Dimitry Nakhla | Babylon Capital®@DimitryNakhla

Warren Buffett on the ratings agencies:

“The ratings agencies have had and still have under current conditions an incredibly wonderful business. It takes no capital at all, the pricing power is significant.”

Buffett was talking about $SPGI and $MCO. Let’s focus on $SPGI.

What makes $SPGI specifically extraordinary is what sits alongside the 𝐑𝐚𝐭𝐢𝐧𝐠𝐬 𝐛𝐮𝐬𝐢𝐧𝐞𝐬𝐬 — the 𝐈𝐧𝐝𝐢𝐜𝐞𝐬 𝐛𝐮𝐬𝐢𝐧𝐞𝐬𝐬.

Together, these two segments represent perhaps the most capital-light, pricing-power-rich combination in public markets.

𝐑𝐚𝐭𝐢𝐧𝐠𝐬 𝐨𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐦𝐚𝐫𝐠𝐢𝐧𝐬: 𝟔𝟒.𝟑𝟒% (𝐋𝐓𝐌)

𝐈𝐧𝐝𝐢𝐜𝐞𝐬 𝐨𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐦𝐚𝐫𝐠𝐢𝐧𝐬: 𝟔𝟖.𝟗𝟗% (𝐋𝐓𝐌)

Both above 60%. Both requiring virtually no capital to sustain. Both collecting tolls on the global financial system whether markets rise or fall — ratings on every bond issued, indices on every dollar of AUM benchmarked against the S&P.

And the quality of the entire business is set to improve further. $SPGI is divesting its Mobility division — a business running at 21.62% operating margins (LTM). Removing the lowest-margin segment from the portfolio concentrates the earnings power in the two strongest segments. The business gets cleaner, higher-margin, and more focused.

Now the valuation.

𝐋𝐓𝐌 𝐨𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐩𝐫𝐨𝐟𝐢𝐭 𝐟𝐫𝐨𝐦:

𝐑𝐚𝐭𝐢𝐧𝐠𝐬: $𝟑.𝟏𝟒𝐁

𝐈𝐧𝐝𝐢𝐜𝐞𝐬: $𝟏.𝟑𝟑𝐁

𝐂𝐨𝐦𝐛𝐢𝐧𝐞𝐝: $𝟒.𝟒𝟕𝐁 — from just two segments. At today’s market cap of $119B, you are paying approximately 26x LTM operating profit for those two businesses while the overall portfolio quality is actively improving.

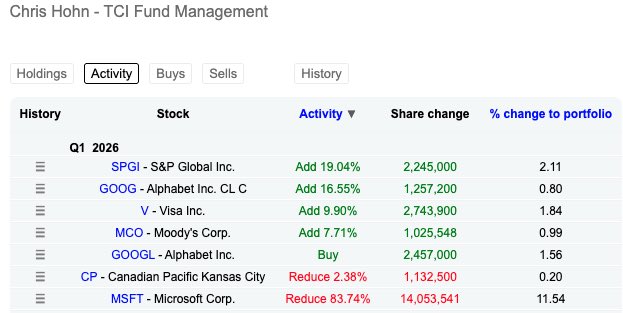

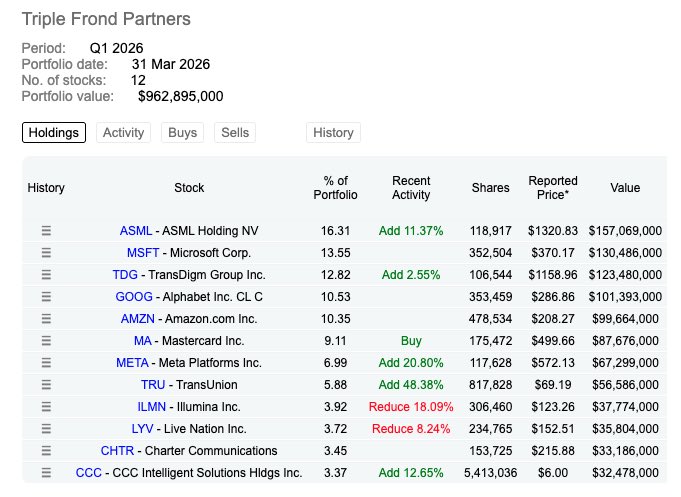

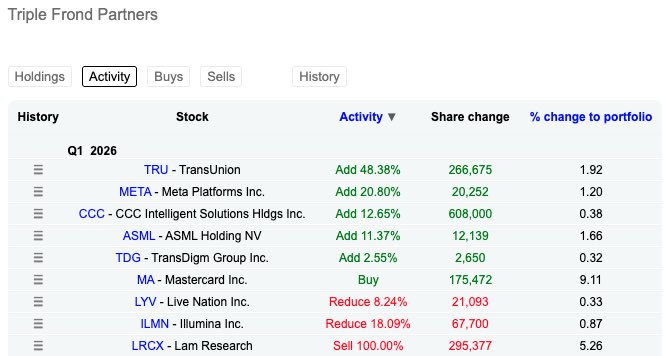

It appears Chris Hohn, Pat Dorsey, and Li Lu — among the most rigorous fundamental investors in the world (as well as recent $SPGI insider purchases) — are seeing exactly this in their latest 13Fs.

Sometimes the best ideas aren’t hidden. They’re hiding in plain sight and you just have to be a contrarian with strong conviction and patience.

___

🎙️ Berkshire 2010 Annual Meeting | CNBC Warren Buffett Archive