@WinnerInvestor They reported 14.7 MM in the Q1 2026 earning call. Hope they surpassed 15 million little while back.

English

TheEquityPulse

41 posts

@EquityPulse20

Decoding market data into actionable logic. Grounded in data. Logic over noise.

$SOFI None of that matters. It’s the loan book. Always the loan book. They raised capital twice in six months… why? Exactly — to keep piling on more unsecured loans. This will keep haunting the stock until they prove they can move those loans off the balance sheet fast. Who’s buying all those loans? You guessed it… Private Credit. And what's happening to them? They're not doing so well. Hence Sofi is in the dumpster. Yea yea.... I understand they made over $600M on net interest income. But none of that matters when you can’t unload those loans to private credit — especially the moment unemployment ticks up.

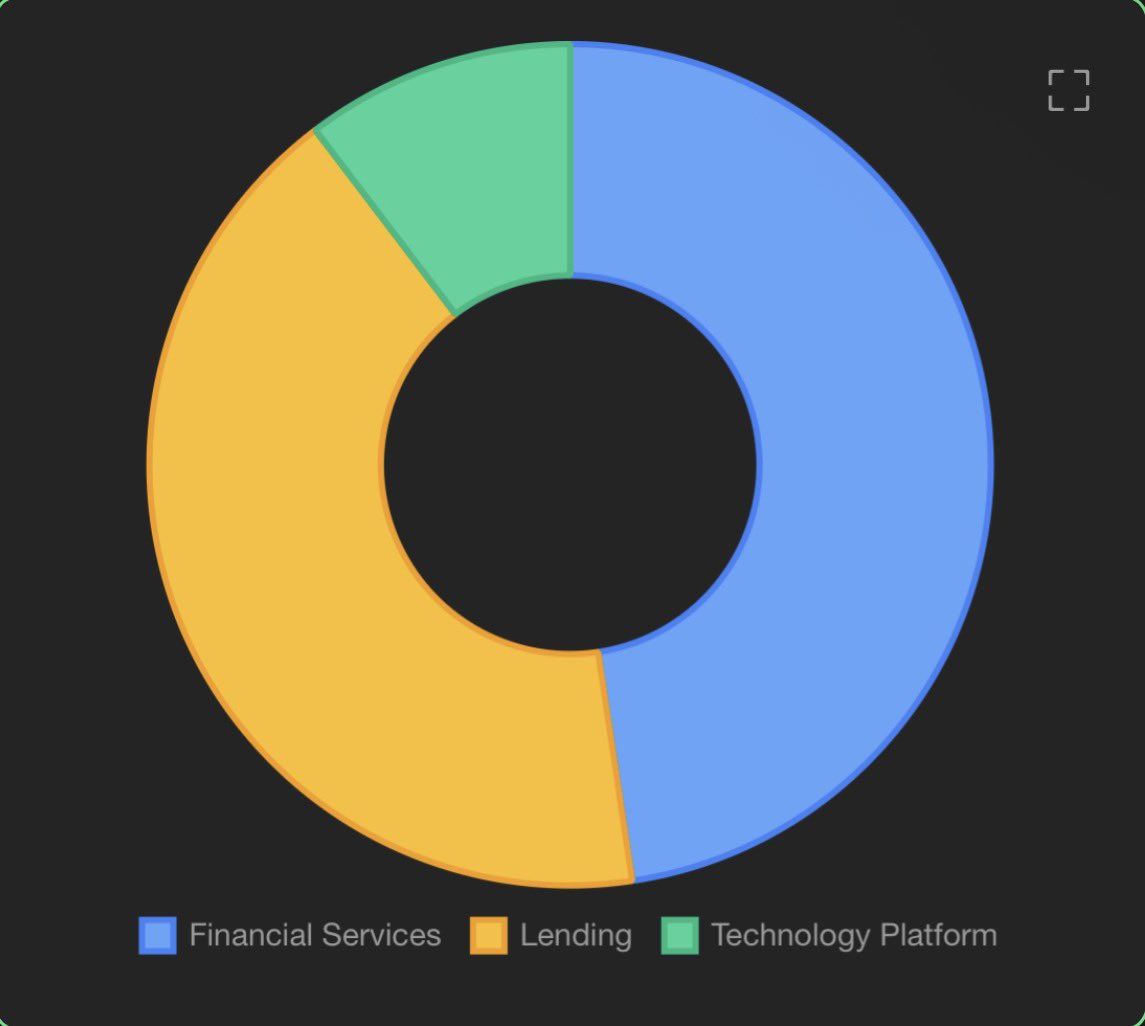

When $SoFi went to $32 was it because of the tech platform?

I can see how one might feel that way. But mostly no and this is the argument you can give anyone who might be just early days thinking about the financial sector and lending: Bad lending, subprime lending, potentially yes. Long duration lending, also maybe, if you have someone too young who doesn't understand the concept of duration ($UPST, had literally no one with any kind of longer resume and I'm not sure if that has been corrected) High credit rating, short duration lending? No, in general and also compared to all of emerging fintech. The type of lending $SOFI does is very stable. fairly predictable, and that is before you layer in the strategic advantage $SOFi carries right now by being so liquid and it's specific funding and asset mix going into that part of the market. The major macro risk to $SOFI is ONLY the following: A rising rate environment where you ALSO have 2 other features, 1) an attack on illiquid assets such that private equity can no longer continue to get their returns off of liquid assets and must force sell to raise capital 2) some macro weakness that specifically attacks higher credit quality individuals. You need both, b/c if you only get 1 or the other, money will need to go the asset class that is the safest and that would mean a) decrease duration b) improve credit quality of assets. In contrast, fintech, particularly emerging fintech, is a simple porter's 5 forces analysis. Any emerging tech or new tech can create massive substitutes or new entrants that can take them out. And right this minute, given what's happening in AI AND ALSO, it's impact to the regulatory changes that are happening in blockchain and also banking, that is a FAR greater risk. Those changes actually help most banks/not hurt as - in general - they do less disruption and more reduction of the most expensive cost any financial firm has (labor). Hope that clarifies.