The Bullish Broke Guy X

9.1K posts

The Bullish Broke Guy X

@EthGoldi

I trade, I lose, I learn. Surviving the markets one dip at a time 📉💪 markets & madness - one viral post at a time. #Investing #AI #Finance. Not Advice

Real 🌏 Katılım Eylül 2021

58 Takip Edilen1.5K Takipçiler

דל"פ: ניר דבורי צודק.

בתחילת השבוע הוא אמר בשידור: "בסוף, בשורה התחתונה, אנחנו נכנסים לשבוע הרביעי. זה יהיה שבוע מרכזי שיוביל אולי בסופו אל תחילת ההתלבטות כיצד להמשיך את הדרך."

וכולם התנפלו עליו.

אולי במקומו הייתי משנה את הניסוח, אבל לגמרי הבנתי למה הוא התכוון.

למה?

כי לפני שבועיים בערך ניהלתי איתו את הוויכוח הזה בשידור אצל רפי רשף, וגם אחרי שיצאנו מהאולפן המשכנו לשוחח. אני טענתי שאני לא מבין מה יש להפציץ שם ארבעה עד שישה שבועות. הוא אמר לי: בוא ניתן לצה"ל לנצח ואז נראה איפה אנחנו עומדים. Fair point.

אז יאללה, זרמתי איתו, וזה גם לא שמישהו באמת שאל אותי.

והופס, נחתנו בבאזל. הננו כאן.

הטענה של דבורי היא כזו: אנחנו בסוף השבוע הרביעי.

מסיימים את השלב הראשון של תקיפת היכולות הצבאיות של איראן. עכשיו בואו נדבר על מה הלאה.

התקיפות אתמול רק מוכיחות את זה. אם הגענו למצב שאנחנו תוקפים את הכור באראק (גם אם לא תקפו את הכור עצמו אלא את מתקן ייצור המכ"ד הטיעון עצמו לא משתנה) ואת מפעל העוגה הצהובה ביזד, סימן שאלו המטרות הערכיות ביותר שנשארו לנו.

ובחיאת, תחסכו לי. אם הם היו כל כך חשובים, היו תוקפים אותם בתחילת המלחמה.

אז אם נשארו חימושים גם למטרות האלו, אנחנו כבר עמוק בגארבג' טיים.

תקיפת מפעלי הפלדה היא כבר סיפור אחר. זה לא יעד צבאי קלאסי, אבל גם עוד לא מעבר לאסקלציה כלכלית כבדה. זה יפגע באופן מסויים ביכולת שלהם לייצר טילים אבל עם נזק שיורי משמעותי לכלכלה. בעיניי זו בעיקר פעולה שאומרת - תראו לאן אנחנו יכולים ללכת אם נרצה.

אני לא חושב שבגיחת הפצצה אחת ייצרנו שם נזק של מיליארדים, ולכן גם זה לא איזה גיים צ'יינג'ר. זה בעיקר איתות.

המשמעות היא שאנחנו מתקרבים למיצוי השלב הזה. המטרות הצבאיות שאנחנו תוקפים כבר לא כאלה רלוונטיות, ובטח שלא מצדיקות המשך קמפיין אווירי מאסיבי.

האם השגנו הכרעה? לא. רחוק מכך.

בתחום הגרעין, הנכס המשמעותי ביותר, האורניום המועשר, עדיין באיראן.

מבחינת יכולות הטילים, על פי צבא ארה"ב מאתמול, רק שליש הושמדו, ועכשיו אנחנו במוד של צייד סיזיפי. גם פגענו להם ביכולות הייצור של טילים עתידיים.

איראן עברה למוד של מלחמת התשה, וכנראה יכולה להמשיך בקצב הירי הנוכחי במשך שבועות, ואולי אפילו חודשים ארוכים.

מנגד, לא ברור מה מצב המיירטים שלנו ושל מדינות האזור, והאם נוכל להמשיך לתת את אותה רמת הגנה לאזרחים. אני לא צריך שיפרסמו מספר, זה לא משהו שהציבור צריך לדעת, אבל אני מוכן להמר שגם אנחנו בכלכלת חימושים.

איראן הצליחה להתמודד באופן סביר עם הפגיעה בהנהגה הצבאית והפוליטית על ידי מימוש "הגנת פסיפס", כלומר חלוקה לתתי יחידות שכל אחת יודעת לעבוד באופן עצמאי גם אם איבדה קשר לפיקוד המרכזי.

זה לא מפתיע אותי. אני שנים מתייחס ל"פרקטל האיראני", ליתירות שהם מייצרים בכל דבר, עד לרמה הקטנה ביותר.

לדוגמה: גם כשצריך לרכוש איזה רכיב לתוכנית הגרעין או הטילים, הם ינסו לרכוש כמה דגמים, וכל דגם הם ינסו להשיג בכמה וכמה ערוצי רכש.

עוד דוגמה: הם פיתחו פאקינג 29 סוגי טילים וכטב"מים. יותר ממספר סוגי הקורנפלקס על המדף בסופר.

נכון, זה לא יעיל, ואפילו מאוד בזבזבני. זה גם מקשה מאוד על האיראנים לרכז מאמץ.

אבל זו אסטרטגיה טובה אם אתה לא רוצה שיהיו צווארי בקבוק שפגיעה בהם תמנע ממך להשיג את המטרה שלך.

האסטרטגיה הזו היא מה שהפך את איראן לכלכלה כושלת, אבל היא גם זו שמאפשרת לה להחזיק מעמד כרגע.

אז בקיצור: זה לא שאנחנו לא מנצחים. זה האיראנים שלא מפסידים מספיק.

ומהגנה להתקפה: איראן הצליחה לייצר עבור עצמה נכס אסטרטגי, סגירת מיצרי הורמוז.

היא מחזיקה את הכלכלה העולמית בביצים.

אני מנסה להחדיר לשיח הציבורי את הביטוי שאיראן תופסת את העולם בהורמוז, תעזרו לי בבקשה.

זה לא רק 25% מהנפט שעובר שם, אלא גם אחוז נכבד מהגז הטבעי ובערך שליש מתעשיית הדשנים העולמית עובר דרך המיצר.

האיראנים מחזיקים את האנרגיה והחקלאות העולמית כבנות ערובה, והביאו למצב ששחרור המיצר, שהיה פתוח לפני 28 בפברואר, הופך למטרת מלחמה בפני עצמה.

ופה כבר אפשר להגיד שמדובר בכישלון אמריקאי.

בכל משחק מלחמה שאני השתתפתי בו, איראן סגרה את המיצר.

שערורייה שלא הייתה תוכנית צבאית נורמלית להשאיר אותו פתוח בזמן סביר.

שורה תחתונה: איראן נמצאת בעמדה לא רעה בכניסה למו"מ עם האמריקאים. הזמן לאו דווקא משחק לרעתה, בטח כל עוד המיצר סגור והטילים ממשיכים לעוף. ה BATNA שלהם היא פשוט להמשיך.

אז בואו לא נתבלבל. למלחמה היו שלוש מטרות:

מטרה ראשונה: שינוי משטר.

למרות שלא הוצהרה כמטרה מפורשת, ברור שהיא שם למעלה. כרגע נראה שבטווח הקצר המשטר מחזיק. למרות הסרטונים המרשימים של תקיפת עמדות בסיג', המעט שיוצא מהמדינה מראה שהמשטר עדיין מחזיק לא רע. זה יכול להתהפך תוך ימים, אבל לבנות על זה עכשיו כתמונת ניצחון ולהמשיך את המלחמה עד שזה יקרה, זו אסטרטגיה מטומטמת. אני עדיין חושב שהמשטר הזה מושחת וכושל והוא ייפול מתישהו בקרוב, אבל זה גם יכול לקחת עוד כמה שנים, ולא ברור שיש דרך לזרז את זה שלא עוברת דרך טנקים אמריקאים בטהראן.

מטרה שניה: מניעת גרעין.

אם אתם עוקבים אחרי, אתם כבר יודעים שהמשמעות של זה בפועל היא הוצאת האורניום מחוץ לאיראן. אולי יש מבצע צבאי בקנה. לא יודע. בטח שזה לא מבצע פשוט. הדרך הכי אפקטיבית ואלגנטית להוציא אותו היא בהסכם הפסקת אש. פירטתי בפוסט נפרד השבוע למה אני חושב שתיאורטית זה אפשרי.

מטרה שלישית: שחיקת היכולות הצבאיות של איראן.

מה שאפשר להשיג בקלות יחסית כבר השגנו. עוד שבוע או שבועיים לא ישנו דבר.

שלא תבינו אותי לא נכון, אני לא אומר שהפגיעה לא משמעותית. ז**נו אותם.

אבל מכיוון שאני כבר מצליח לשמוע מהבית שלי את המצעדים של חמאס ברצועה, למה אנחנו חושבים שהאיראנים לא יצליחו להשתקם מזה?השלב המהותי הבא יהיה רק אם מוכנים להיכנס למלחמה שתיקח עוד חודשים ארוכים, אולי אפילו שנה. ואז המספרים הקטנים של תקיפה פה או שם יתחילו להצטבר.

לא נראה לי שארה"ב מוכנה לזה.

אז מה הלאה?

כמו שדבורי אומר, אפשר להתחיל את ההתלבטות לגבי המשך הדרך.

גם כאן, בגדול, שלוש אופציות:

אופציה ראשונה: להגיע להסכם הפסקת אש מול איראן.

אין מצב להסכם מלא, אבל אולי אפשר להשיג הסכם חלקי שבו הורמוז פתוח, ואולי אולי גם האורניום מחוץ לאיראן. אני חושב שכרגע הסבירות לכך נמוכה, לאור העמדות ותחושת העמידות של שני הצדדים. או כמו שאיציק שאשו כתב השבוע, במו"מ בין בני יהודה לויניסיוס יש פחות פערים.

אופציה שניה: אסקלציה.

לדעתי זו האופציה הריאלית. יכול להיות שיימשכו כמה שבועות של מו"מ עקר ואולטימטומים, רק כדי לבנות את הכוח הנדרש. המרינס בדרך, אולי גם עוד כוחות. מבחינת ארה"ב יש כמה סוגי אסקלציה: פעולה קרקעית מוגבלת להשגת האורניום, פתיחת מיצרי הורמוז או כיבוש אחד האיים, חארג או האיים ששולטים על המיצר, או תקיפה של תשתיות אזרחיות קריטיות - תשתית החשמל המדינתית, שתגרור ביקורת בינלאומית, או תשתית ייצור הנפט, שתגרור עצבנות בשווקים.

הבעיה העיקרית בתרחיש הזה היא שלא ברור האם הוא יביא את איראן להתגמש במו"מ. במידה רבה, האיום באסקלציה הרבה יותר משמעותי מהביצוע שלה בפועל, כי אחרי שהוא קורה, מה כבר יש למשטר להפסיד?

מבחינת האיראנים יש עוד מדרגות אסקלציה, כמו מיקוש כל המיצר ופגיעה בתשתיות אנרגיה באזור, אבל אני חושב שדווקא כאן היד שלהם חלשה. לא חושב שהם יוכלו לעשות נזק משמעותי הרבה יותר ממה שהם כבר עושים.

קלף אחד שהם עדיין לא השתמשו בו הוא החות'ים, שיכולים לסגור את מיצרי באב אל מנדב ולעצבן עוד יותר את השווקים. גיים צ'יינג'ר? לא בהכרח.

הרבה יותר מעניין יהיה לראות אם האמריקאים מצליחים לפתוח את הורמוז צבאית. כרגע זה לא נראה בכיוון, ובטח שלא מהר.

מה יקרה אחר כך? נקבל עוד פיוט של דבורי, ונחזור להתלבטות כיצד להמשיך את הדרך, בהתאם לסיטואציה. כרגע יש יותר מדי משתנים כדי לנבא.

אופציה שלישית: להמשיך את המצב הקיים לאורך זמן.

זו האופציה הכי גרועה. ההישגים שלנו יישחקו, והאיראנים רק ימשיכו להרגיש על הסוס כי הם מחזיקים מעמד מול אמריקה הגדולה. העולם, שבינתיים לא מפעיל לחץ אמיתי על אמריקה לסיים את האירוע, יתחיל לתת איתותי אמת.

עזבו את מחירי הנפט, שזה האובייס. בטווח הבינוני אנחנו יכולים לראות קריסה של הדולר כמטבע הדומיננטי במסחר בינלאומי ועליית חלופה של היואן הסיני. זה האיום האסטרטגי האמיתי.

האופציה הרביעית, שיכול להיות שנגיע אליה, היא שהאמריקאים פשוט יחתכו הפסדים ויכריזו שניצחנו.

אם דוברת הבית הלבן קרולין לויט הצליחה להסביר השבוע שבעצם כבר יש שינוי משטר באיראן, אז גם למסגר את המלחמה כניצחון יהיה קטן עליה. אפילו מוכר רהיטים יכול לעשות את זה.

בקיצור, את ליל הסדר כבר הבנו שאנחנו הולכים לעשות בממ"ד. אפשר כבר להסתכל על יום העצמאות, ואולי גם ל"ג בעומר ושבועות.

אחר כך כבר ראש השנה ובחירות גם פה וגם באמריקה.

ניפגש אחרי החגים. השאלה היא איזה חגים. סטיי סייף.

עברית

$67.6B in Net Worth. $6.6B Market Cap. The market is pricing a fortress like a liquidation sale.

Our daily watchlist scan flagged $FMCC (Freddie Mac) this morning. Not because of a price drop, but because of a volume anomaly disconnected from fundamentals. While the street chases AI high-flyers, the most profitable machine in America is trading at ~2x earnings and 0.1x book value. This isn’t a “value trap”—it’s a regulatory hostage situation nearing a breakout.

THE ASYMMETRIC SQUEEZE

📉 Valuation Disconnect: Latest 10-Q confirms Net Worth hit $67.6B in Q3 2025. That’s up from $56.4B a year ago. The stock price? Flat. The “Value Gap” has widened to over $60 billion.

🏛️ Macro Catalyst: The Trump administration is officially “opportunistically evaluating” a conservatorship exit by end-2025. This moves the thesis from “if” to “when.”

💰 Earnings Power: $3.1B in Net Income for Q3 alone. Annualized run rate of ~$12B against a market cap of ~$6.6B. You are buying the engine for the price of the tires.

🔍 Insider Signal: Zero open-market sales. The capital structure is locked, and the smart money knows the only exit is a recapitalization that unlocks the common.

My Take

This week’s decision-quality review highlights a rare “fat pitch.” Most investors are over-analyzing rate cuts while ignoring capital structure catalysts. The risk here isn’t business quality—delinquencies are near historic lows and the guarantee book is pristine. The risk is political timing. But with the Net Worth chart going parabolic (see below) and the political wind shifting, the “conservatorship discount” is the most mispriced risk premium in the market. We are effectively holding a call option on the US housing finance system with no expiration date.

The math is simple: The government needs the money. The shareholders own the equity. Eventually, the two align.

Bullish 🦅

English

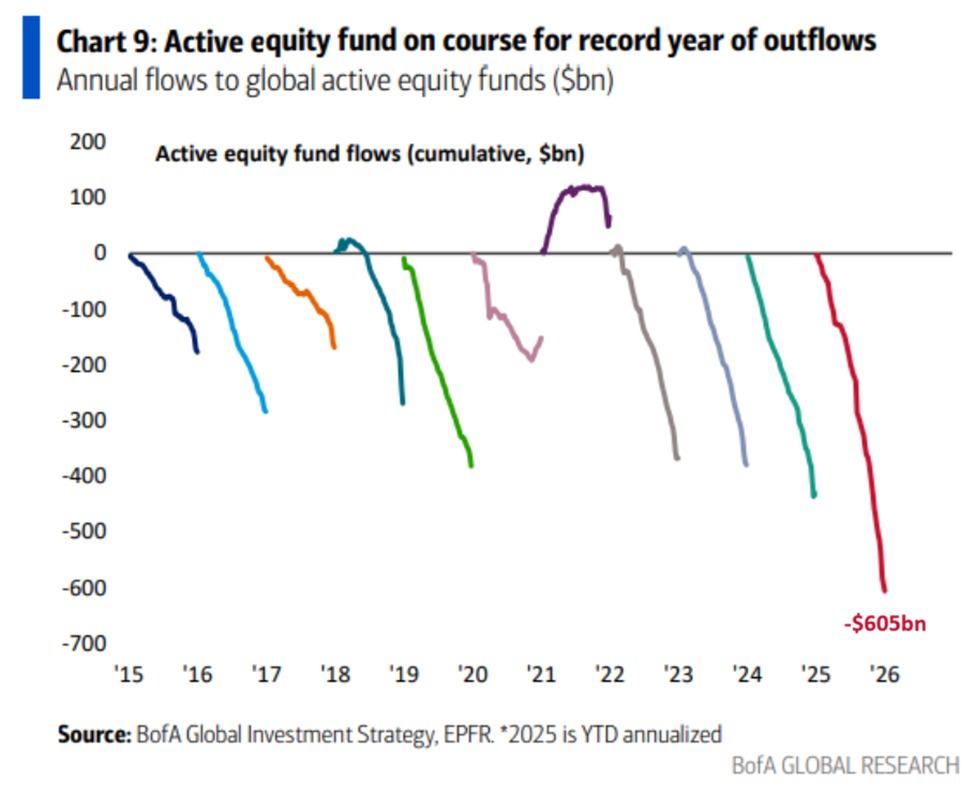

📉

Stock picking isn’t dying. It’s being outsourced to indices.

A projected -$605B in outflows from active equity funds this year, with cumulative -$3.1T over 11 years, is not noise it’s regime change. When only 29% of large‑cap managers are beating the benchmark, versus a long‑term average of 37%, allocators are doing the rational thing: they are firing humans and hiring the S&P 500.

THE GREAT ROTATION

This is what the active‑vs‑passive shift really means in flows and structure:

📉 Structural Redemption: Outside of a few niches, active equity has logged net outflows in 10 of the last 11 years, culminating in the current record. That is not a cycle; it’s a melting ice cube.

📈 Passive as Default: Over the same window, passive equity funds have absorbed trillions in inflows and now dominate new capital, with 2025 likely adding ~trillion‑plus yet again. The benchmark is no longer the yardstick; it’s the product.

🎯 Alpha in the Tail: With only ~1/3 of managers beating after fees (and less in US large caps), investors are deciding that stock picking is an occasional satellite, not a core holding.

MY TAKE 🎯

Active management isn’t “dead,” but it has become a niche skill sport in a world that prefers cheap beta. The paradox: as more capital crowds into passive vehicles like $SPY and $VOO, index construction itself becomes the biggest active decision in markets. For truly active strategies that are unconstrained, concentrated, and genuinely different from the benchmark, this may quietly be the best hunting ground for alpha in 20 years because the competition is bleeding AUM and career risk is forcing everyone else into closet indexing.

Bullish 📉

English

Active fund managers are struggling:

Investors are on track to withdraw a record -$605 billion from global active equity funds this year.

This surpasses the previous record of -$450 billion.

It also marks the 10th annual outflow over the last 11 years.

Over this period, active equity funds have recorded -$3.1 trillion in net outflows.

Meanwhile, only 29% of large-cap mutual funds are outperforming their benchmarks year-to-date, the lowest percentage since 2019.

This is far below the 37% average since 2007.

Active management is in a sharp decline.

English

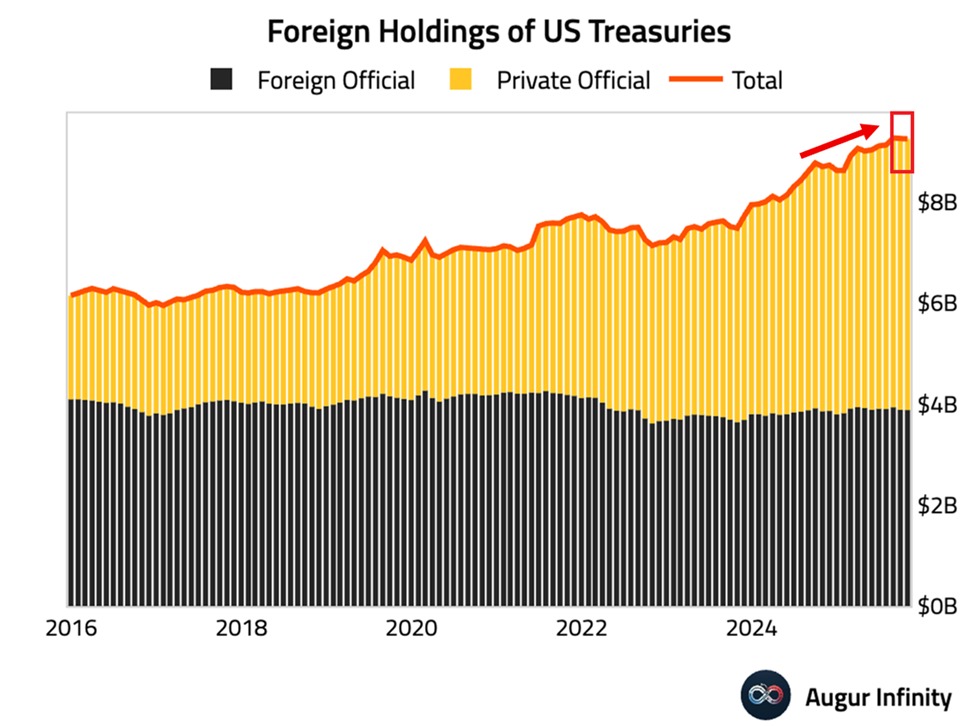

Ignore the “China is dumping” fear porn. Total foreign holdings are still near record highs ($9.2T). The demand for the US Dollar as a collateral layer is untouched. What we are seeing is Geopolitical Structuring countries are moving their stack from “Direct Ownership” to “Custodial Proxies” to protect against potential asset freezes. The plumbing is changing, but the water is still flowing to Treasury.

English

BREAKING: Foreign holdings of US Treasuries fell -$5.8 billion in October, to $9.2 trillion, but remain at the 2nd-highest level on record.

China’s holdings, the 3rd-largest holder, declined -$11.8 billion, to $688.7 billion, the lowest since 2008.

However, Belgium’s stockpile, which includes Chinese custodial accounts, rose +$1.6 billion, to a record $468.4 billion.

Japan, the largest foreign holder of Treasuries, posted a +$10.7 billion increase, to $1.2 trillion, the highest since July 2022.

The UK, the 2nd-biggest owner, saw a +$13.2 billion surge, to $877.9 billion, the 3rd-highest on record.

Meanwhile, Canadian holdings dropped -$56.7 billion, to $419.1 billion, the lowest since July.

Demand for US Treasuries remains strong overall.

English

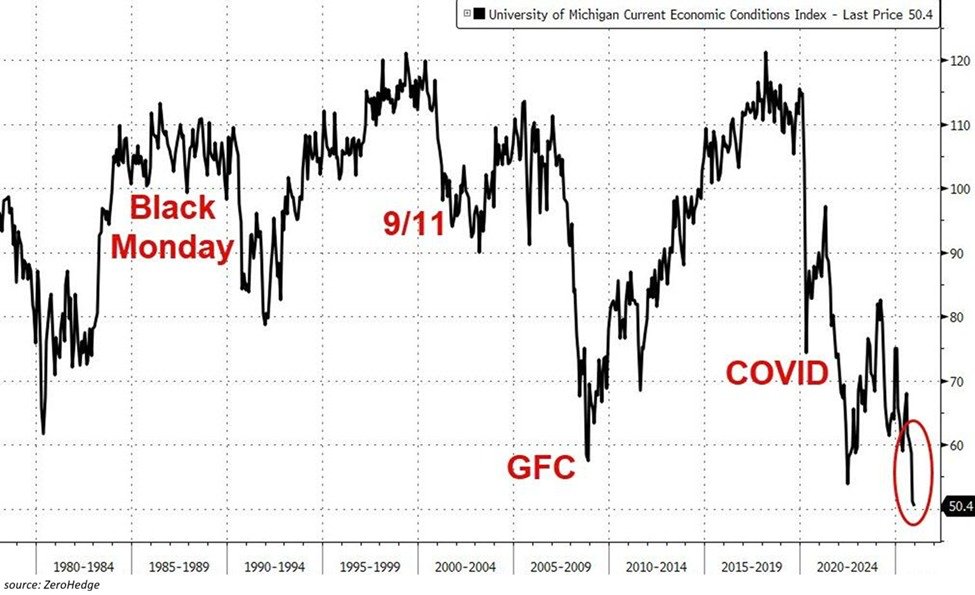

This 50.4 print is the green light for the Fed to panic. They cannot keep rates restrictive when the consumer is screaming “Depression.” Bad news is about to become the ultimate buy signal for duration assets $TLT .The equity market $SPY might hate the earnings recession, but it will love the liquidity injection that comes to fix it. We are at peak pessimism, which is usually exactly when the money printer turns back on.

English

BREAKING: The US consumer sentiment assessment of current economic conditions has declined to 50.4 points, the lowest level on record.

This is 5 points and 8 points below the lows seen in 2022 and 2008.

By comparison, the index stood 11 points higher in 1980, when annual inflation was at 13.5%.

This comes as Americas' perception of current buying conditions for big-ticket items deteriorated to the lowest level on record.

An ongoing affordability crisis and a weakening labor market continue to weigh on household finances, dragging consumer sentiment lower.

Consumers have rarely been this pessimistic about the economy.

English

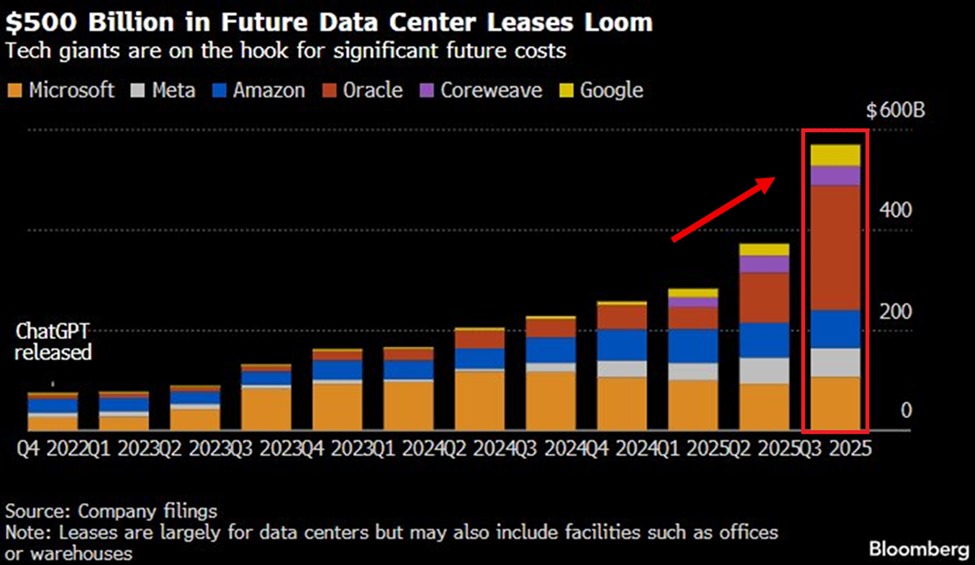

The AI boom is accelerating:

US tech companies are committing to spend a combined $569 billion on data center leases over the next several years.

A lease is a long-term rental agreement, meaning these companies commit to multi-year payments for data centers, offices, or warehouses, without owning them upfront.

This represents a +$197 billion, or a +53% increase from Q2 2025.

Oracle, $ORCL, alone added +$148 billion in new lease commitments in Q3, bringing its total data center lease obligations to $248 billion.

Some of these leases can last up to 19 years, locking Oracle into massive fixed costs regardless of future AI demand.

Tech companies are making massive bets on AI.

English

This slide is the purest expression of the current AI regime: tech is swapping variable cloud flexibility for locked‑in, utility‑like obligations. In portfolio terms, $ORCL is no longer just software; it’s a quasi‑infrastructure name with embedded power and utilization risk. The market is still valuing many of these names like high‑margin software while they quietly morph into capital‑intensive utilities. That mispricing cuts both ways: if the AI demand curve is real, earnings power is being structurally underpriced; if not, this is how an AI bubble turns into a margin recession.

English

🖨️

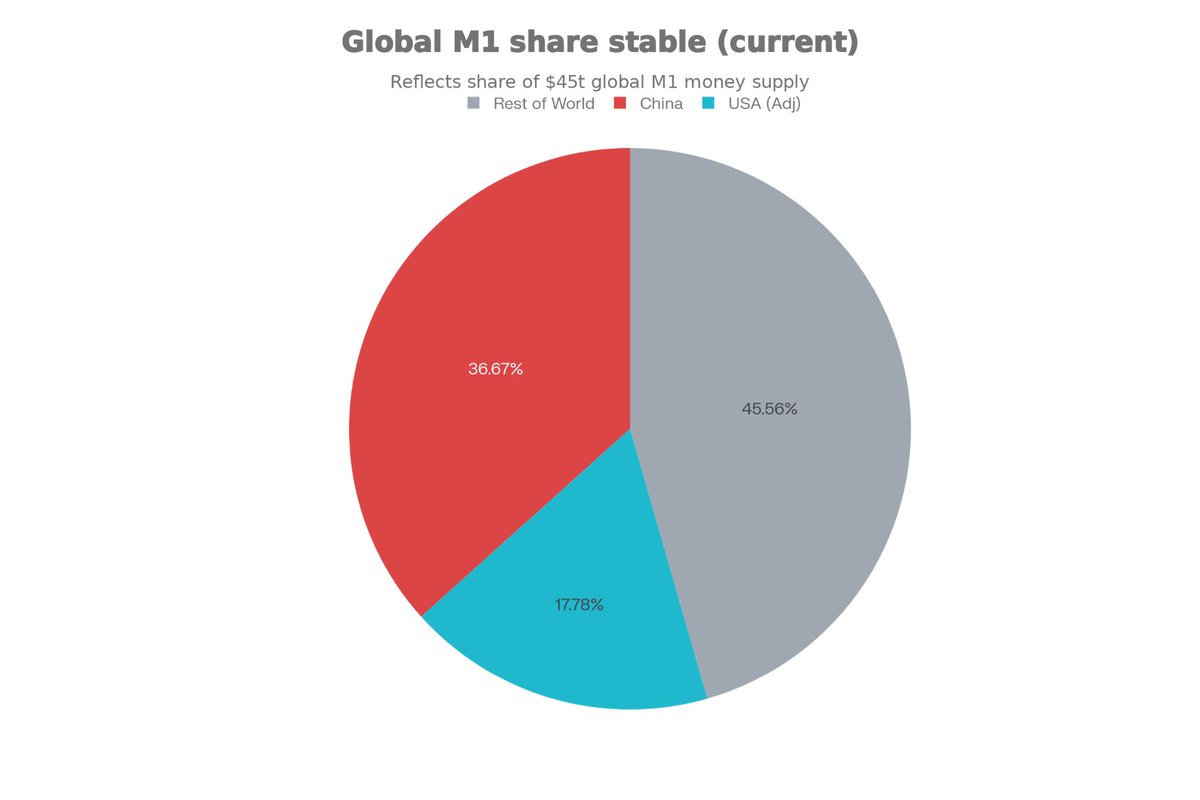

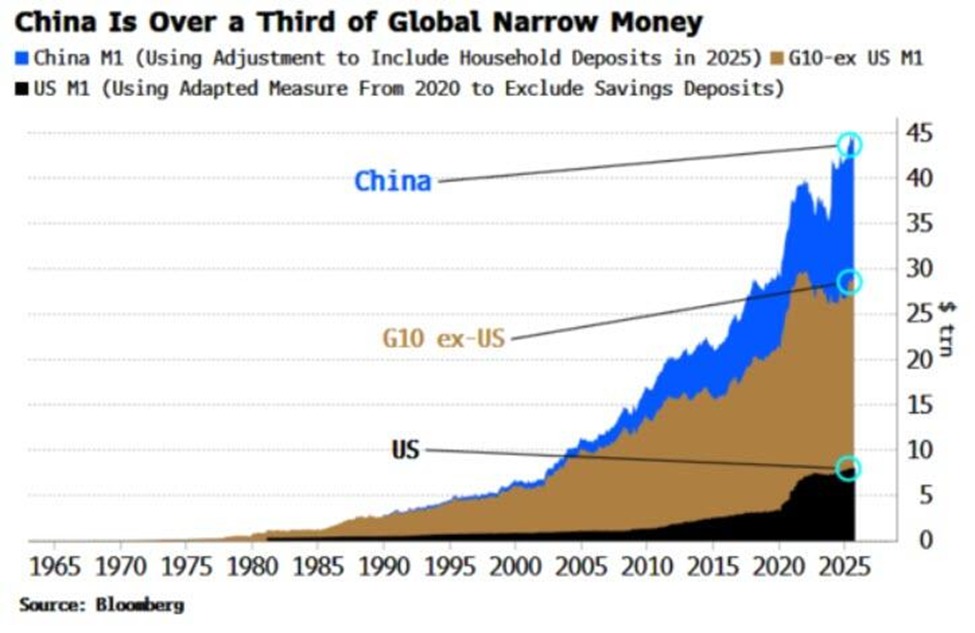

The Fed is loud. The PBoC is lethal.

Everyone is obsessed with Jerome Powell’s 25bps cuts, but they are watching the wrong central bank. The real liquidity hose is now in Beijing. With China’s M1 hitting an all-time high of $16.5T, they are effectively printing a new “Germany” worth of cash every few quarters. The US is no longer the main character in the global liquidity story; we are the supporting actor.

THE GREAT ROTATION

Global M1 hitting $45T isn’t just a number; it’s a signal that fiat debasement is now a competitive sport.

🧲The 2:1 Ratio: For every dollar of “narrow money” the US creates, China is creating nearly two. This explains why Chinese equities ($FXI) are waking up despite their deflationary macro data.

🧲The Silent Inflation: We look at US CPI and think we won. But global liquidity always finds a home. If it’s not in US goods, it flows into hard assets.

🧲The Shadow Stimulus: While the US fights over “fiscal discipline,” China is flooding the plumbing. This money doesn’t stay behind the Great Firewall; it leaks into commodities, crypto, and luxury assets globally.

My Take 🎯

We are witnessing a “Liquidity Handover.” The US is fiscally constrained by debt interest, but China is desperate to reflate. This specific $8.5T gap between China and US M1 is the bullish case for scarcity. When the world is drowning in paper, you buy the things they can’t print. The next bull run won’t be funded by Wall Street; it will be funded by the People’s Bank of China.

Bullish 🖨️

English

We are witnessing a “Liquidity Handover.” The US is fiscally constrained by debt interest, but China is desperate to reflate. This specific $8.5T gap between China and US M1 is the bullish case for scarcity. When the world is drowning in paper, you buy the things they can’t print. The next bull run won’t be funded by Wall Street; it will be funded by the People’s Bank of China.

English

Global money supply is out of control:

Global money supply is now up to a record $45 trillion.

This comes as China's M1 money supply has risen to $16.5 trillion, an all-time high.

China has driven the majority of global money supply growth this year.

China is currently the largest producer of narrow money in the world, accounting for ~37% of the total.

Meanwhile, the US M1 money supply, excluding savings deposits, is up to a record $8 trillion, representing ~18% of the world's total.

Global liquidity is expanding.

English

This is financial engineering at its peak. If this executes, $TSLA stock stops trading on auto margins and starts trading as a holding company for the Musk Economy. The “insane amount of work” Musk mentions is just code for regulatory hell, but the signal is clear: The walls between Musk’s companies are coming down. Long-term holders are about to get paid in rocket fuel.

English

.@elonmusk, what if we took @SpaceX public by merging it with Pershing Square SPARC Holdings, Ltd. (SPARC) a new form of acquisition company that was approved by the @SECGov.

We could distribute SPARC special purpose acquisition rights (SPARs) to @Tesla shareholders so that all Tesla shareholders would have the right to invest in the SpaceX IPO, or they could choose to sell their SPARs to someone else.

This would reward loyal Tesla shareholders with the opportunity to invest in SpaceX (or with cash for their SPARs), while totally democratizing the IPO process.

In addition to receiving common stock in SpaceX, exercising SPAR holders would also receive Pershing Square SPARC Holdings II SPARs, which we could use to take @xai public at the time of your choosing.

Pershing Square would due diligence on behalf of all shareholders and would commit $4 billion of capital to the IPO at a fixed price per share.

SPARC has no underwriting fees, founder stock or shareholder warrants, and we would waive our right to receive SPARC sponsor warrants.

The result would be an IPO without any underwriting fees or dilutive securities issued. @SpaceX would go public with a 100% common stock capital structure and it would not incur any transaction costs other than modest legal fees which SPARC would pay from its cash on hand.

We could raise whatever amount of capital you would like by adjusting the exercise price of the SPARs. Assuming we issue 0.5 SPARs for each share of Tesla, there would be 1.723 billion SPARs outstanding including the 61.1 million SPARs that are already outstanding. Since one SPAR would be exercisable for two shares of SpaceX, the SPARs would be exercisable for 3.446 billion total SpaceX shares.

So, if we set the SPAR exercise price at $11.03, SpaceX would raise $42.0 billion, $38 billion from the exercise of SPARs and $4 billion from Pershing Square, or if we set the SPAR exercise price at $42.0, SpaceX would raise $148.7 billion, $144.7 billion from the SPAR exercise and $4 billion from us.

SPARC is indifferent to how much of the shares are primary versus secondary shares giving the company maximum flexibility.

We could do due diligence and enter into a definitive agreement committing to the transaction within 45 days, at which point it would be certain that SpaceX would go public at a fixed valuation subject only to SEC approval of the merger proxy/registration statement. Our commitment to the transaction would not be subject to market conditions.

We could start work right away and announce the transaction by mid- February.

It only seems appropriate that the most innovative and efficient rocket company in the world should go public in the most innovative, efficient, and fairest-to-Tesla-shareholders manner possible.

To Mars and beyond!

What do you say?

English

🌉

Banks are closed. The blockchain is open. Interactive Brokers just built the bridge.

While J.P. Morgan sleeps on weekends, $IBKR just solved the biggest friction in global capital markets: settlement speed. By allowing clients to fund accounts directly with $USDC, they aren’t just adding a “crypto feature.” They are effectively declaring that stablecoins are superior to SWIFT for moving money. This is the first major brokerage to treat crypto not as an asset to trade, but as a rail to run on.

THE 24/7 LIQUIDITY PIPE

Legacy finance is terrified of what $IBKR just did. They turned the $320B stablecoin market from a “casino chip” into immediate buying power for the S&P 500.

⚡ Zero Friction: You can now move liquidity from a Solana wallet to a stock portfolio in minutes, bypassing the T+2 settlement dinosaur.

🛑 The Weekend Gap: Banks lock your cash from Friday at 5 PM to Monday at 9 AM. The blockchain doesn’t. $IBKR clients can now position capital before the Monday open.

🌊 The Floodgates: Global investors in hyper-inflationary zones (Argentina, Turkey) hold savings in $USDT and $USDC. $IBKR just gave them a direct on-ramp to US Equities without touching a correspondent bank.

My Take 🎯

This is a structural shift in market plumbing. $IBKR is capturing the “unbanked” wealthy who live on-chain. By the time $SCHW and $HOOD figure this out, Interactive Brokers will have already absorbed the liquidity of the crypto-native economy. They are essentially becoming a DeFi protocol with a banking license. The spread between “crypto” and “finance” just collapsed to zero.

Bullish 🌉

English

🥇 Banks Raise 2026 $Gold Targets – Consensus Breaks Higher 🥇

The Setup:

Macro Overwhelms Mean Reversion

Gold is no longer speculation territory. Every major bank $Goldman, $BAC, Deutsche, $JPM has lifted 2026 targets to the $4,450–$5,200 range. This isn’t exuberance. This is structural. Central banks bought 760 tonnes in 2025 alone, up 2.5x the pre-2022 baseline. Emerging markets, led by China, remain vastly underallocated to gold. The Fed is cutting, the dollar faces gravity from fiscal deficits approaching 7% of GDP, and Western ETF inflows hit $33 billion in eight weeks.

💰 Why Banks Are Synchronized (And Why That Matters)

🔸 Central bank diversification from USD reserves into bullion 95% of central banks surveyed expect global holdings to rise

🔸 ETF demand structural: $14 billion flowed into gold ETFs in September alone, 880% higher year-over-year

🔸 Fed rate cuts by 100 basis points expected by mid-2026 non-yielding gold becomes relative value

🔸 Fiscal backdrop unchanged under Trump: deficit spending, tariffs, debt issuance all gold-supportive

🔸 $JPMorgan Private targets $5,200–$5,300, the outlier high end, signaling how far optimism extends

Where the Consensus Cracks

Not everyone agrees. $HSBC remains defensive at $3,950 assuming faster stabilization. Commerzbank caps upside at $4,100. Their case: tightening fiscal policy could emerge, Fed could stay hawkish if inflation re-accelerates, and equity markets could re-attract capital. Lease rates elevated. Physical supply squeezed. Manipulation risk exists. Real rates could turn positive again, crushing gold’s runway.

My Take 🎯

The macro case for gold is airtight: devaluation cycle, reserve diversification, monetary ease. But $5,000+ assumes no policy shock or equity capitulation doesn’t reverse the central bank bid. Consensus at $4,800–$5,000 reflects pricing power that needs to hold without the structural drivers fracturing. Watch Fed communications Q1 2026 a pivot kills momentum fast. The risk isn’t the target. It’s velocity and mean reversion when positioning peaks.

Bullish 🥇

English

היום נדבר על יסודות המינוף. בחיים האישיים, העסקיים, במסחר ובהשקעות.

מה זה מינוף, איפה אנחנו פוגשים אותו ביום-יום, יתרונות, חסרונות, דברים שחשוב לקחת בחשבון כשמשתמשים בו וטיפים קריטיים.

השיעור שכל אדם בעולם צריך ללמוד🧵💰

עברית

🏗️

BUFFETT’S BET ON THE “RENTERSHIP SOCIETY”

Everyone is watching the Fed pivot. Buffett is watching the demographic cliff. The market sees $LEN and $DHI as cyclical construction stocks. The Oracle sees them as the manufacturing arm of a new asset class: Institutional Housing.

THE SUPPLY SQUEEZE

The data is screaming divergence. Mortgage rates at ~6.5% didn’t destroy the need for shelter; they just destroyed the ability to buy it. This is where the Build-to-Rent (BTR) arbitrage begins.

🧱 The Pivot: Builders aren’t just selling to families anymore. They are selling entire zip codes to Private Equity.

📉 The Gap: We have a structural deficit of ~4M homes. That doesn’t vanish because money is expensive.

💰 The Moat: $LEN and $DHI have the capital to build when regional banks are paralyzed. They are capturing 100% of the supply growth.

🏦 The Vehicle: $XHB holds the builders, the suppliers, and the insurers. It’s the ETF for the “Shelter as a Service” economy.

My Take 🎯

Housing is no longer a cyclical trade; it is a yield trade. When you can’t buy, you rent. And when you rent a brand new single-family home, you are paying a premium to the only people capable of building it. Buffett didn’t buy “homebuilders.” He bought the future landlords of America. The American Dream is becoming a subscription model. Don’t fight the landlord.

English

🤖 $AMZN: AWS Goldilocks Inflection Point AI Capex Finally Printing Money 🤖

The Macro Setup: Rates Stabilizing, AI Spending Verified, Margin Thesis Intact

The fed funds futures market is pricing 2-3 more cuts through 2026, which means refinancing costs for Amazon's infrastructure binge are stabilizing. That matters enormously. $AMZN committed $125 billion in capex for 2025 most massive spend in tech but here's the pivot: AWS is now reaccelerating hard. Q3 2025 saw AWS grow 20% YoY, the fastest since 2022. That's not capex-driven noise. That's actual demand for AI infrastructure translating into revenue velocity.

The market had priced in two years of capex burnout. Wrong. Amazon is monetizing before capex peaks. Unlike $META's margin murder, $AMZN pulled off the rare feat spending $125B while expanding operating margins. Q4 guidance of $21-26B operating income actually beats expectations despite capex intensity.

AWS: Custom Chip Flywheel + Model Optionality = Durable Moat

🔹 Market share at 29% (down 2pts YoY but stabilized) while growing 18%+ YoY—competitors (Azure +39%, GCP +32%) grow faster but from much smaller bases

🔹 Trainium2 now fully subscribed, shipping in volume to Anthropic (Project Rainier: 500k chips). Trainium3 preview in late Q4, full volumes early 2026. This is margin-accretive custom silicon, not a capex sink.

🔹 Amazon Bedrock (generative AI applications) and AgentCore (agentic AI infrastructure) are the growth engines. Bedrock supports DeepSeek, Claude, GPT models maximum vendor optionality for enterprise customers.

🔹 Infrastructure backlog hit $200B at Q3 2025 end. October deals exceeded entire Q3 volume. Pipeline visibility is the highest we've seen in cloud.

The 2026 Bear Case (Acknowledged)

⚠️ 2026 capex will be even higher than $125B—likely $135-150B+ territory if guidance holds

⚠️ AWS margin compression from 39.5% (Q1) to 32-34% range as AI infrastructure monetization lags training costs

⚠️ AI monetization timelines remain uncertain; margin recovery depends on 2027-2028 payoff

⚠️ Valuation at ~32× P/E and $2.43T market cap means execution risk is priced in tightly

My Take: Macro Liquidity + Documented Demand = Margin Floor Holding

The inflection moment is now. Amazon caught the rare window where capex peaks while revenue velocity from AI infrastructure is demonstrable $200B backlog, 20% AWS growth, custom silicon ramping, enterprise deals validating spend. Unlike 2023-2024 when this was speculative, we now have hard bookings.

Margin compression is real but managed. Operating margin trajectory has moved from 2% pre-pandemic to 12%+ today. A dip to 10-11% in 2026 is digestible, not fatal. The company funds $125B capex from $130.7B operating cash flow—leverage is clean.

$META faces a cliff (no FCF proof of capex ROI). $MSFT faces hybrid complexity. $AMZN has the cleanest unit economics: AWS profit margins dwarf everything else; advertising (+24% YoY) and retail (+11%) are gravy. Even a 50bp margin dip on AWS leaves it as the highest-margin cloud business globally.

Risk: If capex growth accelerates beyond $150B without matching revenue velocity, the thesis breaks. Watch 2026 Q1 and Q2 AWS growth rates. Anything below 18% triggers repricing.

Patience beats conviction here.

Bullish 🤖

English