@aleabitoreddit $IQE will likely do the same.

English

Eccentric Shiba Inu Invest

2.9K posts

I’m long $SIVE at $140M. I believe this is the next $LITE that markets and institutions missed. $SIVE makes InP CW DFB lasers. Closest comparison is $LITE in the current EML laser bottleneck. But instead of supplying to Innolight/Eoptolink for current optical transceivers cycles. They supply the lasers to $POET Starlight, Ayar SuperNova. And others for the future CPO/silicon photonics architectures spearheaded by $NVDA. Current valuations make 0 sense to me personally. $POET is advanced packaging for $SIVE type lasers… But $POET commands worth 11x+ more than the company making the laser itself? It’s feels like valuing a more advanced $FN (~$20B) packaging at $400B when $LITE is valued at $40B. So now at $130m: - - You have a likely mini $LITE like laser supplier to Marvell Celestial + hyperscalers through $POET. - Laser supplier to Ayar ( $NVDA, $INTC ), though they do multi source with $LITE, Sumitomo, $MTSI. And other potential up and coming suppliers potentially like Lightmatter that they’ve name dropped (eg. Q2 2023 earnings). This is unconfirmed but supply chain BOM is confidential. On top, for revenue, they expected $453M "pipeline next few years”. And, they have capacity expansion through WIN: “Win Semi foundry qualification in progress for volume production from Laser designs from Sivers." Sivers feels the silicon photonics/CPO version of $LITE, with actual rapidly growing customers like Celestial through $POET, Ayar, with more to come. I wouldn’t have liked it last year, but just 3 weeks ago, they refinanced all their debt successfully to $12M convertible loan (10.85%) and a $5M term loan (12%), which cleans up debt. It’s $17m total, which feels like nothing to US markets when $AAOI is doing a $500m ATMs every other week. Best of all, this is their pure play inp laser segment for silicon/photonics + cpo. Their Lidar segment is ramping up and they have $53-138M projected revenue coming in. Downside risk: - execution (as always) - dilution to scale up capacity to compete with $LITE and others. - $LITE, $COHR competition on scale after $NVDA just gave them $4B - CPO ramp gets delayed. I have no clue how, $LWLG, a pre-revenue science project with $TSEM, is valued at $1B+ MC. Or how $POET, is worth ~9-10x more than its laser supplier. When $SIVE, the mini $LITE equivalent for CPO/Silicon photonics, is valued at $140M. I do believe this is largely undiscovered by institutions, since this is some random company in OMX Nordic Exchange (similar to micro $AXTI before I started posting about the inp substrate bottleneck). But I do think it will get a lot of institutional attention as Celestial and Ayar scale up. Especially if $POET and $SIVE gets qualified with other customers. If CPO completely replaces pluggable transceivers in the next generation of hyperscaler architectures. Sivers, with possible WIN Semi qualifcation and if they become the multi-source lasers for NVIDIA, Marvell, Intel, and Broadcom architectures, can be strongly rerated. Just as how $LITE did today going from $16 -> $622. This is just my personal thesis I'm sharing, DYOR/NFI. TLDR: InP Lasers are the current bottleneck in photonics as seen with $LITE valuations. $SIVE looks like the mini $LITE for the upcoming CPO/Silicon Photonics ramp. I personally took long position in $SIVE, as I believe they’re a large beneficiary of the upcoming silicon photonic/CPO architectural changes by $NVDA (with GTC cataylst). The upside here just way too compelling for me personally as the next possible $LITE.

$5,000 Gold: The New Floor Is Here? But Silver Has Massive Upside and Could Beat Gold in 2026 Watch now: youtu.be/KOwgX5VPaWs #stocks #gold #silver #economy #dollar @DanielaCambone

It's awesome to build applications with prompts - but what about the path to production? Enter Palantir's newest application builder: Pilot...

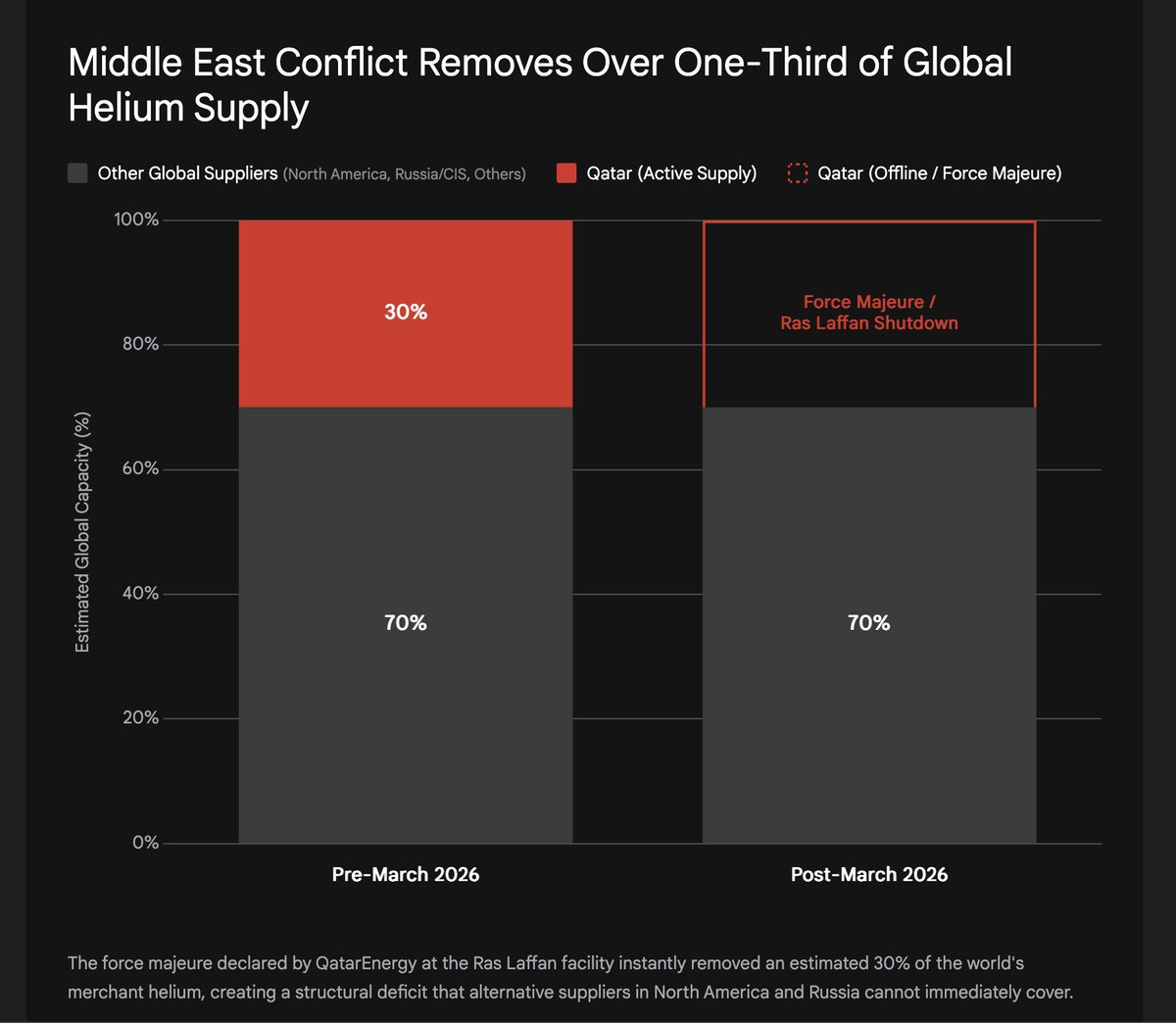

The Strait of Hormuz has been closed for 8 days. Everyone thinks this is about oil. This is about what oil becomes. 92% of the world's sulfur comes from refining oil and gas. Close the Strait of Hormuz and you don't just lose 20 million barrels of crude per day. You lose the feedstock for sulfuric acid, the single most produced chemical on Earth. Sulfuric acid is how we extract copper. It's how we extract cobalt. Without it, you can't make transformers, EV batteries, or the substrates inside every data center on the planet. One chemical, made from one feedstock, shipped through one chokepoint. The cascade goes further: Qatar ships 30% of Taiwan's liquefied natural gas through Hormuz. Taiwan has 11 days of reserves left. TSMC, the company that makes 90% of the world's advanced chips, draws 8.9% of Taiwan's total electricity. No gas, no power, no chips. Then food. 33% of the world's nitrogen fertilizer feedstock moves through the Strait. Half of all humans alive today exist because of synthetic nitrogen. Sulfur, semiconductors, food. That makes three supply chains, one 21-nautical-mile chokepoint, and zero domestic alternatives at scale.

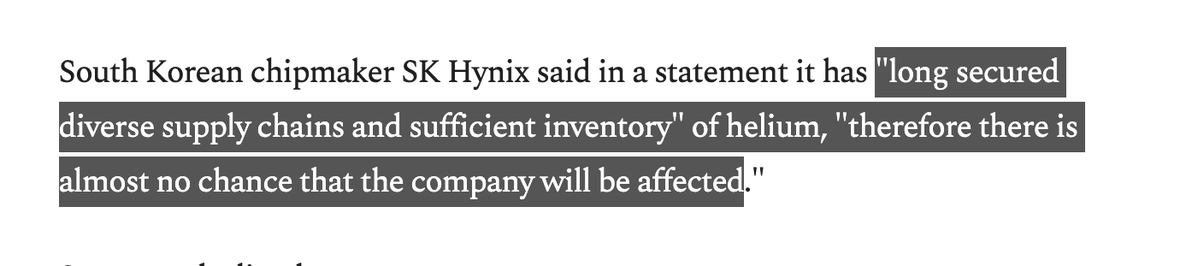

If the Hormuz were closed, it looks like 80% of South Korea’s LNG imports would be unaffected. And looks like $EWY SK Hynix and Samsung are largely diversified since 2022. People are quoting majority of all LNG flowing through the Strait of Hormuz (~59%) goes to just four Asian countries: South Korea, Japan, China, and India. Looks like a scary number, but that’s just a fraction of their total imports. Roughly four-fifths of imports already arrive via Hormuz-free routes: Australia (24.6%), US (12.2%), Malaysia, Indonesia (~20%), and Russia/Sakhalin (~4.6%). Then 82% of 2024 imports for example were long term contracts, not spot. So any hiked rates for new price hikes would be largely insulated. Even if they did, costs would be passed onto hyperscalers. Looks like South Korea learned their lesson from 2022 and diversified sources + added long term pricing contracts.