Gem

2.4K posts

@blakepickett Last summer I was pining 1mg 3 days a week of mt2 with no nausea

Now im pinning between 100-250mcg of mt1 and getting intense cramps for 30 minutes

English

just pinned glow + mt1 into my chest near some gnarly scar tissue

wonder if mt1 pinned IM will be easier on my stomach than subq

English

Don’t have a problem injecting most substances but I don’t understand doing MT2. MT1 + grass should get you a tan and less autism without mole debuffs and skin cancer

English

🚨 Holy shit... this Python library bypasses Cloudflare automatically and nobody's talking about it.

It's called Scrapling and it just killed every scraping tool you're currently using.

While everyone's duct-taping Selenium + BeautifulSoup + proxy services together and spending $500/month on CAPTCHA solving APIs...

This does all of it in one pip install. For free.

→ Cloudflare Turnstile and Interstitial bypass out of the box

→ Adaptive element tracking that survives website redesigns automatically

→ HTTP/3, TLS fingerprint spoofing, stealth browser, full Playwright — one API

→ Full spider framework with pause/resume checkpoints and real-time streaming

→ Built-in MCP server that feeds pre-extracted data directly to Claude/Cursor

→ 784x faster than BeautifulSoup on parsing benchmarks

The CAPTCHA solving industry built a $200M business on a problem this repo just made irrelevant.

100% Opensource.

(Link is in the comments)

English

@sunnyviljamaa No worries! I'm definitely not recommending anyone to go long on $SIVE.

I personally just found it extremely compelling like I did with $LITE last year. And I'm just sharing my thesis along the way in case others find it interesting

Thanks for the note of appreciation!

English

Just in: $SIVE announces major partnership with O-Net and Enablence for CPO.

Sivers will be the laser array supplier for CPO.

This is thesis validation in effect as $SIVE becomes InP CW DFB supplier for silicon photonics.

In simpler terms, this is the $LITE -> $FN relationship for current optical bottlenecks.

And mirrors the existing $POET -> $MRVL Celestial CPO supply chain, but in Asia.

Enablence makes the "Star Coupler", similar to $POET interposers.

O-Net is a massive assembler, that packages them for the finished module.

O-Net in HK is a supplier to companies like Huawei, ZTE, Ciena, Nokia, Fujitsu, and more.

Serenity@aleabitoreddit

$SIVE is now up +73.78% today ($231M MC). As markets price in information synthesis of the next potential $LITE of photonics. If I had to explain the difference: One laser source in Lumentum primarily benefits from current optical bottlenecks. The other in $SIVE is for the upcoming CPO/Silicon Photonic bottleneck. Lumentum is largely benefiting right now from $NVDA and hyperscalers securing capacity of EML lasers for current pluggable optical transceivers cycles. As seen with the current EML bottleneck, hyperscalers are buying out any 800G/1.6T transceiver + upstream capacity from: - $AAOI (in-house) - $COHR, $LITE (EML lasers + design) -> $FN (assembly) - $COHR, $LITE (EML lasers) -> Innolight / Eoptolink What's next? Silicon Photonics and Co-Packaged Optics. The architectural shift to CPO requires massive arrays of high-power CW DFB lasers. And this would likely trigger a complete, sudden paradigm shift in volume demand. $SIVE benefits from InP CW DFB lasers for SiPh and CPO: The up and coming companies like: $AYAR, $POET source $SIVE lasers, but primarily do advanced packaging. Then they feed up to larger companies like $MRVL Celestial (that buy $POET's interposers). However, if you go upstream, the light source is $SIVE. CW DFB lasers are light engine ( $SIVE ); the silicon photonics package ( $POET and others) is how it gets transmitted. CPO scale is not there yet. But we know it's coming. And as seen with current optical transceiver cycles: - Light sources from $LITE and $COHR demand much higher valuations than companies like $FN that focus on advanced packaging. Markets have been focusing on $POET, but missed where they get the actual $LITE type light source for Starlight. The risks are present including facing multi-source competition with $LITE, $COHR, $AVGO, and others. So again, make sure to do your own research. But my argument against that: Sivers been early enough to tailor custom lasers to fit $POET, Ayar, and other specifications before they got popular (sort like the $POET to $MRVL Celestial analogy). There's volume risks as well: But the potential Win Semi qualification offsets that. Dilution risk to scale capacity, is always present with every early-stage company as well. I did my thesis on $LITE last year and still love the stock for Google TPU ramp/OCS. But this year, I'm focusing on: $SIVE, as my personal CW DFB laser exposure for the new photonics architectural shift. I’m sharing my own thoughts on capturing the rotation from the current EML cycle to the upcoming CW DFB/Silicon Photonics cycle.

English

@charscrutton @nypost Anyone wonder why prostate cancer rate spike correlates with a massive under 30 finesteride uptake? Every dude is on it. You can get it prescribed in 5 min online.

English

New triple threat topical treatment fights hair loss better than finasteride and minoxidil trib.al/5wupebc

English

@TonyNashNerd Can't they just buy russian oil then? I heard putin won't send oil to Europe anymore so more for china

English

@endless_frank @antmillionsbot Can they just buy oil from russia then until war is over?

English

@antmillionsbot If China does anything stupid in Taiwan, the U.S military will blockade all oil leaving the Strait of Hormuz within hours and China’s economy will fall off an irreversible cliff with 0 access to energy.

So if I had to guess, I’d say they aren’t doing shit.

English

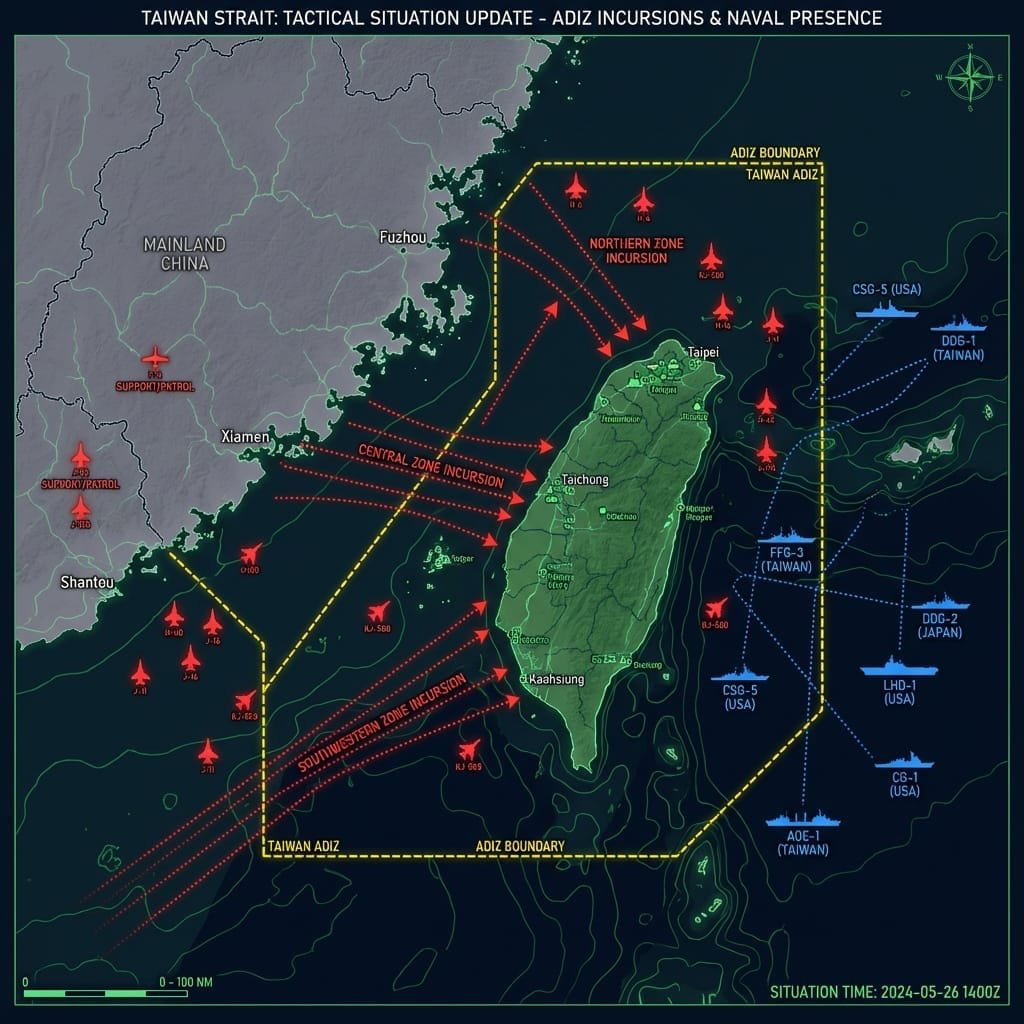

🚨🚨🚨 CHINA SURROUNDED TAIWAN WHILE AMERICA WAS FIGHTING IRAN. THE TIMING IS NOT A COINCIDENCE. 🚨🚨🚨

Yesterday, Taiwan's military detected 26 Chinese warplanes.

7 Chinese navy ships.

All circling the island at once.

This is the LARGEST military presence China has shown near Taiwan in weeks.

And it happened the exact same day the US announced more troops heading to the Middle East.

⚠️ Taiwan signed a $9 BILLION arms deal yesterday — scrambling before a March 15 deadline

⚠️ One of those arms packages — 82 HIMARS systems — expires on March 26

⚠️ South Korea quietly withdrew its THAAD missile defense because of Iran

⚠️ If China moves, North Korea could simultaneously threaten Japan and South Korea

Here is the logic chain that should terrify you:

China went quiet for 16 days near Taiwan → experts said "maybe peace" → then 26 planes returned yesterday → the lull was never peace → the lull was Xi waiting for the perfect window.

America is at war in the Middle East.

America's missile stockpiles are depleted.

America's Marines are in the Gulf.

And TSMC — the company that makes 90% of the world's advanced chips — sits on that island.

⚠️ If Taiwan falls, every AI company, every phone maker, every car brand on earth loses its chip supply

⚠️ One analyst called it: "S&P 500 down 50%" scenario

⚠️ The New York Times said it would "cripple the US economy"

The uncomfortable question nobody is asking:

If China moves this week, what exactly does America do with zero available military units and oil at $100?

This is the most dangerous geopolitical window since 2003.

Prepare accordingly. 🚨🚨🚨

English

English

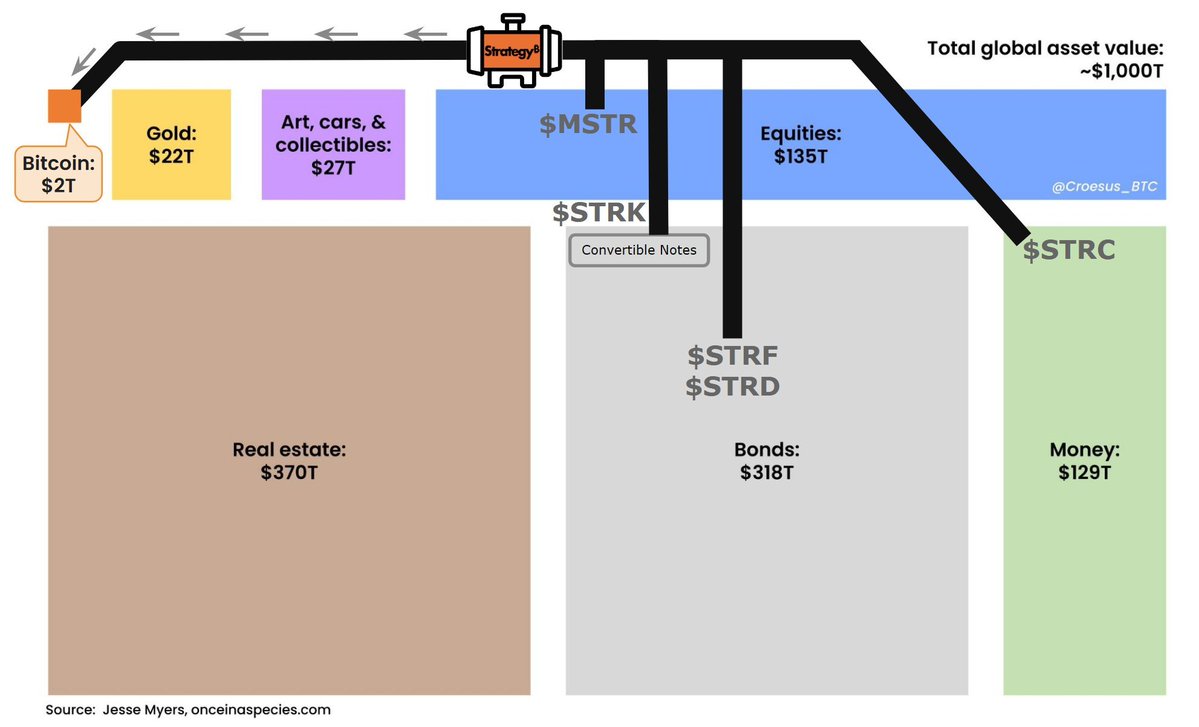

This is the biggest story in finance. Yet few are aware what's happening.

Strategy@Strategy

Record day for $STRC. $409M - Daily Traded Volume (highest ever) 3% - 30D Volatility (lowest ever) $99.78 - 1M VWAP (highest ever)

English

@Gubloinvestor Next one? Im always too late...

Can you post about your story from nobody to retired at 31?

English

Am at 95% cash with a few small tracking positions in $CF $MOS $PBF $GLEN $VNOM $BWLP

Dollar soars, everything else crashes. Maybe chemicals, refiners, energy can do ok.

R/R is as bad as ive seen it since Lib day, covid, Ukraine war.

Kuppy@hkuppy

1) Some thoughts on my book… It’s increasingly obvious that Trump convinced himself that taking out the top 100 guys in Iran would “fix” things there. It didn’t work. Plan B seems to involve bombing it to rubble. The issue is that by closing Hormuz, Iran has infinite negotiating leverage, and it’s pretty easy to keep Hormuz shut (Houthis did it in the Red Sea for 2 years)

English

I don’t think people are realizing that NOTHING in the global economy works at $120/Oil.

Nothing.

English

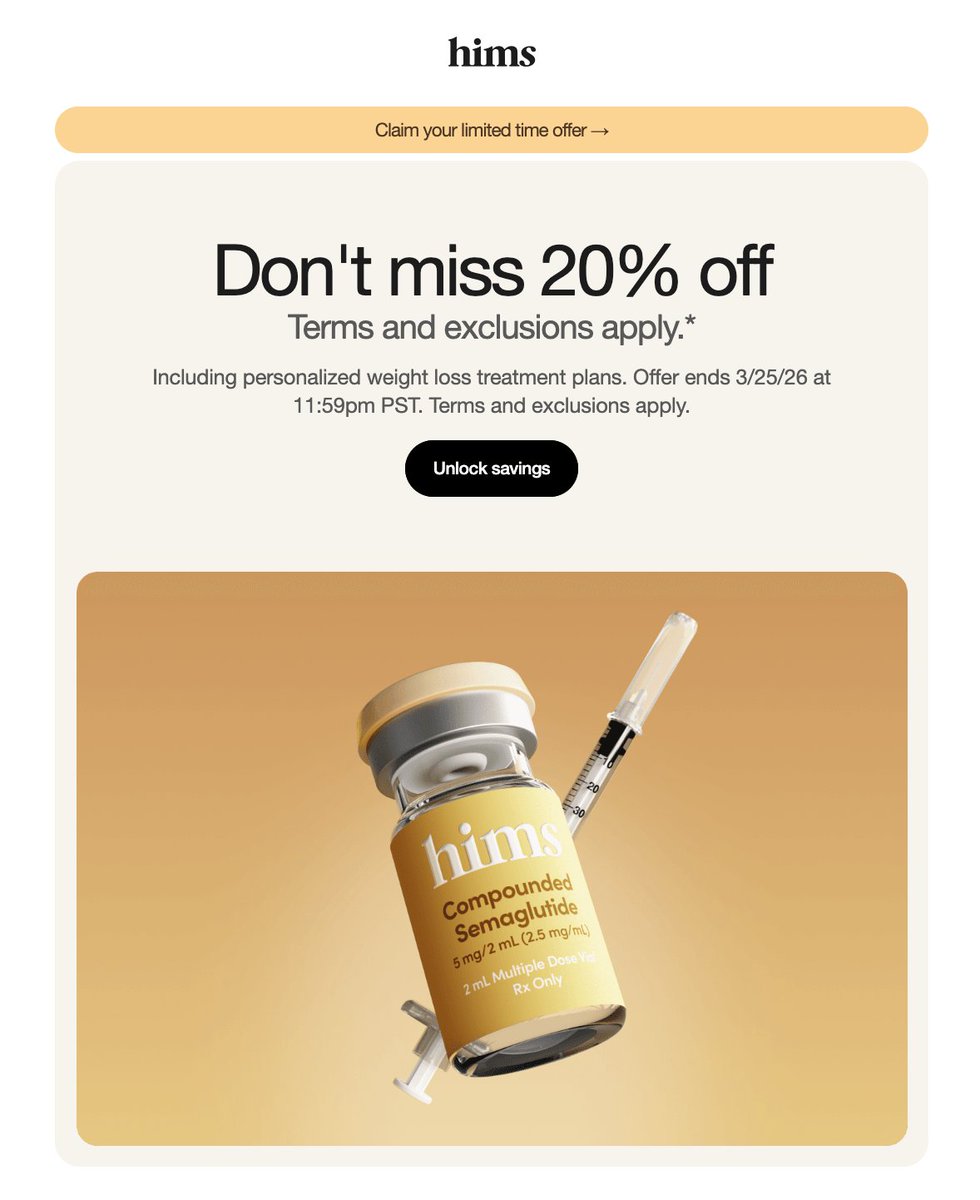

Seeing lots of speculation that $HIMS agreed to give up compounded GLP-1s in exchange for the deal with $NVO

Certainly possible!

But we still have zero details on the deal

And $HIMS is still sending 20% off marketing emails for compounded semaglutide and reaffirming the deal doesn't expire until March 25

If they plan to pull the product tomorrow, they're pushing it right up to the wire:

English

You beat everyone for the next 5 years with this:

US Market:

$ZETA

$UNH

$HIMS

$GOOG & $NVDA (after they correct)

CHINA:

$BABA

$BIDU

$JD

BONDS:

$TLT

EMERGING MARKETS:

$EWZ

$SE

$GRAB

CRYPTO:

$ETH

$BTC

EUROPE:

$ASML

$NVO

DIVIDEND:

$UPS

$PFE

DATA:

$NBIS

$AMD

$DELL

SAAS:

$NOW

$ORCL

BIO:

$TMDX

CONSUMER:

$LULU

$NKE

$ONON

FINTECH:

$SOFI

$NU

DISRUPT:

$OSCR

$HOOD

$ONDS

MOAT:

$ASTS

$ADUR

English