HamatoYoshit

4.4K posts

$CELH is down nearly 70% from its peak.

That is exactly when I start paying attention.

A stock being down this much does not automatically make it cheap, but the business here looks a lot stronger than the chart suggests.

Celsius just reported Q1 revenue of $782.6M, up 138% year over year. Adjusted EPS came in at $0.41, well above estimates, and the company now controls roughly 20% of the U.S. energy drink market across Celsius, Alani Nu, and Rockstar.

The Alani Nu acquisition is a major reason this thesis looks more interesting to me.

Alani Nu did about $368M in Q1 sales alone, and it is now moving through the PepsiCo distribution system. That gives Celsius a much larger portfolio, better shelf presence, and multiple brands attacking different parts of the energy drink market.

The biggest risk is margin pressure and integration.

Gross margin fell to 48.3% from 52.3%, partly because Alani Nu and Rockstar currently carry lower margins. So this is not a perfect story. The company still has to prove it can integrate these brands, improve margins, and keep growth strong after the acquisition boost.

But that is also why the opportunity exists.

If Celsius can keep gaining share, expand internationally, improve margins back toward the low 50s over time, and execute with PepsiCo, this drawdown could look extreme in hindsight.

A broken chart does not always mean a broken company.

$CELH might be one of the more interesting “hated growth stocks” in the market right now.

English

הם הצליחו למחוק חשבון של 270,000 איש, אבל את האמת אי אפשר להשתיק! 🇮🇱

אחרי שנים של הסברה ישראלית בכל הכוח, החשבון הרשמי שלי נסגר. מבאס? מאוד. עוצר? בחיים לא.

חברים, אני בונה הכל מחדש ואני צריך אתכם איתי. בואו לעקוב עכשיו:

עברית

@jakebrowatzke @vishal_better Amazing answer I loved it. Thanks mate.

I feel the same about Hardware. Not my speciality but I did recognize the momentum and that everything's built on it, and can't argue with MU's growth and low p/e so I do have some exposure of ~15-20% of my portfolio to chips/memory.

English

I think that's a fair question.

The reason I have not made chips a focus of my personal investing portfolio or the "how to invest" portfolio, or something that I talk about often is because I don't have any expertise in hardware. It's that simple.

My two mentors, Peter Lynch and Warren Buffett, both said that you don't need to swing at every pitch and it's okay to miss opportunities. You can miss any number of opportunities and it doesn't hurt you. What matters is investing in the opportunities that you do understand fully, because hitting a few homeruns is all it takes to do extremely well in a single lifetime.

On a personal basis I couldn't tell you what separates an AMD chip from an NVIDIA chip, at least nothing on a very substantive level or with any sort of technical expertise, to be in a place where I really understand what makes one company's chips faster than another. Or what will make one company own the market of the future over another? Or what stops Google or Tesla from eating a substantial part of the market long term? Hardware is just not my specialty at all.

I think I can make enough money investing in software. At this exact moment yes it feels very bad because software is out of favor and hardware is in favor but that means this is actually the perfect moment to double down on software even more, not only because I understand it but because it's out of favor.

Now that does not mean that I don't think AMD or MU are good investments. But unless you're buying something that you have a ton of conviction in and understand thoroughly and really believe in over the next decade plus, you're not going to hold it long enough and it's just not worth buying. That's how it is for me. Knowing your own limitations can be one of your best strengths.

English

As $BETR's Q1 topline beat was pre-released, all focus will be on guidance in the Q1 report tomorrow - new partnerships, volume growth and the path to profit

Looking forward to hearing about all the great work being done at Better @vishal_better 💪

Good luck fellow shareholders

Jake Browatzke 🚀@jakebrowatzke

My most thorough thesis yet: Why I have invested $2 million to buy over 0.2% of Better.com (ticker $BETR )

English

@Doodushco אין מספר ברזל אבל אני תמיד משתדל להיות לפחות עם 15% מזומן

עברית

@mistershefer קניה ראשונה שלי היתה ב 23 דולר, חבל שלא קניתי יותר כבר אז

עברית

HamatoYoshit retweetledi

Lemonade’s Q1 results are 🔥. So much to share, where do I start?

First, get into the AI mood, click this, + volume ⏫

open.spotify.com/track/20HCH8XT… (by @kidfrancescoli)

🚀10th consecutive quarter of accelerating IFP growth

🔥 Topline at $1.33 Billion (IFP +32%)

🔥 Revenue grew 71% to $258M

🔥 Gross Profit increased 159% to $100M

🔥 3.14M Customers

🔥 Adj. Free Cash Flow $17M

Lemonade Pet exploding!

✅ Surpassed $500M top line early in Q2

✅ #1 most searched pet insurance brand in the U.S.

✅ @lemonade_inc is now the 4th largest pet carrier in the U.S.

✅ AI-powered automation drives record claim handling efficiency (LAE: ~4%)

✅ Our data + tech edge lets us lower prices while boosting profitability

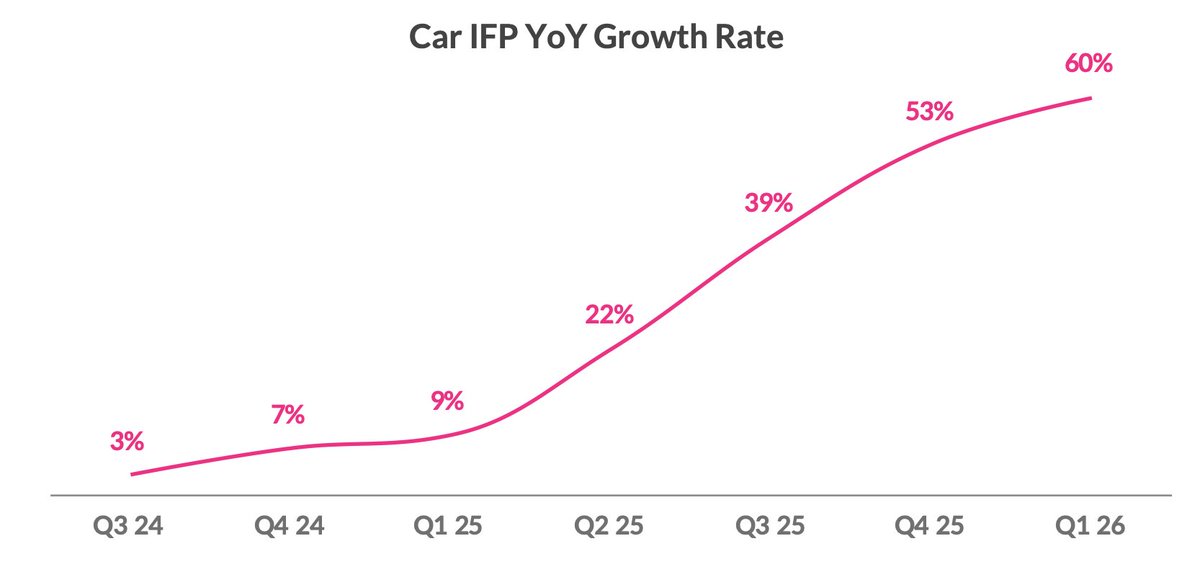

Car picking up speed

✅ Now at 60% YoY growth, $214M IFP

✅ Loss ratio improved to 74% (14 pts better YoY)

✅ Autonomous Car for @Tesla FSD conversion rate 70% higher than standard

And more...

↗️ Raising 2026 top & bottom line guidance

↗️ IFP per employee > $1M (3x improvement in 4 years)

↗️ Positive Adj. EBITDA in Q4

↗️ Investor Day in NYC November 17

English

🚨BAD news for ISRAEL

🚨Spain will tomorrow submit a formal request to the European Union to terminate the partnership agreement with Israel.

English

HOW I WILL PLAY THE NEXT MONTHS AND WHAT I EXPECT:

I want to touch on 5 important things:

1. First, I’m sad to see the lunch of $ASTS fail. I sold a while ago. “$Execution delays is a risks. Sold and took profit recently.”

Still saddens me to see.

2. I see a lot of new concerns on US/Iran. Here’s my take and how I will play it:

Overall I believe we have see the worst. I could be wrong. But usually when ceasefire and ‘talks’ have been somehow ongoing it’s very rare a full blown war will continue.

I expect some volatility short-term. I’ll be DCA’en through if it plays out.

Long-term I have NO concerns. US are on their way to a ‘goldilocks’ era. So many investments are being made INTO US.

I expect inflation to rise short-term. Fall afterwards towards the goldilock-era for US where AI infrastructure will play out and dominate.

Lastly. I see some concerns about ‘oh, but $SPY $SPX $QQQ are all back to ATH and topping.

Yes. But MAG7 is not topping. $NVDA $GOOG $AMZN are close to touching Octobers high. But recently. $MSFT $AAPL $TSLA are far from it.

Meaning the ‘top’ is not driven by small cap or MAG7.

But the middle-layer of $SPYx / SP500.

I’m not concerned. But expect more of a rotation to continue into risk-on - when US/Iran clears.

3. A couple of hours ago I released a FREE NEW extensive deep dive on $OUST. You should go read it.

4. I’m considering creating a FREE group-chat here on X. A community.

What I expect of the group:

This is not a buy/sell signal group.

But a group to connect with like-minded. Analyzing the market, sharing ideas, research, insights, learnings and Go deep on finding gems together.

There’s limited spots.

If you want to join. Comment: “YES.”

And just to be clear: I dont have a course or offer no paid services.

5. Based on 2) - I’ll sit tight in my long-term high conviction plays with ease and peace. Add on dips. Pure DCA.

Meanwhile I’ll soon open up my short-term account again and begin some short-term swing trades in the timeframe of less than < 6 months.

-BP.

Please note: this is not financial advice.

Black Panther Capital@BlackPantherCap

→ PORTFOLIO UPDATE & REFLECTIONS: Here’s what have changed: I used the recent volatility to take some profit and consolidate around my highest conviction names. LONG-TERM PORTFOLIO: $IREN – 24.2% $CIFR – 22.2% $TE – 16.2% $ONDS – 14.1% $RKLB – 14.1% $OSS – 9.1% SHORT-TERM PORTFOLIO: $IBRX – 100% What this tells you: I’m backing the truck up on AI infrastructure plays; $IREN, $TE, $ONDS, $OSS. These are convictions that’s only getting stronger. Why $IREN & $CIFR are now 46% of my portfolio: > The Microsoft deal didn’t change. > The hyperscaler arms race didn’t stop. > Power infrastructure remains the bottleneck everyone’s fighting over. $IREN controls 4.6GW now. $CIFR 3GW. Both are scaling and sitting on secured power, and deals. The drawdown? That was the market giving you a gift. Why I started a new position in $RKLB: Space infrastructure isn’t slowing down. It’s accelerating. I’ve been watching $RKLB for a while now. And the dip was a gift. Rocket Lab is the only pure-play orbital launch company trading at a reasonable valuation (in the growth sector) with PROVEN execution. It’s the ONLY competitor to @spacex, and market doesn’t like monopoly. Electron launches. Neutron coming. Defense contracts stacking. The setup is asymmetric. Why I added to my position in $TE: $TE owns and operates a 5GW solar With first phase 2.1GW online by end 2026. AI data centers accelerate power demand. Solar scales rapidly to address grid constraints. This isn’t complicated. Demand is structural. Supply is constrained. $TE owns the picks and shovels. Defense Exposure — $ONDS & $OSS at 23.2% Combined: NATO spending isn’t reversing. Defense autonomy isn’t optional anymore. These companies own bottleneck technologies in programs that compound for decades. $ONDS: Raised 2026 guidance by 25%. $65M backlog up 180% in 60 days. Trading below analyst target. $OSS: Brings high-performance AI to denied, contested, or austere environments where conventional setups cannot operate or introduce lethal latency. No debt. Watchlist now: $ASTS – Still on the watchlist. Conviction remains. But execution delays is a risks. Sold and took profit recently. $KRKNF – Monitoring closely. The Anduril thesis is intact but position sizing matters here. Sold recently. $NBIS – High conviction but fully allocated for now. Would add on meaningful dips. Sold recently. $ZETA – Back on the radar. Took profit earlier but watching for potential re-entry if the right setup allows. $RDW – Watching. $SATL – Watching. Early-stage conviction building. $PGY – Under review. Short-Term Play: $IBRX at 100% This is the asymmetric bet. Biotech with binary catalyst potential. High risk, high reward. I’m watching this daily and will adjust fast if thesis breaks. My approach right now: > Market volatility doesn’t change fundamentals. > AI infrastructure spending is going from $200B to $500B+. > Defense budgets are locked in for years. > Energy demand is structural. > The companies I own control bottlenecks in these trends. > Drawdowns are buying opportunities when conviction is high. I used this one to concentrate around my strongest theses. Bottom line, this portfolio is built around: → AI/energy infrastructure bottlenecks → Defense tech with sole-source positioning → Space infrastructure with proven execution → One asymmetric biotech swing Every position is sized by conviction. The drawdown strengthened my hand. My conviction didn’t drop. It increased. Adding on potential dips. Note: This is not financial advice.

English

My current portfolio:

$IREN - Currently over 50% of my portfolio.

$HIMS - Incredible week +48%. Peptides new AI.

$ONDS - Reduced greatly, but will revisit later.

$KRKNF - Recently added to long-term portfolio.

$OUST - This will be the next retail favourite.

$SATL - My current favourite space stock.

$IBRX - Anktiva approved across 33 countries.

$VELO - 3D printing, used by SpaceX. 'Nuff said.

$NUAI - Very high risk. A lot to prove.

NFA.

English

@jakebrowatzke My point is that technology changes so much faster nowadays so maybe 5-10 years outlook is becoming impossible to predict?

English

@Doodushco If anything it'll create even bigger opportunities and make having a Buffett/Lynch level understanding of fundamentals even more profitable.

English

My Investment Strategy: The Buffett-Lynch Hybrid

My strategy is simple, but it's not easy.

I own between one and five stocks at any given time. That's it. No options, no stop losses, no hedging. Just stock in businesses I understand deeply. I've averaged nearly 100% annualized returns since 2019 doing this, and I want to explain why it works and why most people would never be able to stomach it.

Where the Idea Comes From

My approach is a hybrid of two of the greatest fundamental investors who ever lived: Warren Buffett and Peter Lynch. Both were obsessed with understanding what a business is actually worth. But they expressed that obsession very differently.

Buffett has said that if you find three wonderful businesses in your life, you'll get very rich. His conviction is legendary, at one point, roughly 50% of Berkshire's stock portfolio sat in a single name, $AAPL. He prefers to buy no-brainers and never sell. His concentration is extreme because his conviction is extreme.

Peter Lynch ran Fidelity Magellan with over 1,400 stocks at times, which gave him a reputation for never meeting a stock he didn't like. That reputation is entirely unfair. Lynch was a master of understanding what every single company he owned was worth and actively rotating capital based on where the best opportunity was *right now*. If a stock ran up and the fundamentals hadn't improved to justify the new price, he'd sell it and move that capital into something where the fundamentals were strengthening but the price hadn't caught up yet. That discipline is what allowed him to outperform even Buffett during his time at Magellan.

I take what I believe is the best of both:

- **From Lynch:** The willingness to buy and sell based on present opportunity. The understanding that when a stock's price goes up without a corresponding improvement in fundamentals, your expected forward returns are shrinking and at some point, your capital is better deployed elsewhere.

- **From Buffett:** The heavy concentration on only your highest-conviction ideas. If something isn't a top-five idea, it doesn't deserve my capital.

How It Actually Works

Everything I do comes down to one question: *Which stocks in my universe have the highest estimated forward returns over the next five years?*

I'm constantly ranking opportunities. A stock earns its place in my portfolio by offering the best combination of strong or improving fundamentals and an attractive price. A stock loses its place when that equation changes - and it can change for several reasons:

- The stock price has gone up significantly without the fundamentals improving, compressing forward returns.

- The fundamentals have genuinely deteriorated, making the business worth less than I previously thought.

- Another stock with great fundamentals has dropped substantially, creating a better opportunity than what I currently hold.

- I discover a new opportunity - a company I wasn't previously tracking - that offers higher estimated forward returns than anything currently in my portfolio.

I'm never selling because a stock went down. A stock dropping 30% with improving fundamentals is a *better* opportunity than it was before, that's a reason to hold or add, not to panic. This is exactly why I don't use stop losses. Stop losses are a price-based exit rule, and my entire framework is fundamentals-based. They would force me to do the opposite of what my system calls for at exactly the wrong time.

I also don't sell because of macro headlines or market fear. I sell for one reason only: something else now offers a better forward return for my capital.

The Returns

This approach has allowed me to average nearly 100% annualized returns since 2019. I'm up roughly 300% over the last twelve months alone. Those numbers are real, but I need to be honest about what comes with them.

The Downside And I Mean a Real Downside

If you're going to own only a handful of stocks, you have to be willing to endure enormous drawdowns. There's no diversification cushion. When your top holdings go down, your entire portfolio goes down, and it can go down hard.

Amazon dropped over 90% during the dot-com bust and has suffered at least six separate drawdowns of 50% or more on its way to becoming one of the greatest investments in history. If you owned a concentrated position in $AMZN, you lived through those drawdowns in full. That's the price of concentration. You have to be able to sit through the pain without abandoning the strategy, because the moment you panic-sell a great business during a drawdown is the moment you turn a temporary loss into a permanent one.

I know this isn't theoretical, because I'm living it right now.

As of this writing, I am in an 80%+ drawdown year to date. That's not a typo. Eighty percent. And no that doesn't contradict being up 300% over the past 12 months. The reason is that I have used leverage margin as a core part of my strategy since 2019, and I want to be completely transparent about how it works and what it costs.

The Margin Strategy And Why I'm Rethinking It

Leverage amplifies everything. It amplifies your gains on the way up, which is how I generated a 300% return in twelve months, but this return was a 10x in a single year before the drawdown I'm in now. It also amplifies your losses on the way down, and worse, it introduces a risk that can make the core strategy unworkable: margin calls.

The basic principle of my strategy depends on being able to hold or buy when prices are falling and fundamentals are intact. Margin calls do the exact opposite as they force you to sell when you want to be buying. They take the decision out of your hands at the worst possible moment. So how do I reconcile using margin with a strategy that requires conviction through drawdowns?

Here's how it actually works: I allow the margin calls to happen at the beginning of a drawdown. I let the broker force-sell shares on the way down. Then, once the drawdown becomes severe, I deposit fresh capital into the account, capital I've kept on the sideline for exactly this moment. That fresh capital lets me repurchase all the shares I was forced to sell, ideally at much cheaper prices than where the margin calls hit. Not all immediately, but thanks to the new capital base, I ride the entire recovery back up using margin to buy an even larger share count than I started with, supported by the fresh capital added to the account in the drawdown.

This is not a strategy I recommend. It is genuinely degenerate. But the math has worked: I started with $20,000 in 2019 and grew my portfolio to $10 million in 2025. At that point, I withdrew $1 million in cash. I'm up over 300% over the last twelve months in portfolio value, that was only possible because of the withdrawals I took as the portfolio was running strong.

Now here's the pain. My portfolio went from $10 million down to $1.3 million where I sit today. One million of that $1.3 million is fresh capital I deployed during the drawdown. That means the market effectively destroyed $8.7 million in portfolio value. That is the real cost of combining concentration with leverage.

To make it worse, the stock I've now gone all-in on is a company I view as a potential 30X over five years, currently growing revenue 89% year over year, on the verge of EBITDA profitability within six months, with $130 million in cash and only $30 million of burn ahead before the profitability inflection, doesn't even allow margin. The market views it as too risky. So at this exact moment, I'm running the unleveraged version of the strategy for the first time in seven years. Not by philosophical choice, but by circumstance.

With multiple stocks I like down 50%-80% with strong fundamentals, it feels like the exact wrong time to not be leveraged heavily into my top 5. When I reduce or remove margin from my strategy, it should happen at a moment of strength when everything is going well, not in a drawdown where all my favorite stocks are down 50%+ and my portfolio is down 80%+.

What I'm Starting to Question

I'll be honest: this last drawdown has been the most painful I've ever experienced, and it's the first time I've seriously questioned the strategy.

The numbers still look good on paper. I've gone from $20,000 to $1.3 million in roughly seven years, even after an 80% drawdown. But I watched $10 million turn into $1.3 million. The psychological toll of that is real, and no amount of long-term compounding math makes it feel okay in the moment. Only having my real hope in Christ Jesus makes it easily barrable.

Here's what I'm reconsidering: my strategy has been designed from day one to maximize annualized returns. That has been the only objective function. Everything, the concentration, the leverage, the willingness to endure enormous drawdowns, flows from that single goal. And by that measure, it has worked.

But if the means of one of my eternal goals is to become a billionaire, then I think I need to weight longevity higher than I have been. A strategy that maximizes annual returns but periodically risks catastrophic drawdowns, the kind that can wipe out years of compounding completely, may not be the optimal path over a 20- or 30-year time horizon. The best annual return doesn't matter if you can't stay in the game long enough to compound it. Getting zeroed out once can turn a career of 100%+ annualized returns over decades into a complete failure.

This is the opposite of how I've thought about investing for the past seven years. I'm not sure yet what the right balance is between maximizing returns and ensuring survival. But I know that the unleveraged version of this strategy - owning one to five of your highest-conviction ideas, rotating toward the best opportunity, and never selling on fear - is the foundation that actually works. The leverage was an accelerant. It made the ride faster, but it also nearly ended it.

The unleveraged version of this strategy will still produce large drawdowns. Owning one to five stocks means you will, at some point, watch your portfolio drop 40%, 50%, maybe 60%. You need to be honest with yourself about whether you can handle that without making emotional decisions. Most people can't, and there's no shame in that. It just means this strategy isn't for them.

But if you can endure the drawdowns, if you can hold when every emotion is telling you to sell - the math of buying great businesses at attractive prices and rotating toward the best opportunity tends to work out over time. It has for Buffett. It did for Lynch. And it has for me, even with the scars I'm carrying right now.

PS: On Thursday, when the broader market was rallying hard on the peace talks, I fully deleveraged and sold out of the ridiculous 30+ stock portfolio I had built solely so I could stay maxed out on leverage while having most of my portfolio's liquid value in a margin-ineligible stock $BETR in my IBKR portfolio margin account. Borrowing into my 30th best idea is exactly the sort of idiocy I want to avoid in my investing career.

This weekend is my first weekend without any margin borrowed in what feels like six years. Beyond realizing I couldn't sleep well owning 30+ stocks — way too much to be thinking about and keeping up with — the other reason for selling was to make my portfolio transfer to a new brokerage easier.

I'm in a period of transition, trying to settle into the portfolio I feel has the highest upside and least downside coming out of the SaaSpocalypse, but I don't feel settled yet. I honestly don't know what I'll be doing on Monday. My #1 highest-conviction play, $BETR, being margin-ineligible is a new challenge for my strategy that I've never faced before.

I'm actively trying to find a broker that will lend against this stock, because I can't justify selling any of it — my model shows $BETR with a 3x+ higher 5-year return than my next highest-conviction names like $PATH, $LMND, and $HIMS. If my model is right, being 300% net invested across those three (100% in each) would produce roughly the same returns as simply going all-in on $BETR with no leverage at all.

However, my strategy really juices when I can continually buy more of a stock on margin as it rises (as long as it still shows the highest 5 year return). This creates a double compounding effect - the share price and the share count are both growing simultaneously, which makes the numbers go up unbelievably fast. Without that ability on $BETR, I could actually come out of this crash stronger being 300% invested in $LMND, $HIMS, and $PATH, since their rallies would unlock more margin buying power in a way that $BETR's rally can't. That said, I'm hopeful that once $BETR crosses a $1B market cap, margin eligibility prospects will improve. I also haven't lost faith in finding a brokerage or new account setup on IBKR that lets me margin into $BETR this week.

PPS: If you've read this far, you're clearly a reader so I highly recommend picking up Peter Lynch's One Up on Wall Street and Beating the Street for a far more experienced perspective than mine.

OahuRE.com@OahuRE_com

Sorry if you posted this before, but I am new to your posts and very interested. The $1.3 million, what percentage of your portfolio is that, and do you consider any type of stop loss, or do you hold long term unless your thesis changes about the company? You might have gone over your entire portfolio, stop-loss strategy, and other topics in other posts, but I am just reading your posts now.

English

@jakebrowatzke Can't BETR be easily disrupted by AI like most SAAS ?

English

I don't know what the future holds

But at this moment I believe the most likely outcome is that my $1.3M in $BETR becomes $39M within 5 years.

Why? Better Home & Finance isn't a mortgage lender. It's an AI operating system for the $15 trillion mortgage industry and almost nobody has figured that out yet.

Here's the core of the thesis:

The Tinman Platform. Tinman is an AI-driven automated rules-based decision engine that combines a point-of-sale system, CRM, pricing engine, document engine, loan origination software, and underwriting calculation engine into one platform. Better Traditional mortgage lenders stitch together eight legacy systems. Better replaced the entire stack with a single AI-native platform. Tinman is trained on over a decade of Better's internal mortgage data, having mapped roles, tasks, rules, and decisions across more than $110 billion in funded loans, 12 million recorded customer calls, and 5 billion pages of documentation.

The result? Loan officers using the Tinman AI app can fully underwrite loans in as little as 47 seconds, with a median time of about 2 minutes and 24 seconds — compared to an industry average of roughly 21 days.

But here's the inflection I'm betting on — Tinman is becoming a platform sold to others. Better is pivoting from being just a direct-to-consumer lender to licensing Tinman as infrastructure for the entire mortgage industry. @vishal_better described Tinman's commercial model as being sold "by the outcome" rather than by seats or licenses, with clients paying per transaction at funding. That's a SaaS-like business model layered on top of mortgage economics.

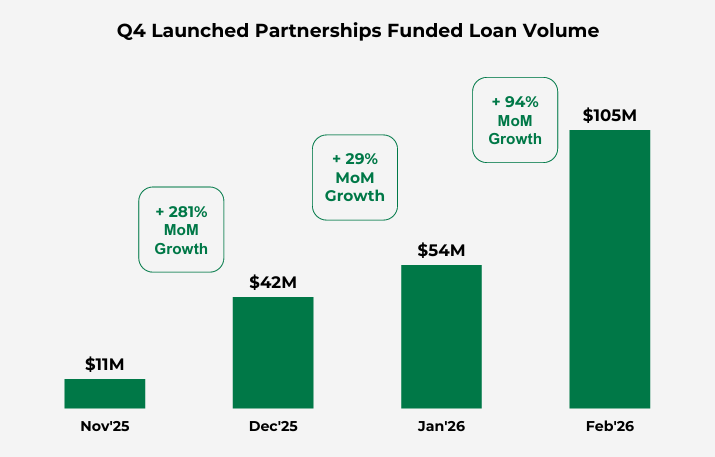

The partnerships are stacking up fast:

1. Credit Karma — this is the monster. Credit Karma has over 140 million members, and in just five months, the partnership has generated more than 30,000 mortgage pre-approvals while reaching less than 1% of its eligible member base. Pre-approvals scaled from 850 in October to 2,600 in November, 5,000 in December, 11,000 in January, and 13,000 in February 2026. That's an exponential ramp — and they've barely begun.

2. Finance of America — integrating HELOCs and home equity loans into its reverse mortgage platform through Tinman's plug-and-play capabilities.

3. ChatGPT/OpenAI integration — Better launched the first conversational credit decision engine for mortgages inside ChatGPT using a custom MCP connector, enabling lenders to underwrite loans through natural language. Within two weeks of launch, over 50 banks and mortgage brokers requested demos, including two of the three largest banks in the country.

4. A top-five non-bank mortgage originator went live starting with HELOCs, with a full enterprise rollout expected in Q2 2026.

5. A top-three personal lending fintech pilot was initiated and scaling rapidly.

6. Coinbase recently partnered with Better to offer Bitcoin backed mortgage loans via Better's Tinman. Better runs the entire mortgage stack and Coinbase custodies the coins.

The deals are generating real growth. Q1 2026 funded loan volume hit $1.64 billion, up 89% year-over-year, exceeding guidance of $1.40–$1.55 billion.

Tinman AI Platform funded loan volume reached $646 million in Q4 2025, comprising 44% of total volume. Better is targeting $1 billion in monthly loan volume by end of May 2026. That would mean another double from Q1 (already up 89% y/y) by Q3 2026.

The NEO distribution model proves Tinman works at scale. Within six months of rolling out, NEO increased loans funded per officer by 91%, per processor by 17%, and per underwriter by nearly 50%, all powered by Tinman AI.

The valuation gap is absurd. Figure Technologies trades at 11 times sales, Rocket Companies trades 3.14 time sales, while Better trades at just 2.4 times sales despite growing faster than Figure and MUCH faster than Rocket. $BETR's market cap today sits around $500–600 million.

Now the math for my $1.3M → $39M. That's roughly a 30x return. With ~18.5M shares outstanding and the stock around $35, I'd need the stock somewhere near $1,000+, implying a market cap of ~$18–20 billion.

For context, Rocket Mortgage sits around $41B and doesn't even have a 6% mortgage market share. If Tinman becomes one of the default operating system that banks, fintechs, and brokers plug into — charging per funded loan across a $15 trillion annual market — and if the HELOC business keeps compounding, and if Credit Karma alone converts even 5–10% of its eligible members... the revenue trajectory to support that valuation starts looking VERY plausible over a 5-year horizon.

There is risk. No doubt. The company is still loosing money and they recently had to dilute shareholders to raise capital, but now I believe they have all the runway they need to reach profitability.

Better is guiding to EBITDA breakeven by the end of Q3 2026. Total burn from here should not exceed $30M and they now have $130M of cash. Once profitable, the market will be forced to re-rate this from "money-losing mortgage lender" to "fast growing AI mortgage platform."

The CEO, CFO, CTO, and Chairman all recently purchased additional shares on the open market — insiders are buying. Insiders sell for many reason, but they only buy to make money.

Jake Browatzke 🚀@jakebrowatzke

BREAKING: 10% Insider Framework Ventures Loads Up On >0.3% of All $BETR Shares Friday 👀

English

SpaceX is heading for an IPO.

AI has had its moment in the spotlight, now space is about to steal it.

The next wave of winners is forming. Some will be short-term rockets. Some will be long-term compounders. Most will be noise. The hard part isn't getting excited about space, everyone's excited. The hard part is cutting through the hype to find the companies that actually have the right stuff.

That's what we do.

Our team sifts through the chaos, because who has time to read 1,000 reports? We do it for you so you can make an informed decision in as little as 5 minutes.

Our 193,000+ investors already get the clearest picture every week:

✅ All Meat, No Filler — We skip the noise and stick to the intelligence that actually matters.

✅ Early Alpha — We covered $RKLB in December before it peaked 60%+ in ~80 days. That's the kind of insight we put in your hands.

✅ Human Intelligence — Written by market veterans who've seen it all, not a bot hallucinating in a server farm.

Join our FREE newsletter today and lock in your membership forever. Every week we cover AI, Space, Tech, Crypto and Macro Analysis. I can't promise this stays free for long.

Comment "rocket" and I'll DM you the link. First 50 only.

English

היי חברים, מעדכן שהחשבון שלי בפייסבוק חזר.

אני רוצה לשתף אתכם בניסיונות ההשתקה הרבים שעברתי השבוע.

(1) עמית סגל, העיתונאי החזק בישראל, התרעם והשתלח בי על זה שהעזו לתת לי לכתוב 450 מילים בעלון שבת שחולק בבתי כנסת.

(2) עקיבא נוביק כתב נגדי וכמובן חסם אותי בכל הרשתות החברתיות.

(3) החשבון שלי בפייסבוק נוטרל לשעות ארוכות ללא כל הסבר מניח את הדעת.

(4) הכתב הדתי הפוליטי של ynet השתלח בי ואמר שאני לא ראוי בכלל לסיקור או התייחסות כי אני קיצוני מדי לטעמו או ״שונא דת״ לטענתו

(5) עיתונאי מקור ראשון שזה העיתון הגדול של הדתיים, יצא נגדי בגלל שהעזתי לדבר על חילוניות בעיתון דתי. יחד איתו עוד מאות דתיים בטוויטר התרעמו על זה שיש לי חופש ביטוי בכלל

(6) נפתח חשבון ווצאפ שהתחזה אליי, הפיץ פייק ניוז והפיל בפח עיתונאים, ואיתו שיתפו פעולה דובר של ח״כ סוכות מהקואליציה, שכבר התנצל מאז

(6) אלפי חשבונות טוויטר ופייסבוק תקפו אותי ודיווחו עליי כדי לסגור אותו. כל החשבונות שלי בכל הרשתות עוברים התקפות כאלה גם עכשיו.

וכל זה רק גורם לי להתחזק בחילוניות שלי ולחייך. אני מבין היטב שהאג׳נדה שאנחנו מובילים פה - ציונות חילונית בלתי מתנצלת, שעומדת בראש מורם ועם החזה מלפנים מול הפרימיטיביים שעמלים להפוך את ישראל למדינת הלכה חשוכה וענייה, האג׳נדה הזו מפחידה אותם. כי הם יודעים שרוב הישראלים יותר רוצים לחיות במדינה מערבית, חילונית ועשירה מאשר במדינת הלכה פרימיטיבית. אז הם מנסים להשתיק אותנו. ואני אומר אותנו - כי הם משתיקים גם אתכם כחילונים.

מה עושים מפה? משנים מציאות. אני אשים לכם כמה לינקים בתגובות. לינק אחד להתנדבות בצוות שלי שאת כולם אפגוש אצלי בבית אחרי החג. לינק נוסף לתמיכה בקמפיין הפוליטי שלי לפריימריז באתר שלי. ולינק שלישי לחיזוק קבוצת הווצאפ שלי לעדכונים ושיתופים אישיים.

שלא יהיה לכם ספק, בלי הגיבוי שלכם פה וברשתות חברתיות אחרות, אני לא בטוח שהחסימה היתה משתחררת כל כך מהר. יש הרבה כוחות פוליטיים שרוצים להשתיק אותנו. את הציונות החילונית שהפסיקה להתנצל.

עברית

@AdamBLiv Interesting! Could it go lower to 45k-50k in the next months like some believe and still be up a lot 12 months from now so it fits your script?

English

🔥BITCOIN JUST FLASHED A SIGNAL WITH A 100% HIT RATE ACROSS 15 YEARS OF DATA🔥

The power law z-score just dropped to −0.93σ.

I backtested every single time BTC reached this level of oversold.

Here's what happened next:

→ Median 12-month forward return: +631%

→ WORST-case 12-month return: +82%

→ Win rate: 100% (7 out of 7 episodes)

→ Best case: +2,500%

Read that again.

The absolute floor... the worst outcome in history from buying this level... was still almost a DOUBLE.

For context:

• Mar 2020 COVID crash hit this zone → +1,020% in 12 months

• Nov 2022 FTX collapse hit this zone → +151% in 12 months

• Sep 2023 hit this zone → +128% in 12 months

BTC at $66K is trading 47% below its power-law fair value of $125K.

The model (R² = 0.96) has held across 4 halving cycles, 3 bear markets, and every black swan you can name.

The math doesn't negotiate. It just compounds.

Not financial advice. Just a model and 5,700 days of data.

English

אחותו של השר עמיחי אליהו, הרבנית רחל בזק, עם כיסוי ראש, מסבירה ל-140,000 עוקבותיה שמצאה תרופה לסרטן.

אי אפשר להמציא את הפרימיטיביות האנטי מדעית הזו.

ואלה רוצים להטיף לציונות החילונית מוסר.

עברית

Drones are the future.

They can literally do anything.

Inspect pipelines, deliver critical supplies, monitor remote sites, operate where humans cannot.

Energy, defense, logistics.

Every sector is about to be disrupted.

My top drone pick is $ONDS.

Eric Trump@EricTrump

Drones are the wave of the future — Proud of this company and the work that they are doing to keep America safe. #JFB #XTEND

English