Belzebubz retweetledi

Belzebubz

1.4K posts

Belzebubz retweetledi

Here's the humanoid exposure crowdsourced list:

- $OUST

- Rainbow Robotics (277810)

- $AMBA

- Ubtech Robotics

- $MKA

- Nextronics

- $SYM

- Harmonic Drive (6324)

- $VPG

- Beijing Geekplus

- $MBLY

- $ARBE

- Nabtesco (6268)

- $SERV

- $HSYDF

- Robotstrategy

- $ZBRA

- $CATL

- $ABB

- $BOT

- Unitree (not public yet)

- $LSCC

- Esunny Robot (300024)

- $NOVT

- $RR

- $PDY

- Hesai (2525)

- $SHA.DE

- $XBOT

- $XPEV

- $BAM

- $ALNT

- 6268.T

- $AMBQ

- $ATOM

- $MRAM

- $ISRG

- $HLIT

- Robosense (2498)

- $HG

- $ACUVI

- $CGNX

- $KLIC

- $BSL

- $AEVA

- $AUR

- $CTH.V

- $IMSR

- $NEO

- $KDK

- $MRLN

- $KITT

- $INDI

- $NOVT

Off the top of my head:

Harmonic Drive, $OUST, $BOT, $VPG, $MBLY, and Ubtech showed up the most.

Will start doing DD into mentions.

Serenity@aleabitoreddit

All right chat. I need some more ideas on the early $RKLB equivalent for humanoid exposure. 10x+ potential returns only in the next 2 years and more pure play exposure than $TSLA. What’s your best ideas?

English

Belzebubz retweetledi

毎週開けられる!復活する金庫の場所まとめ🔒

ヘテロシティに存在する金庫は一部毎週復活します🔑

全て開けると15,000ファンスが獲得できるため、近くに立ち寄った際は開けておきましょう!

金庫の付近には不良NPCが配置されているため、邪魔されないように倒してから解錠するのがおすすめです⚔️

①絵空町西側の空き地

②絵空町北東の塀の裏

③ミゲル区西側の倉庫

④ミゲル区北側の倉庫

⑤ミゲル区東側の倉庫

⑥ミゲル区東側の工事現場(3Fと3Fと2Fの間の階層)

日本語

Belzebubz retweetledi

Belzebubz retweetledi

Hotori Pre Global Rating:

9/10 for Blossom/Nanally

7/10 if not playing Blossom.

Blossom Team with Nanally/JY/Zero/Hotori is definitive T0 team in NTE.

Gameplay:

- She's not really a support, but more of a sub DPS that deals a single nuke damage at the end of your original 3 man rotation.

- EG: Zero > JY > Nanally full EQ, swap to Hotori for her Ult to deal a single big nuke. Hotori always goes last.

- Essentially replaces Sakiri by having a much higher damage ceiling with Blossom (Vita Buds can still attack during Time Stop).

Cost Investment:

- Between Nanally and Hotori, I'd get E1 Nanally first; her ult energy charge is very comfortable for 1 rotation ults.

- Hotori Dupe > Weapon, espeically if you bought the Rain (MC) Arc. Dupe go for A1 or A6

Builds:

- 4PC Cosmos, Cosmos DMG%/Crit Rate Main.

- Double Crit > DMG% > ATK%

I'd be trying to go for E0S1 on my F2P account with E1 Nanally, most likely redeeming selector for Jiuyuan to complete Blossom Team.

#NevernesstoEverness

English

Belzebubz retweetledi

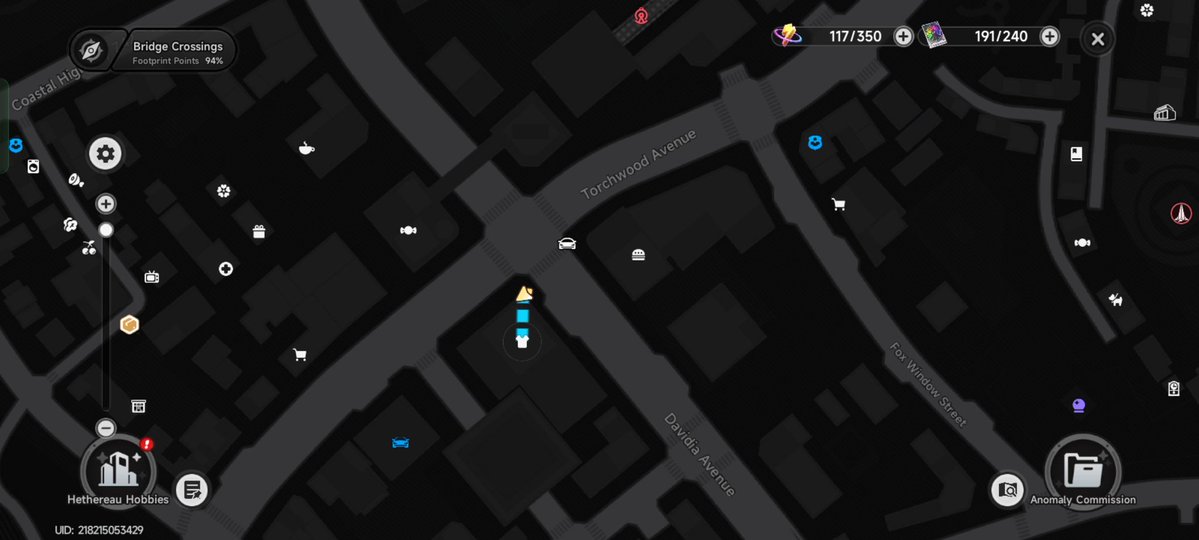

If you have Nanally, go to this location (try around 10am) & look for this NPC.

Once she meet Nanally, she will give her 50k Fons (& achievement)

#NevernessToEverness

English

Belzebubz retweetledi

เข้าคริปโตด้วยทุนแสนนึง ผ่านช่วง defi+nft+gamefi+มีมคอย กำไรไปถึงขั้น 7-8m+ ระเบิด+คัมแบ็ก ไม่รู้กี่รอบ สุดท้ายออกจากวงการคริปโตถาวร หลังช่วงมีมคอย ได้เงินมาก้อนนึง ใส่หุ้นอเมริกา นอนหลับสบายสุดๆครับ ถึงจะกำไรไม่เท่าตอนคริปโต แต่สบายใจสุดๆ

𝐲 / 𝐰 ❁@925_yiw

ทุกคนมีสิ่งที่พลิกชีวิตเป็นอะไรบ้างคะ? ของเราที่พลิกมากๆ เลยคือตอนที่ติดโควิดแล้วได้เงินประกันมาเกือบ 3 แสน จากมนุษย์เงินเดือนมีเงินติดบัญชีหมื่นต้นๆ เลยได้มีโอกาสมาเรียนที่ออสเตรเลีย ชีวิตก้าวกระโดดจากจุดเดิมพอสมควรเลย 🥹

ไทย

Belzebubz retweetledi

Belzebubz retweetledi

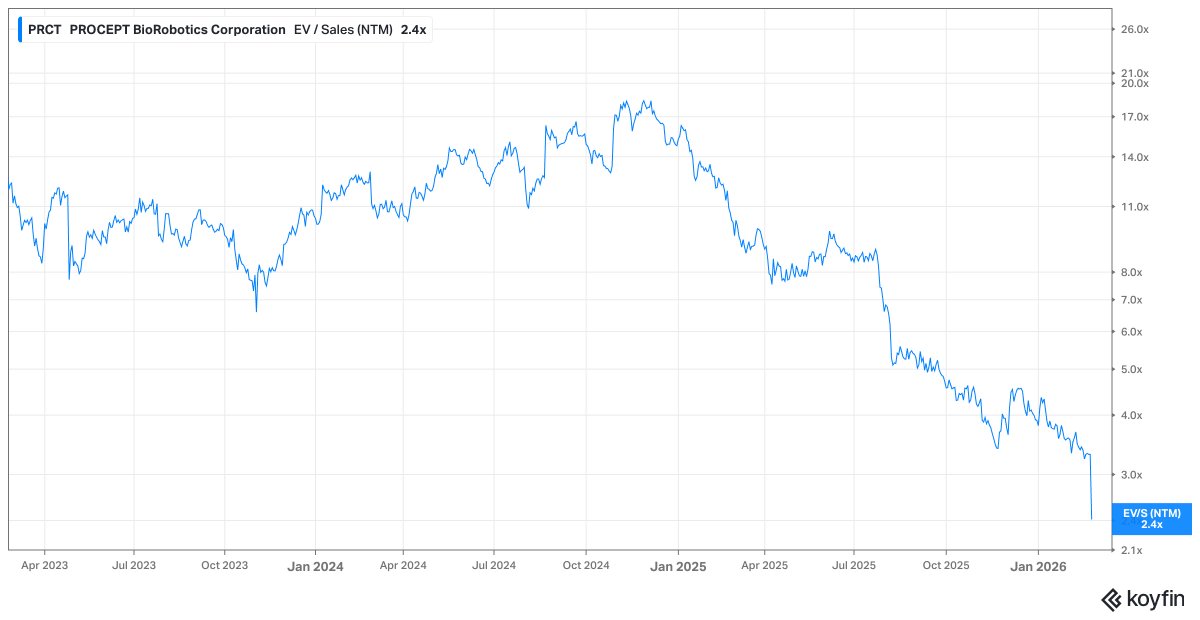

Lots of stocks this past month have gotten hammered on bad earnings reports (ie revenue miss and/or earnings miss and/or weak guidance).

One stock that deserved to be down (which I'll explain below) but now looks extremely attractive is $PRCT.

$PRCT is a medtech / robotics company that helps men with BPH (enlarged prostate).

There are 40 million men suffering/living with BPH... 6.7 million men are on drugs... 1.1 million men have tried drugs but discontinued (usually from the side effects)... 400,000 men (per year) are having surgical procedures to fix the BPH.

$PRCT is down -20% today because they missed on Q4 revenues but you need to understand why... the company said their customers were all starting to wait until end of quarter to put in their orders because they knew $PRCT would offer a bulk discount... so, they made the decision to stop doing bulk discounts in Q4. This caused an -18% miss on Q4 revenues versus expectations (not good).

Management said these quarter-end bulk discounts were creating bad habits, weaker margins and difficult inventory management so they needed to pull the plug... this definitely caught shareholders and analysts by surprise.

If you listen to the earnings call and the investor day presentation (from this morning), management said they needed to get rid of bulk discounts in order to raise ASP (average selling price) and remain on their previously announced path to profitability. Management said the elimination of bulk discounts will raise ASP by 9% in 2026 vs 2025.

$PRCT has provided CY2026 revenue guidance of 27-33% which implies $390M to $410M revenues. $PRCT said ebitda will be somewhere between -$17M and -$30M however they feel very confident they'll be ebitda+ by 2026 Q4 and ebitda+ for all of 2027.

If you look at the chart below, just 16 months ago (Nov 2024)... $PRCT was trading at 18.4x NTM revs (way too expensive)... today, $PRCT is trading at 2.5x NTM revs and that doesn't include the $285M of cash on the balance sheet so it's more like 2x NTM EV/revs.

$PRCT did say they believe procedures will be at least 37% YoY in CY2026 however it's hard to know exactly how much inventory their customers are sitting on but those customers can't run inventory down to zero... but this makes me think there's some upside to their 27-33% revenue guidance.

Something else I want to discuss is medtech margins once they hit the breakeven inflection point because this is where it gets really interesting... and one reason why I try to be in these stocks before that inflection point.

Medtech has significant upfront costs when developing, launching and selling their products but once they get their systems installed in hospitals and/or surgical centers every $1 of incremental revenue sold through those centers comes with significant profit margin. $PRCT already said gross margins will increase from 63% in 2025 to 65% in 2026 with a path to 70% or higher in the next few years.

$PRCT ended 2025 with 718 installed systems, up 42% YoY which means many of these systems have barely been monetized... they expect to add another 200+ systems in 2026.

Over the past 5 years I've done well with medtech... my two biggest winners were $TMDX and $SWAV (acquired by $JNJ at 13x revs).

If you look at their financials over the past 5-6 years you will see horrible ebitda margins up until the inflection point and then those margins go parabolic.

Starting with $SWAV, going back to 2019 and 2020, they had an average of -94% ebitda margins... however by 2022 and 2023 those ebitda margins had improved to an average of +34%

Moving onto $TMDX, going back to 2019-2022, they had an average of -92.8% ebitda margins and by 2024 those ebitda margins had improved to +20%

So, if $PRCT is telling us they'll be ebitda+ by end of 2026 and ebitda+ all of 2027 then it means the inflection point is not far away and it's possible we see ebitda margins in the 20-30% range within the next 2-4 years.

I believe $PRCT can compound revenues at 24% through 2030 while expanding ebitda margins to 20-30% in the same timeframe.

$ISRG is a very mature medtech / robotics company with 43% ebitda margins. $SWAV was at 32% ebitda margins when they got acquired. It's not unreasonable to think that $PRCT can get ebitda margins to 25% or better over the next 4 years.

If (and it's still a big if)... $PRCT can compound revs at 24% through 2030 and get ebitda margins to 25% (midpoint), then the stock price has significant upside from current prices... perhaps a 3-bagger or better.

I'll stop there since it's already alot of information to think through... fwiw... they also have new products coming out (to help with prostate cancer) and they've realigned their sales & launch teams to better monetize newly installed systems.

NFA. DYOR.

**We do have a small position in $PRCT at @FirstWaveFund and increased that position today on the selloff.

Here is the link to the investor day presentation from earlier today... ir.procept-biorobotics.com/static-files/5…

English

Belzebubz retweetledi

จากใจคอกาแฟวันละ 2 แก้วเสี่ยงฟันเหลืองคราบพลัคขั้นสุด แต่ฟันยังขาวอยู่ได้จนหมอฟันกับผู้ช่วยทักไปทำอะไรมา จริง ๆ ไม่ยากแค่

- หาหมอฟันทุกปี ขูดหินปูนทุก 6 เดือน เช็คสภาพช่องปากทั้งหมด ฟอกสีฟันกับหมอเห็นผลที่สุดไม่รับความเห็นต่าง

- กลับมาเมนเทนต่อด้วยการใช้ยาสีฟันสีม่วง เน้นสูตรไม่แสบปาก ไม่ทำร้ายเคลือบฟัน (เราใช้แบรนด์ไทยตัวดังอยู่ตัวเดียว)

- แปรงสลับกับยาสีฟันมีฟลูออไรด์สูง 1,000 - 1,500 ppm

- แปรงแห้ง หรือ บ้วนน้ำน้อย ให้ฟลูออไรด์ได้ทำงานนานขึ้น

- เริ่มแปรงลิ้นด้วยแล้ว ช่วยลดคราบสะสมที่อาจส่งผลมาถึงฟัน และกลิ่นปาก

- ใช้แปรงสีฟันสูตรเพื่อฟันขาว ถ้ามีงบไปใช้แปรงไฟฟ้า

- น้ำยาบ้วนปากช่วยเยอะนะ เราใช้สีม่วงตัวดังสูตร 6-in-1 Benefits ไร้แอลกอฮอล์ไม่แสบปาก

- ใช้ไหมขัดฟันเคลียร์เศษอาหารออกจากซอกฟัน ที่แปรงสีฟัน/ไม้จิ้มฟันเข้าไม่ถึง

- ดื่มชากาแฟจากหลอดเสมอ (หลอดร้อนก็มี) ฟันเหลืองช้าจริง เราไม่ต้องงดชากาแฟเลย ฟินมาก

- ดื่มน้ำเยอะ ๆ หรือบ้วนน้ำบ้างระหว่างวัน ช่วยชะล้างเม็ดสีและกรดที่อาจทำลายเคลือบฟันได้

- โชคดีที่เราไม่สูบบุหรี่ไม่ดื่มแอลกอฮอล์ หมอบอกว่ายิ่งคนดื่มไวน์แดง ยิ่งจะฟันเหลือง

mb@malieblue

คือเราประสบปัญหาฟันเหลืองไม่ค่อยมั่นใจ ช่วยแนะนำเราหน่อยได้ไหมคะ ยาสีฟัน หรือผงขัดฟันอะไรก็ได้ค่ะ (( ส่วนตัวแปรงฟันถูกทุกอย่าง ชากาแฟไม่ทาน แต่อาจจะเป็นเพราะพริกแกงของคุณแม่ )) ช่วยแนะนำหน่อยนะคะ 🙏🏻

ไทย

Belzebubz retweetledi

\㊗️ポケモン30周年🎊/

これまでに発見されたポケモンたちの30周年ロゴを、全国5都市の屋外広告で公開中!

下の画像をタップして投稿すると、

全1025匹分の30周年ロゴアイコンの中からランダムで1つがリプライで届く📲

キミも、ポケモン会えるかな?

⚠️注意事項はツリーへ!

日本語

@louis_meka จริงครับ เหรียญก็เยอะไปหมด liquidity แห้ง เทรนโลกเป็น AI อีกไม่คิดกลับไปคริปโตอีกเลย ยกเว้นจะมีไรกาวๆให้ผมกลับไปเล่นละนะ 55

ไทย

อดทนอยู่แบบติดลบกับคริปโตมานาน 5 ปี พอ Q4 ปีที่แล้วได้จังหวะถอนทุนคืนพร้อมกำไรจากเหรียญ ASTER ผมก็ตัดสินใจออกจากวงการคริปโตแล้วมาเล่นหุ้นแทน โดยใช้ Gemini จัดพอร์ตการลงทุนสำหรับเน้นสายกินปันผลและมีสายเติบโตมาเสริมเล็กน้อย

----------------------------------

📊 เจาะลึกแหล่งที่มาของเงินปันผล (Income Breakdown)

ผมแบ่งสินทรัพย์ออกเป็น 3 กลุ่มตามหน้าที่ในการผลิตเงินสดครับ:

1. กลุ่ม "เครื่องจักรผลิตเงินสด" (High Yield: >7%)

กลุ่มนี้คือหัวใจหลักที่ทำให้พอร์ตคุณมีกระแสเงินสดสูง

- JEPQ (~9-11%): จ่ายหนักที่สุดในพอร์ต มาจากการทำ Covered Call บนหุ้นเทคฯ

- JEPI (~7-9%): รองลงมา จ่ายสม่ำเสมอทุกเดือน

- DIF (~8-9%): กองทุนโครงสร้างพื้นฐานไทย จ่ายนิ่งและสูง

- TFFIF (~7-8%): คล้าย DIF จ่ายสม่ำเสมอ

2. กลุ่ม "เติบโตพร้อมปันผล" (Moderate Yield: 3-6%)

กลุ่มนี้ช่วยให้ปันผลของคุณชนะเงินเฟ้อในระยะยาว

- O (Realty Income) (~5-6%): จ่ายทุกเดือน และขึ้นปันผลบ่อย

- DIVO (~4-5%): เน้นหุ้นคุณภาพ จ่ายปันผลดีและสม่ำเสมอ

- SCHD (~3-4%): ปันผลอาจจะไม่สูงเท่ากลุ่มแรก แต่มีการเติบโตของเงินปันผล (Dividend Growth) สูงที่สุด

- VAYU1 (~3%): ผลตอบแทนขั้นต่ำ (Min Guarantee) ที่ค่อนข้างแน่นอน

3. กลุ่ม "เน้นเติบโต" (Low/No Yield: <1.5%)

- KKP US500-UH และ KKP NDQ100-UH: สองตัวนี้เน้น Capital Gain (กำไรจากส่วนต่างราคา) ปันผลมักจะน้อยมากหรือไม่มี (Accumulating) จึงไม่ได้นำมาคำนวณเป็นกระแสเงินสดหลัก

- SCBKEQTG: ปันผลจากหุ้นเกาหลีมักจะไม่สูงมาก เน้นรอบการเติบโตมากกว่า

----------------------------------

💰 ปฏิทินการรับเงิน (Cash Flow Schedule)

ความสวยงามของพอร์ตนี้คือ "มีเงินเข้าแทบทุกเดือน" ครับ

รายเดือน (Monthly Payers): JEPI, JEPQ, DIVO, O

- คุณจะมีเงินสดเข้าบัญชีทุกเดือนจาก 4 ตัวนี้ รวมๆ ประมาณ xx,000 - xx,000 บาท/เดือน แน่นอน

รายไตรมาส (Quarterly Payers): DIF, TFFIF, SCHD

- ช่วงเดือน มี.ค., พ.ค., ส.ค., พ.ย. (โดยประมาณ) จะมีเงินก้อนใหญ่เข้ามาทบจากกลุ่มนี้ ทำให้รายรับในเดือนเหล่านี้กระโดดขึ้นไปสูงกว่าปกติ

รายครึ่งปี/ปี (Semi-Annual): VAYU1

- มักจะจ่ายปีละ 2 ครั้ง เป็นโบนัสก้อนใหญ่

----------------------------------

👍 จุดที่ "ดีเยี่ยม" สำหรับระยะยาว (The Good)

1. พลังของ Dividend Growth (ปันผลที่โตตามเงินเฟ้อ)

ในระยะ 5-10 ปี ศัตรูตัวฉกาจของนักลงทุนกินปันผลคือ "เงินเฟ้อ" ครับ

Hero ของพอร์ตนี้: SCHD, DIVO, O

เหตุผล: กองทุนเหล่านี้ไม่ได้จ่ายปันผลเยอะที่สุดในวันนี้ (Yield 3-5%) แต่พวกเขามีประวัติการ "ขึ้นเงินปันผล" ต่อเนื่อง แทบทุกปี ในอีก 5 ปีข้างหน้า Yield on Cost (ปันผลเทียบกับเงินต้นที่คุณลงวันนี้) ของตัวเหล่านี้จะสูงขึ้นเรื่อยๆ ชนะเงินเฟ้อได้สบายครับ

2. กระแสเงินสดสม่ำเสมอทุกสภาวะตลาด

Hero ของพอร์ตนี้: JEPI, JEPQ, DIF, VAYU1

เหตุผล: ไม่ว่าตลาดหุ้นจะเป็นขาขึ้นหรือขาลง กองทุนเหล่านี้ถูกออกแบบมาให้ผลิตเงินสด (Cash Flow) ออกมาตลอดเวลา โดยเฉพาะ JEPI/JEPQ ที่ใช้ Options มาช่วย และ DIF ที่เก็บค่าเช่าโครงสร้างพื้นฐาน ทำให้คุณมีเงินสดหมุนเวียนเข้าบัญชีตลอด ไม่ขาดมือ

3. การกระจายความเสี่ยงระดับโลก

คุณไม่ได้ฝากชีวิตไว้กับเศรษฐกิจไทยอย่างเดียว แต่มีทั้งค่าเช่าที่ดินในอเมริกา (O), บริษัทเทคฯ ระดับโลก (JEPQ), และโครงสร้างพื้นฐานไทย (DIF/TFFIF) ซึ่งเป็นการกระจายความเสี่ยงที่สมดุลมาก

ไทย

Belzebubz retweetledi

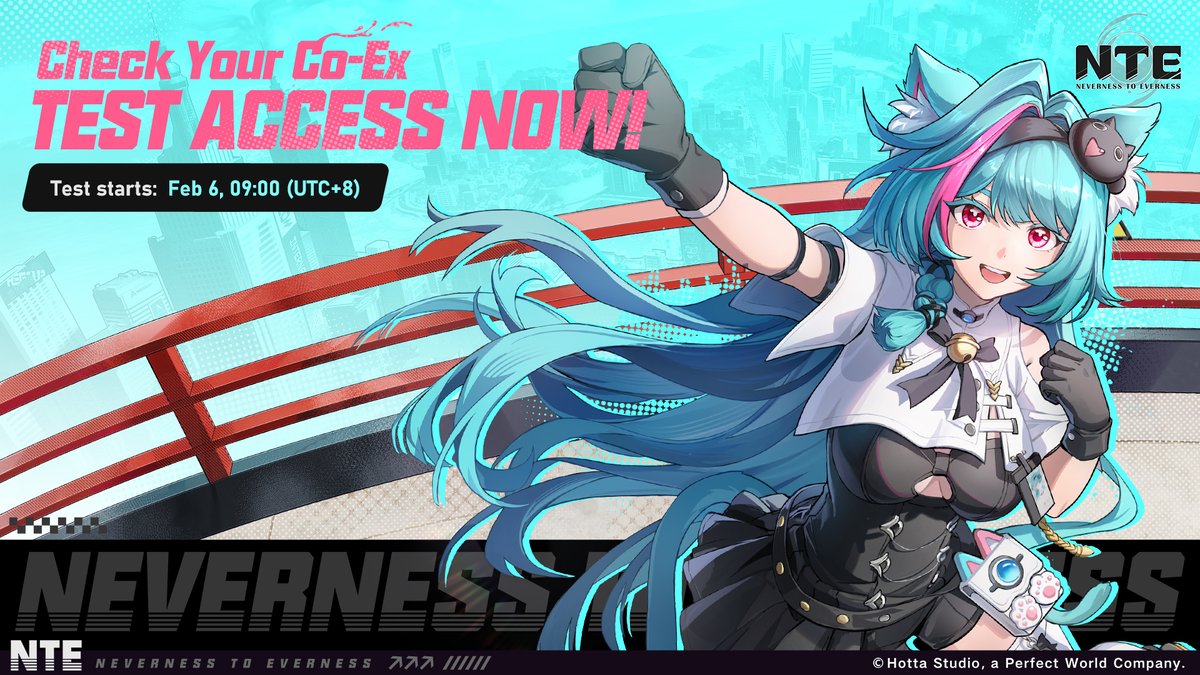

NTE Co-Ex Test Eligibility Checker Now Available

Appraisers, the NTE Co-Ex Test Eligibility Checker page is now live. Visit the page to see if you're able to take part in the Co-Ex Test.

Check your status here: pwgam.es/469h1Qa

>>>How to Check<<<

Visit the page and log in using the PWG account you created during pre-registration. Click the [Query] button to see your result.

※Important Notes:

1. Test access confirmation and game installation guides will be sent via email on February 4th at 09:00 (UTC+8) when pre-download starts. Check the email address you provided during pre-registration.

2. Official Co-Ex Test notification emails will be sent from addresses ending in [@email.perfectworld.com] or [@mail.perfectworldgames.com]. These emails may land in your Spam or Promotions folder, so please check there and mark them as trusted to ensure you don't miss important game updates.

3. Selling, trading, or transferring test accounts & game clients is strictly prohibited. Any account flagged for suspicious activity or transfer will have its test access permanently revoked.

4. Please safeguard your personal information. Ignore any third parties claiming they can sell or trade test access. These are scams.

>>>About the Co-Ex Test<<<

▶ Pre-Download Starts: February 4th, 09:00 (UTC+8)

▶ Test Starts: February 6th, 09:00 (UTC+8)

▶ Test Ends: February 20th, 23:59 (UTC+8)

▶ Test Type: Limited-Access Closed Beta (No Purchases, Progress Wiped)

▶ Platforms: PC (Windows) / iOS / Android / PlayStation®5 / PlayStation®5 Pro

▶ Game Languages: English, Japanese, Korean, German, French, Spanish, Russian, Simplified Chinese, Traditional Chinese

▶ Voice Languages: English, Japanese, Korean, Chinese

NTE pre-registration is now open. Welcome to Hethereau!

Preregister for NTE now >> pwgam.es/4scX8kS

#NTE #NevernesstoEverness #NTEbeta

English

Belzebubz retweetledi

My new position is $WIX.

This might be controversial, but I think it’s one of the most asymmetric opportunities in the market right now.

When you buy $WIX, you’re effectively buying two businesses: Wix and Base44, and that changes the story.

Here’s a summary of the thesis: 👇🏻

For less than $5B, you’re buying...

1) The core Wix business

It generates >$600M in annual FCF with ~30% margins, and there’s still room for additional operating leverage.

Many investors believe Vibe Coding will disrupt Wix. I think that view misses a key point: Wix is deeply embedded across millions of SMBs, and most of these are happy to pay a few hundred extra dollars per year to avoid the friction of switching platforms.

More importantly, Wix isn’t ignoring the shift. The company has already started integrating AI and Vibe Coding into its platform with the launch of Wix Harmony. Management’s confidence seems high, they’re even returning to the Super Bowl for the first time in six years to promote this new product.

2) Base44

Base44 is one of the fastest-growing Vibe Coding platforms in the market (according to Similarweb's data).

$WIX acquired Base44 in June 2025 for $80M. In less than six months, ARR grew from ~$3M to >$50M. I wouldn’t be surprised to see it exit 2026 at ~$200M in ARR.

For context, here’s how its peers are valued in the private markets:

- Lovable recently raised at a $6.6B valuation (~30x ARR), up from $1.8B in July 2025

- Replit is reportedly in talks to raise at $9B (>30x ARR), up from $3B in September 2025

Even applying a lower ARR multiple, Base44 alone could be worth close to $WIX's current market cap by the end of this year.

That’s where the mispricing is, and that’s why I’m accumulating shares.

It’s not about Wix or Base44 being clear leaders in their segments, it’s about the market misunderstanding the assets tied to the stock.

The downside seems limited, and $WIX is taking advantage of the current SaaS selloff to accelerate buybacks.

I’ve removed the paywall from my Deep Dive, published about two weeks ago. You can read it here:

🔗 mvcinvesting.substack.com/p/my-next-big-…

NFA.

English

Belzebubz retweetledi

Belzebubz retweetledi

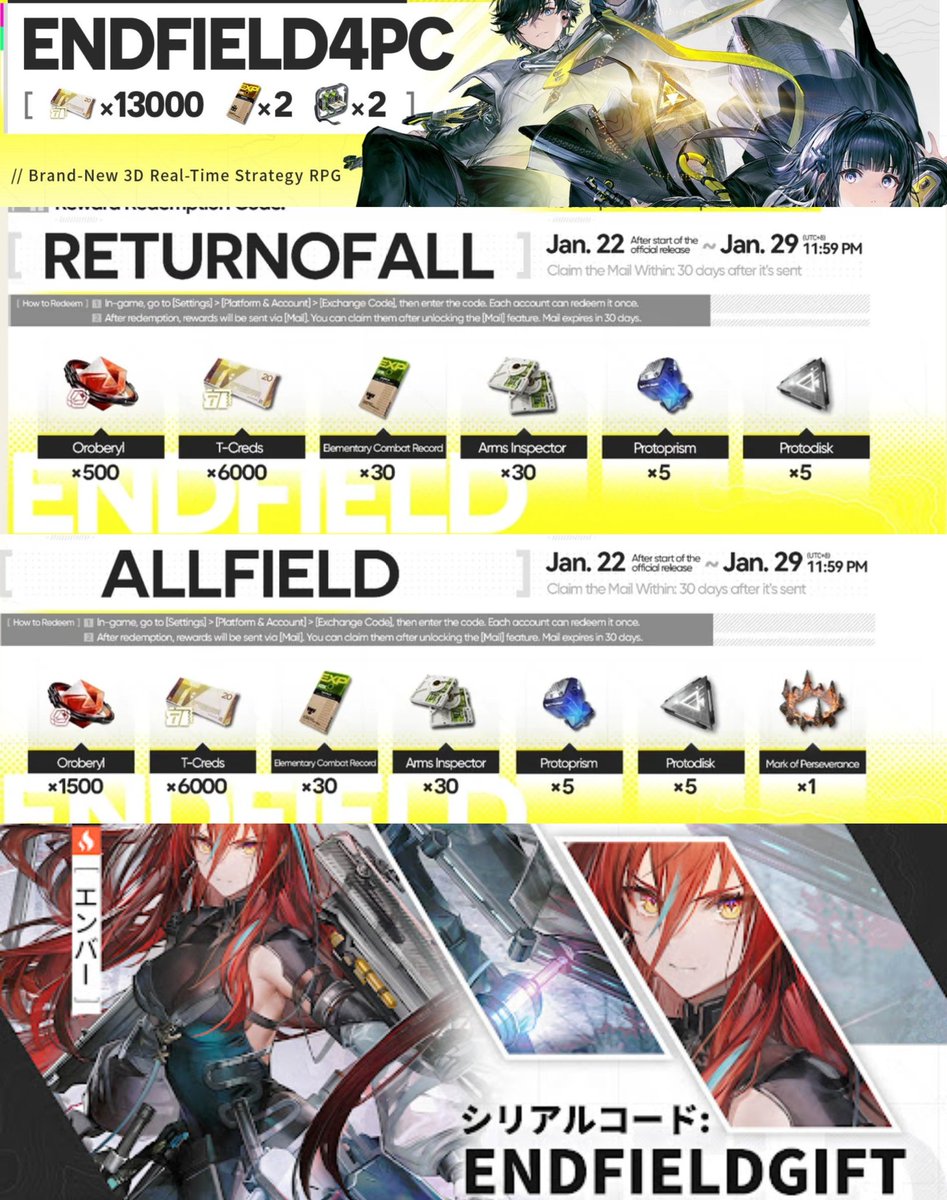

All Arknights Endfield codes

RETURNOFALL

ALLFIELD

ENDFIELDGIFT

ENDFIELD4PC

#ArknightsEndfield #エンドフィールド

English