Sabitlenmiş Tweet

@mcdangerwood Also probably made an absolute bag this summer

English

Hugh Glass 🥋

3.7K posts

@Deerman1700

Hardcore gambler, Buffalo wing and draft beer fanatic, outdoor cranker, ex-potato farmer

Flying elbow drop onto 2 microwaves pt 9 ( WWE CM PUNK STYLE ) #superhumman #donttrythisathome #wwe

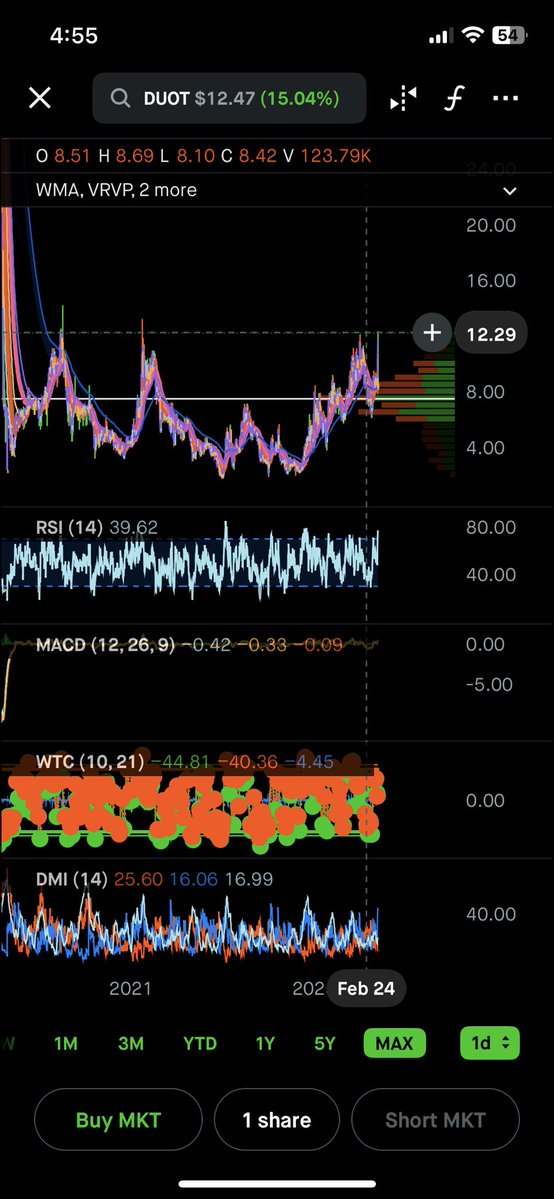

look at $DUOT 👇 A high-volatility AI infrastructure microcap trying to re-rate into a next-gen edge compute + industrial AI platform. Up ~60% in the past year, up ~100% over 3 years, but still swinging hard (-17% last 3 months, +20% last month) — classic early-stage revaluation phase. FINANCIALS: ~$27M revenue (2025) +271% YoY revenue growth ~$9.5M Q4 revenue (+548% YoY) 📈 GROWTH PROFILE: • Revenue growth Q: +547% • Full-year revenue growth: +271% • Forward growth guidance: +50%+ (2026 est.) 💰 BACKLOG / CONTRACT PIPELINE: ~$25.8M contracted backlog (year-end 2025) ~$12.4M expected to be recognized in 2026 ~$10M+ early traction from new Technology Solutions division 🚀 MAJOR AI INFRASTRUCTURE SHIFT: $DUOT is transitioning from legacy rail inspection systems into edge AI data center infrastructure (Duos Edge AI). Key pivot areas: • Modular Edge Data Centers (EDCs) • GPU hosting + GPU-as-a-Service (GPUaaS) • Industrial AI infrastructure deployments • High-density compute sites for latency-sensitive AI workloads 🔥 STRATEGIC PARTNERSHIPS: 🧠 $NVDA ecosystem exposure (indirect but critical) $DUOT’s entire new infrastructure buildout is centered around NVIDIA GPU clusters powering edge AI workloads, positioning it inside the broader AI compute supply chain. 👉 This effectively makes $DUOT a: “physical deployment layer for $NVDA -driven inference demand at the edge” 🤝 Hydra Host (2026) Commercial partnership to deploy high-density NVIDIA GPU clusters Includes GPU hosting + GPUaaS model Targeting a global tech customer deployment Initial ~4.3 MW colocation commitment Multi-site expansion planned Fully financed via ~$65M capital raise + hardware financing 👉 Largest edge data center project in company history 🌐 Seimitsu partnership Builds AI + fiber infrastructure integration in Georgia Combines high-speed fiber with modular edge compute nodes Targets healthcare, municipal, enterprise AI workloads Focus: low-latency distributed intelligence networks ⚡ FiberLight expansion Scaling edge data center deployment across Texas + U.S. regions Focus on underserved high-demand AI compute markets Enables physical rollout of distributed GPU infrastructure 🚀 Key catalyst: Hydra Host contract alone: ~$176M projected over 36 months ~$40M EBITDA potential annually at scale High-margin (~80% gross margin reported structure) Initial customer prepayment (~$18M) 🧠 BUSINESS MODEL SHIFT: DUOT is evolving from: Rail inspection / industrial vision systems Into: Edge AI infrastructure operator + GPU deployment platform Core thesis shift: from project-based hardware revenue to recurring AI compute infrastructure revenue 🏦 VALUATION CONTEXT: ~$271M market cap ~$27M revenue ~10x price-to-sales Forward PE elevated (~230, early-stage distorted earnings) All at 271m market cap. This like Buying $HON at 40$ in 2006