps history Rev and EBITDA ⏫35%+ 10% volume growth for Q4FY26 16% volume growth for FY26 FY27 volume growth target of 16-18% for wores and cables segment 100 bps margin improvement guidance annually for next 2 years Targetting 10.5% OPM in FY28 1200cr capex between FY26-28 16-18% volume growth guidance is too good given the kind of geopolitical challenges that's prevailing at present Kajaria ceramics #Kajaria #KajariaCeramics 11% volume growth in Q4FY26 Volume growth after so many trpid quarters Margins expand exponentially Expects margins to remain in higher range vs last 8 qtrs OPM at 19% vs 10% PAT at 156cr⏫266% WC days improved by 14 days to reach 51 days Better inventory management Approved capex for Srikalahasti facility To increase annual production by 10 million sq mts Strong demand momentum witnessed since Jan 2026 Saw good traction even for April Gas price related challenges Some regions seeing 12-17% hikes Guidance to outperform industry growth for FY27 OPM expected to stay at 17-18% range 300cr buyback at 1380/share approved Emmvee Photovoltaic Power #Emmvee Highest ever revenue, EBITDA, PBT and PAT in comps history Holds on to 33% OPM 100% TopCON 10.3 GW module capacity 9.4 GW orderbook 16.3 GW module and 8.9 GW cell capacity by FY28 De-leveraged well through 1621cr debt reduction Acutaas Chemicals #Acutaas Previously,Ami Organics Highest ever revenue, EBITDA, PBT and PAT in comps history Rev⏫40% at 433cr PAT ⏫114% at 134cr OPM at 42% vs 28% OCF ⏫147% at 292cr Confident to deliver 25%+ topline for FY27 over FY26 CDMO: 1000cr rev guidance by FY28 Net cash balance sheet WC increased slightly from 114 days to 120 days

English

Good Info

Sector Research 🩵@SECTOR_RES0123

Growth Triggers 👇 🔹#TDPower – Data center/export-led generator demand; OB ₹1,845 Cr; new plant + strong FY27 visibility 🔹#QualityPower – Grid capex + HVDC push; Sangli expansion (₹1,500 Cr potential) + JV scale-up 🔹#ShilcharTech – Renewable transformer demand; full utilization + expansion by FY27 🔹#MTAR – AI/data center fuel cells + nuclear/defense; OB ₹2,395 Cr, strong order momentum 🔹#Kaynes – EMS + semiconductor play; OB ₹9,072 Cr; OSAT ramp underway 🔹#Netweb – AI/HPC boom; strong strategic orders + 30–40% growth visibility 🔹#ZenTech – Defense indigenization; anti-drone + simulators; OB ₹1,427 Cr 🔹#DataPatterns – Radar/EW systems; OB ₹1,868 Cr + strong pipeline 🔹#PTCIndustries – Aerospace/defense alloys; global tie-ups (Blue Origin, Honeywell) 🔹#E2ENetworks – GPU cloud/AI infra; hyper growth + high margins 🔹#InoxIndia – LNG/cryogenic exports; diversified global demand 🔹#FrontierSprings – Railways capex play; strong order visibility + capacity ramp

English

Dr Vismaya VR ✨Enigma✨@Vismaya9999

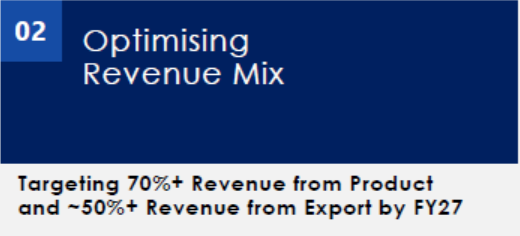

🏛️ HFCL Q4 FY26 Results: Stellar Results 🔥🔥🔥 🔖 YoY (Q4 FY26 vs Q4 FY25) ⬆️ Revenue: 1,824 Cr vs 801 Cr (+127.81%) ⬆️ PBT: 228 vs -105 Cr (+317.14%) ⬆️ PAT: 184 vs -83 Cr (+321.44%) ⬆️ PAT Margin: 10.11% vs -10.40% (+2051 bps) ⬆️ EPS: ₹1.21 vs ₹-0.56 (+316.07%) 🔖 QoQ (Q4 FY26 vs Q3 FY26) ⬆️ Revenue: 1,824 Cr vs 1,211 Cr (+50.66%) ⬆️ PBT: ₹228 Cr vs 138 Cr (+65.04%) ⬆️ PAT: ₹184 Cr vs 102 Cr (+80.18%) ⬆️ PAT Margin: 10.11% vs 8.45% (+166 bps) ⬆️ EPS: ₹1.21 vs ₹0.67 (+80.60%) 🔖 FY26 Full Year ⬆️ Revenue: 4,949 Cr vs 4,065 Cr (+21.75%) ⬆️ EBITDA: 827 Cr vs ₹507 Cr (+63.12%) ⬆️Margin: 16.70% vs 12.47% (+423 bps) ⬆️ PAT: 329 Cr vs 173 Cr (+90.12%) ⬆️Margin: 6.66% vs 4.26% (+240 bps) ⬆️ EPS: ₹2.13 vs ₹1.23 (+73.17%) 🔖 Margin Context (QoQ dip) EBITDA margin dipped 164 bps QoQ (18.47% but not alarming) Because 👇🏻 EPC revenue jumped from 488 Cr to ₹587 Cr EPC EBIT was -₹84 Cr, dragging blended margin Employee costs - from 108 Cr to 137 Cr (+₹29 Cr) for year-end hiring, defence team expansion, bonus accruals Material costs - from 408 Cr to 630 Cr - natural consequence of 51% revenue scale-up, not pricing pressure ✅ Absolute EBITDA grew 38% QoQ. Structure intact. 🔖 Key Business Updates 📦 Order Book 21,206 Cr (3x from ₹7,010 Cr in FY23) includes 4.3x revenue cover; ₹12,248 Cr from exports 🌐 OFC Order Book Record 13,483 Cr - strongest visibility in company history 💡 Largest Single Export OFC Order 10,159 Cr multi-year deal secures ~50%+ OFC capacity over medium term 🔩 Preform CapEx 580 Cr backward integration - lower imports, better margins, cost efficiency; 310 MT/annum by July 2029 🏭 OFC Capacity 34 mn fkm to 43 mn fkm by June 2026 and OF capacity 28 mn fkm to 33.9 mn fkm by Dec 2026 🔁 Global Fiber Upcycle Structural demand from hyperscalers, AI workloads & cloud infra - strong demand from US, Europe & Asia 📱 Telecom Products India’s first indigenously developed 5G FWA CPE; leadership in Wi-Fi APs & UBRs; MPLS routers deployed 🔀 Demerger Plan - Big positive 👍 Three independent listed entities - Telecom (OFC/Products), Defence & EPC. Each vertical to unlock independent valuation; Defence listing a potential re-rating trigger as serial production scales 🖥️ HTL Subsidiary (Data Centre Interconnect) Revenue expected 400 Cr in FY27 to 800 Cr in FY28 ✈️ Aerospace MoU Proposed acquisition brings 1,930 Cr confirmed export order book Defence manufacturing groundbreaking in AP on May 15, 2026 💰 Promoter Warrants 555 Cr warrants done at ₹74/share - conviction signal, not dilution; funds preform plant + defence expansion 🎯 FY29 Targets Revenue 10,000 Cr+ and EBITDA Margin 20-21% Revenue Mix Shift - Products at 62% in FY26 to targeting 70%+ in FY27; Private sector revenue at ~84% 🌍 Exports 41% of FY26 revenue (vs 12% in FY25); targeting 50%+ from FY27 ⚠️ Watch Points Inventory up 58% YoY (₹1,416 Cr) Negative OCF (₹-378 Cr) despite strong PBT - but working capital tied to order execution ramp Finance costs elevated at ₹242 Cr for FY26 #HFCL #Q4FY26 #Q4Results #Vismaya

English