Sabitlenmiş Tweet

$POET live

CA: 4jnqfSMWE1opwNT9m98s5QFKyNasypjeoieJsGsdjupx

Chart: jup.ag/tokens/4jnqfSM…

Discord: discord.gg/6Uc7F2PZzw

Dansk

Jack

1.1K posts

@DetailSZN

Building trading tools & systems @PoetTrading - 4jnqfSMWE1opwNT9m98s5QFKyNasypjeoieJsGsdjupx

JUST IN: 113,360 crypto traders liquidated in the past 24 hours.

Chat? It's not gonna reverse, right guys... Right guys? Jokes aside, I'll flatten up at 91, ahead of yesterday's opening Range. $SOL

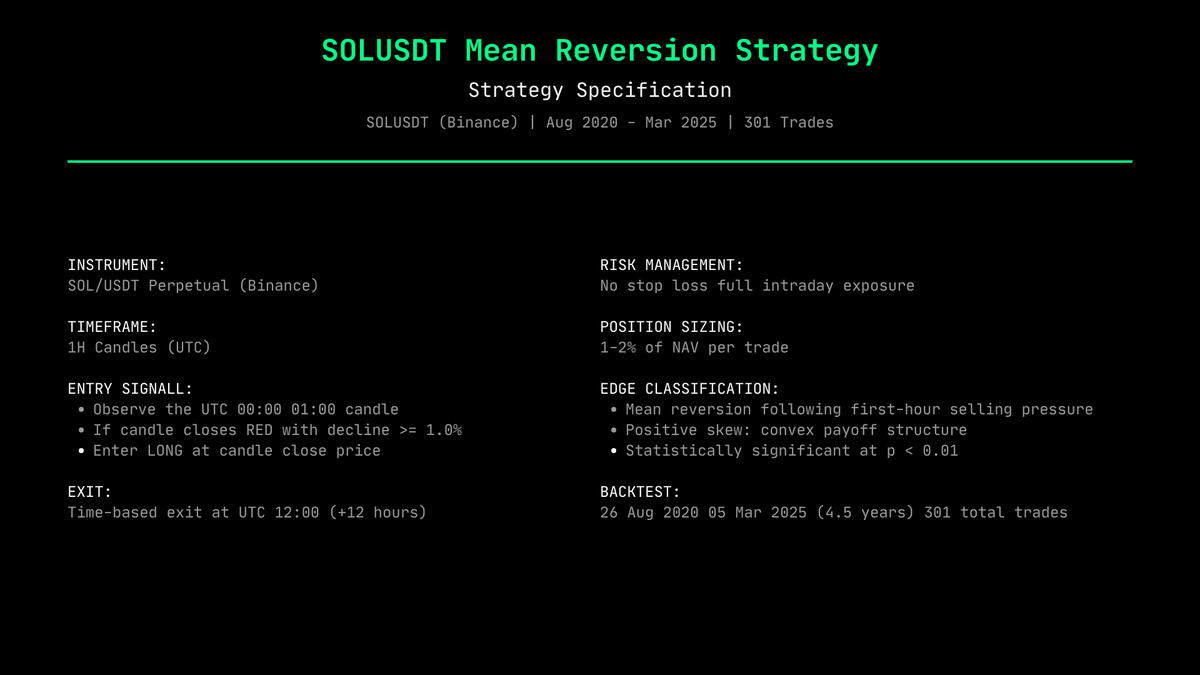

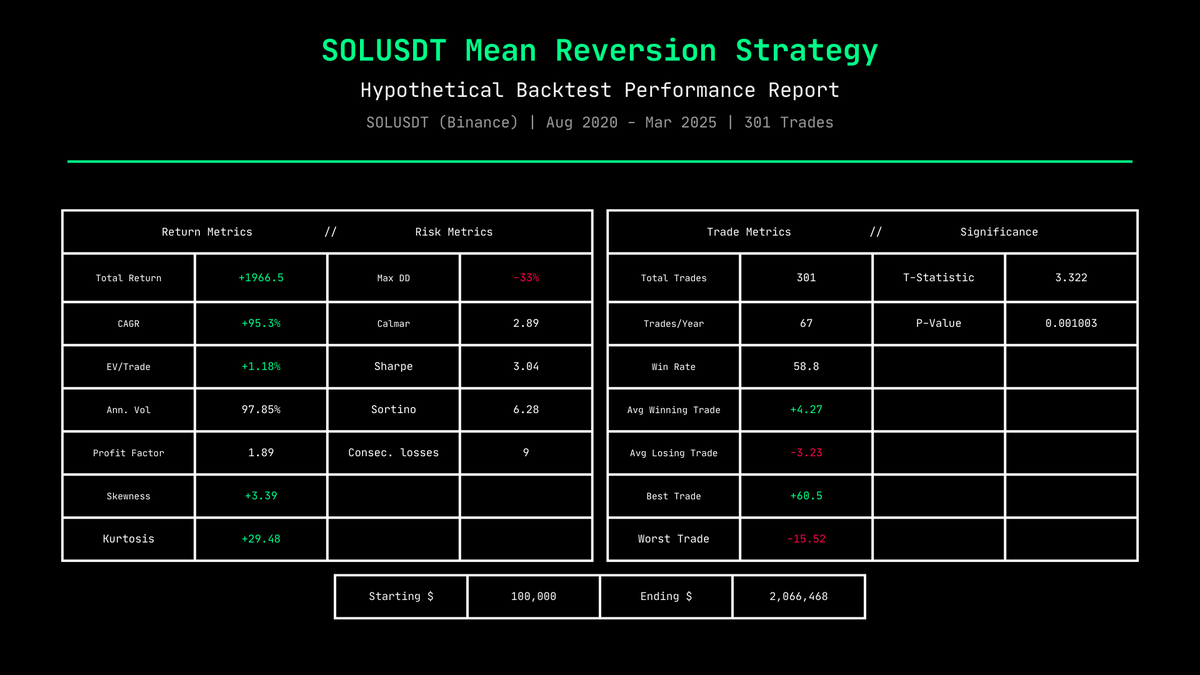

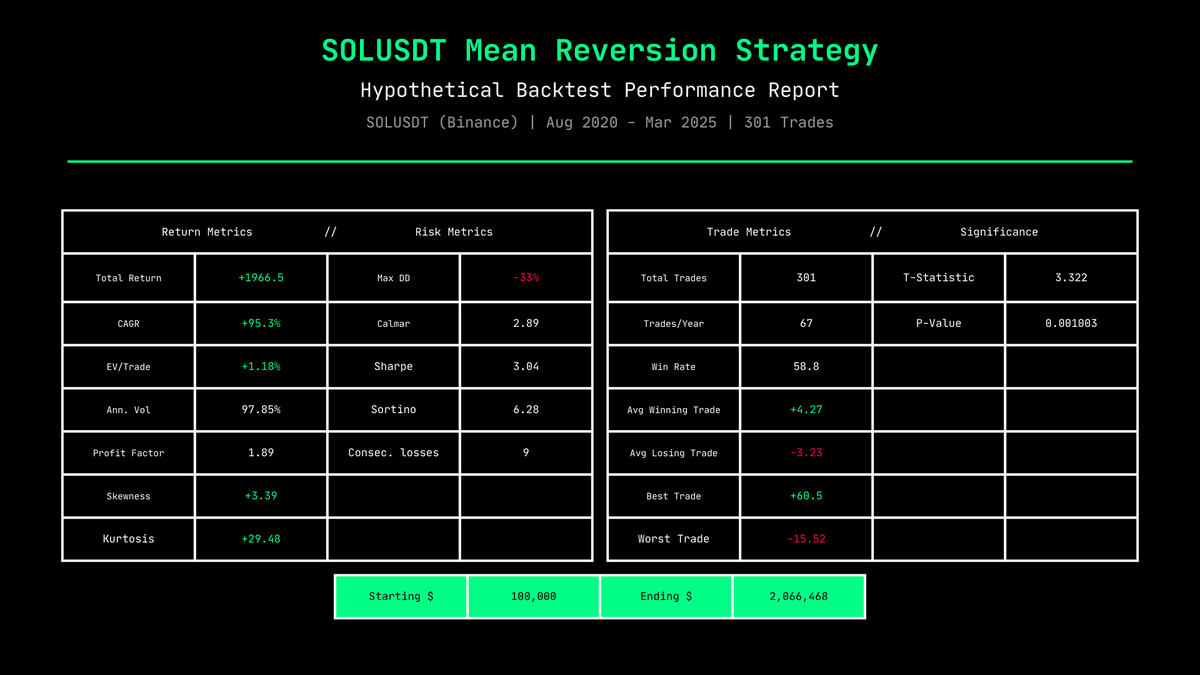

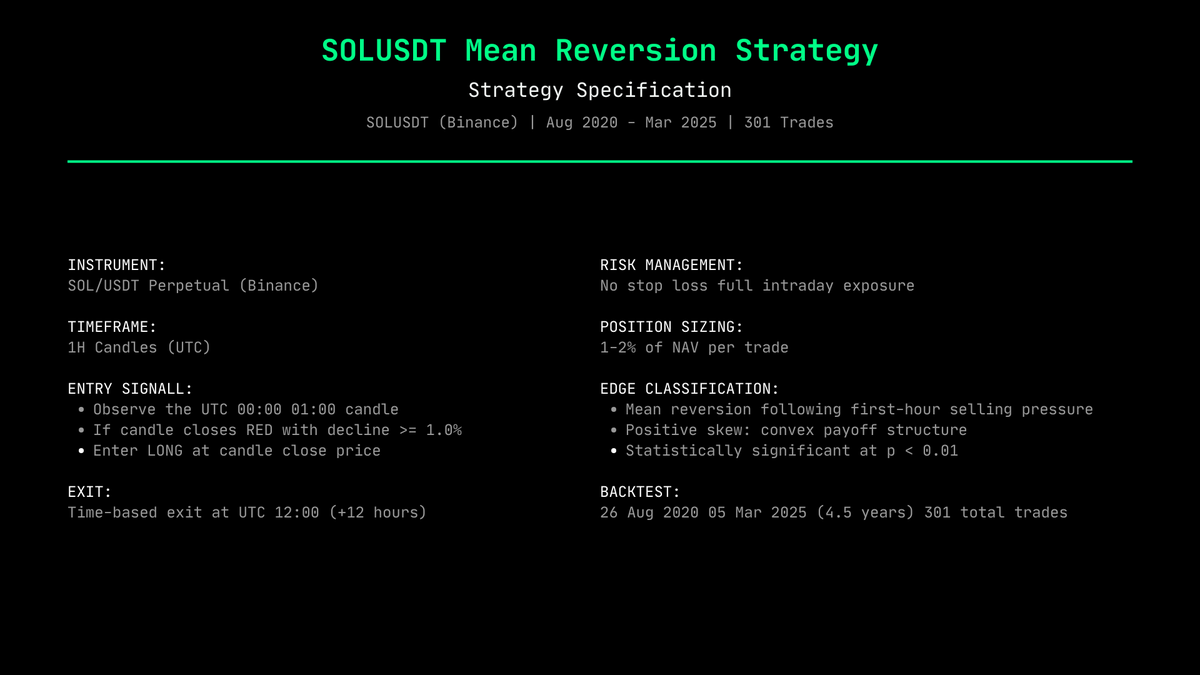

We found a mean reversion edge on SOL that's held for 4.5 years. The first hourly candle of the day closes red by >=1% → long → exit 12h later. One condition. No discretion. +1966% Total Return | Sharpe 3.04 | 301 trades | p < 0.01 Strategy + research paper LIVE now

New strategy live on Poet: $SOL Mean Reversion +1,966% total return 3 Sharpe 59% win rate 300 trades over 4.5 years p-val: 0.001 One rule. First hourly candle closes red by 1%+, go long, exit 12 hours later. Backtest, method, and research paper live. poet-drab.vercel.app

Possibly the most interesting part of looking at the first of hour of trading on $SOL is that the first hour does provide a small edge in discerning if the day closes higher/lower than the opening price. Green Hour = 56% chance of Green Day Red Hour = 57% chance... But... There is no edge (over the past 5 years) in the day closing higher/lower than the close of the first hour. Green Hour = 48% chance of closing above Green Hour Close Red Hour = 50% chance... What we do find though, is that there may be greater edge in a mean reversion trade based on the close of Red Hour. More to come... $SOL