Sabitlenmiş Tweet

For compliance purposes, I’ll no longer be posting.

DMs open if you want to stay in touch, chat ideas, short theses that hinge on SBC/D&A accounting, best Lil Wayne mixtapes, etc.

+Obligatory blurry pic of the dog

English

Danny Ocean

6K posts

@DannyOcean555

FCF per share | Slowly slipping down the quality spectrum

PRMB Didn’t hit the soft guide of +ve customer adds in December, but at this px (8x EBITDA), (improving) directionality is probably what matters H1 likely will have added integration spend (SAP & WMS), so hope is that’s offset w/ improvement elsewhere- E.g.: truck loading recovering from horrible 80% efficiency (?) to the standard 99% that aids in realizing route density, not having to deal with angry, churning customers, etc So, mgmt’s story / street algo is back to very modest +ve topline in ‘26 on volume recovery/minimial px + easy comps w/ slight margin improvement Ideally, integration is less of a headwind & mkt looks out to ‘27 on normalized LSD growth (x-sell, other advantages of scale, Foss makes good & now able to take px) w/ more margin upside FCF’s always been the issue here (high capex + leverage =bad conversion), but leverage is surprisingly inoffensive now @ 3x & can see a more palatable 2.5x by EoY ‘26. +A promise of the tie up was less capex intensity (scale adv + PRMW stops doing dumb things like building nat gas fleets) Regardless, trajectory & out year picture continues to improve: Rerate ~$1.5B ‘26 EBITDA to 9x (I believe legacy PRMW traded around here or higher? Despite being a worse biz) >> $25 stock, 30% upside & potential for ~20% CAGR in ‘27+ w/ cash gen, bbk, & value accrual to eqy Bonus: comp coming market w/ Nestle’s water biz. Latest rumor was €5B @ 10x €500M segment EBITDA

I am always baffled by how investors always confidently think that they know better than management Lord give me the confidence of a 24 year old broccoli hair pod boy telling a memory CEO that his business is cyclical, because he read it in a BofA primer last tuesday

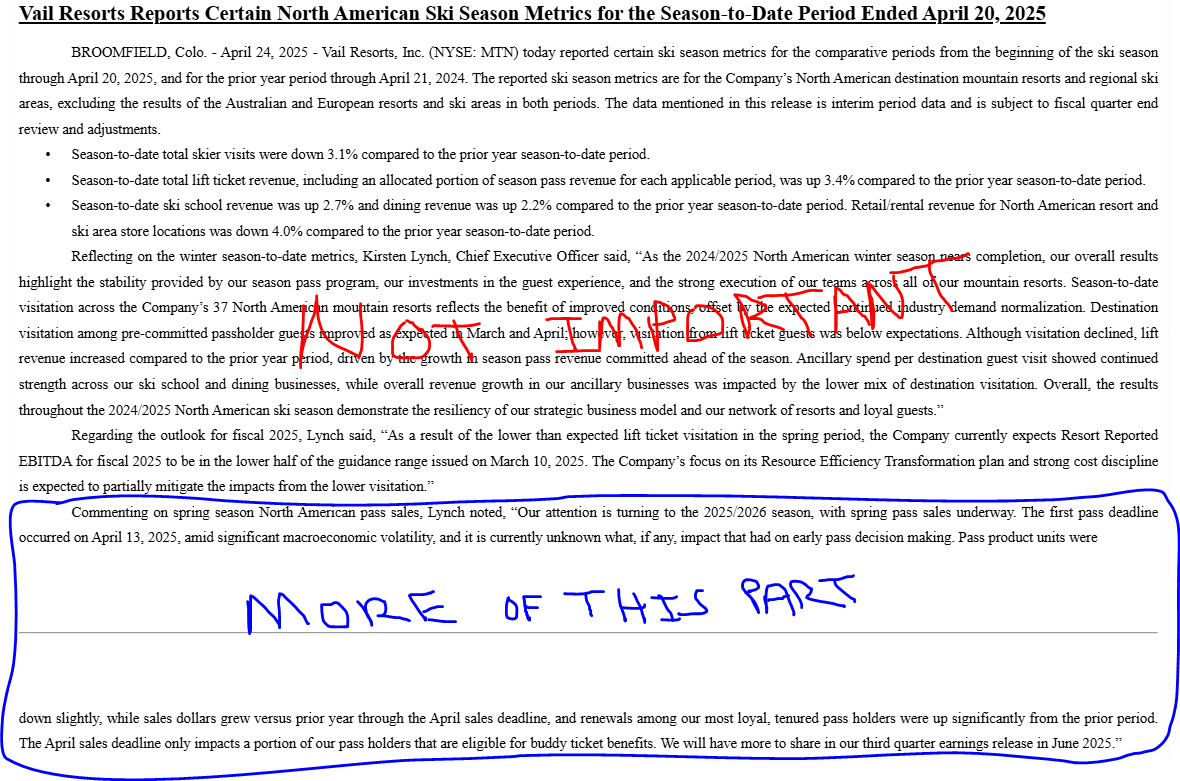

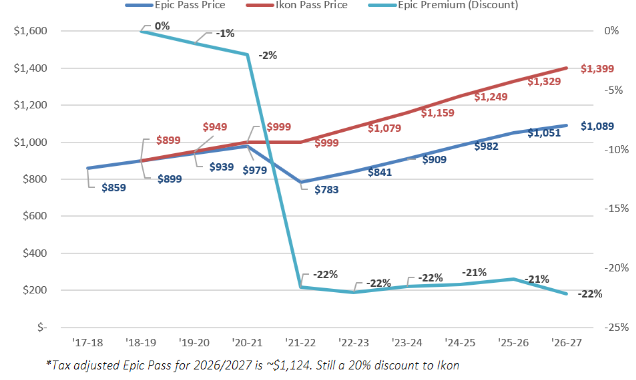

MTN Not quite the CableCo level of "we don't have customers, we have hostages"- But apparently not far off.