Sabitlenmiş Tweet

Francesco A. Fabozzi

27 posts

@FAFabozzi

Education & Research on LLMs and Quant Finance | Research Director @ Yale ICF | Managing Editor @ Journal of Financial Data Science | Data Science PhD

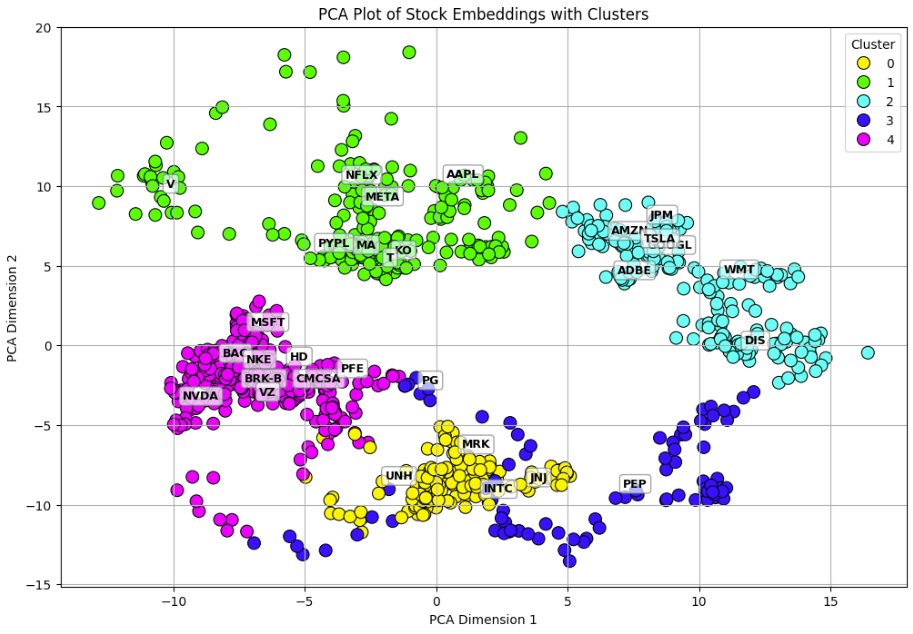

From my colleagues: “Can Machines Build Better Stock Portfolios?” aqr.com/Insights/Resea…