Finlo

816 posts

Finlo

@Finlo_com

Financial Leaning Platform for India. Duolingo Type Learning. try it at https://t.co/QbVRZysnSa

India Katılım Nisan 2026

8 Takip Edilen17 Takipçiler

@KommawarSwapnil A trap young earners fall into: assuming the office health cover has them sorted. It vanishes the day you switch or lose the job, usually right when you need it. Buying a small personal policy while young and healthy locks in a low premium for life.

English

One of the biggest underappreciated themes in India today is health insurance.

Healthcare costs continue to rise faster than most households expect. At the same time, insurance penetration remains relatively low and millions of families still rely on savings or borrowing during medical emergencies.

That gap is the opportunity.

India has made significant progress in expanding health insurance coverage, but compared to many developed markets, we are still in the early innings.

As incomes rise and awareness improves, more families are likely to view health insurance as an essential financial product rather than an optional expense.

This is why I keep an eye on companies that are already deeply embedded in this space.

Star Health, for example, is India’s largest standalone health insurer and has insured more than 19 crore lives since inception. In insurance, scale creates data, distribution advantages and customer trust that can compound over time.

What stands out even more is where the company is growing.

A large share of its business comes from Tier-2 and Tier-3 India. While investors often focus on metros, the next wave of insurance adoption could come from smaller cities where awareness is rising but penetration remains relatively low.

Of course, no investment story is without risks.

Claims inflation, competition and regulatory changes can all impact profitability. In insurance, premium growth alone isn’t enough. Underwriting discipline and claims management matter just as much.

But when you combine rising healthcare costs, an ageing population, increasing insurance awareness and deeper penetration into smaller towns, it’s not difficult to see why many investors remain optimistic about the long-term prospects of India’s health insurance sector.

The story may still be earlier than most people think.

#Investing #IndianMarkets #HealthInsurance #StarHealth

English

@hariniv2505 Solid wake up list, and the fix is gentler than it sounds. Pick one paycheck and automate a small SIP the day your salary lands, before you can spend it. Even ₹1000 a month builds the muscle. The 10 minutes of learning usually follows once you have skin in the game.

English

If you're in your 20's, have a job, and...

– You spend more on EMIs than investing in SIPs

– You think FD's are better than stocks coz your dad did it

- You are regularly spending money on depreciating assets

– You compare food coupons but won’t spend 10 mins learning compounding

Maybe it’s time to pause...

& learn how real wealth is built !

English

@Lettersfromappa The number that gets missed is that most of that 9% started with a tiny amount. You do not need a lump sum to enter the markets. A ₹500 monthly SIP into a broad index fund is a real start, and the habit matters more than the size in year one.

English

13 crore Indians have registered to invest in stocks.

Of those, 6.1 crore also hold mutual funds.

That is roughly 9% of our population in the capital markets.

For perspective:

→ United States - 62%

→ Canada - 47%

→ Australia - 37%

→ India - ~9%

We are early. India has a long way to go.

Two ways to ride the next decade with a SIP:

The safer bet - Nifty 50.

The risky bet - a capital markets ETF. Exchanges, depositories, brokers, AMCs. If more Indians join the markets, these companies grow before any of the stocks they trade.

English

@warrioraashuu Count me in. I am working on Finlo, where young Indians learn money the way they learn a language, one small lesson a day. We cover SIPs, tax, credit scores, insurance, and how to spot a scam before it gets you. tryfinlo.co

English

@sripatro_com Building Finlo, a finance learning app for India that works like Duolingo. Short daily lessons on SIPs, taxes, credit, insurance, and the scams hiding in between. Made for first-job earners figuring money out. tryfinlo.co

English

Hey founders 🙃

Looking to connect with people in:

🚀 SaaS

🤖 AI & Automation

📈 Tech

📱 Product Development

🔥 Web Apps

💻 Dev

🧠 Neurotech & Health Tech

What are you building now? Drop it below 👇 Curious to see what everyone's working on 🚀

English

The cost of raising a child in India can reach ₹6.75 crore, driven by school inflation. Start planning and investing early. Even small, consistent SIPs make a huge difference. tryfinlo.co

English

RBI flags risks, making this a 'stock picker's market'. For you, this means research matters more than ever. Don't blindly follow trends. Look for value in largecaps and specific sectors. More on this every week → tryfinlo.co

English

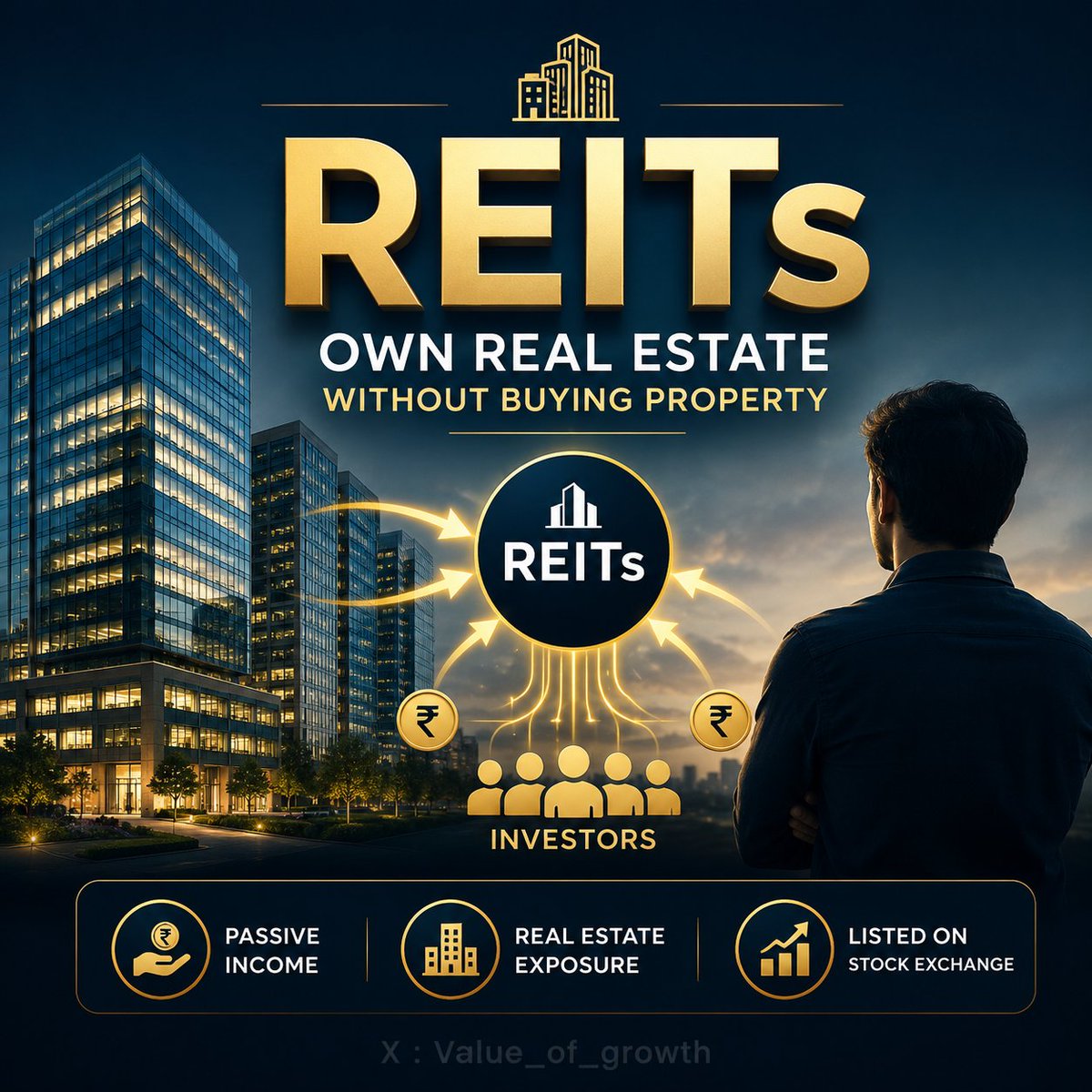

@Value_of_Growth Good primer. One thing beginners miss: a REIT is not the same as owning property. It trades on the exchange, so the price swings daily and reacts to interest rates. Treat it as a small income slice in your portfolio, not a replacement for equity or a home.

English

🏢 Most Indians know about:

✓ Fixed Deposits

✓ Gold

✓ Stocks

✓ Real Estate

But very few know about REITs.

What if we told you...

You can invest in premium commercial real estate directly from your Demat account?

Welcome to the world of REITs 👇

1️⃣ What is a REIT?

REIT stands for Real Estate Investment Trust.

Think of it as a company that owns income-generating commercial properties such as office buildings, business parks and commercial real estate.

2️⃣ Why were REITs created?

Not everyone can buy a commercial property worth crores.

REITs allow small investors to participate in large real estate assets.

3️⃣ How does a REIT make money?

Simple.

Companies pay rent.

REIT collects rent.

A portion of that income is distributed to investors.

4️⃣ How do investors make money?

There are two ways:

💰 Regular Distributions

📈 Capital Appreciation

5️⃣ Is it like buying a stock?

Partly yes.

You can buy and sell REITs through your Demat account just like stocks.

But the underlying asset is real estate.

6️⃣ How much money do I need?

You don't need lakhs or crores.

In many cases, investors can start with just a few thousand rupees, making REITs far more accessible than buying a property.

7️⃣ Can I buy REITs through Zerodha, Groww, Dhan etc.?

Yes.

REITs are listed on stock exchanges and can be purchased just like shares.

8️⃣ Which REITs are listed in India?

🏢 Embassy REIT

🏢 Mindspace REIT

🏢 Brookfield REIT

9️⃣ Why do investors like REITs?

✅ Passive Income

✅ Real Estate Exposure

✅ No Tenant Issues

✅ No Maintenance Headaches

✅ Easy Liquidity

🔟 What are the major risks?

⚠️ Occupancy may decline

⚠️ Rental growth may slow

⚠️ Interest rates can impact valuations

⚠️ REIT prices can fall

Interesting?

In Part 2, we'll cover:

✓ SIP vs Lumpsum

✓ Best Time To Invest

✓ Taxation

✓ Market Crash Impact

✓ REIT Index

✓ How To Analyse REITs

and other frequently asked questions.

Have you ever invested in a REIT? 🤔

#REIT #Investing #PersonalFinance #PassiveIncome #StockMarket

English

@TheTradingwolf0 Worth adding for anyone new to this: simpler tax does not mean you can skip saving. The old regime nudged people to invest just to cut tax. Once that nudge is gone, the discipline has to come from you. Run both regimes on a calculator before locking money into any product.

English

🚨 BIG TAX CHANGE COMING IN INDIA FROM APRIL 1, 2026

The government is replacing the 64-year-old Income Tax Act, 1961 with a new Income Tax Act, 2025.

Here's what it means for you:

✅ Taxable income up to ₹12 lakh = ZERO tax (under the new regime with rebate)

✅ Simpler tax laws and compliance

✅ Wider tax slabs and lower rates

✅ Less paperwork and fewer disputes

✅ Faster and easier ITR filing

❌ Traditional deductions like 80C may become less relevant

❌ Tax-saving investments may no longer be the main way to reduce taxes

Who benefits the most?

• Salaried employees 👨💼 • Middle-class families 🏠 • Senior citizens 👴 • Small business owners 📊 • Professionals & freelancers 💻

The biggest shift?

India is moving from a "save tax through deductions" system to a "pay lower tax by default" system.

This could be the largest simplification of India's tax framework in decades.

If implemented as proposed, millions of taxpayers may never need complex tax planning again.

Agree or disagree? 🤔

#IncomeTax #PersonalFinance

English

@anshumanomics The hardest line on that list is don't touch it. The first 30 percent drop makes every instinct scream to stop. The fix: auto debit on salary day and delete the tracking app. Boring and automatic usually beats clever and emotional.

English

so what do you actually do?

• open a direct mutual fund account (zerodha coin, groww)

• pick 1 simple nifty 50 index fund

• set ₹10k SIP on salary day

• don’t touch it

• repeat for 20 years

that’s it

no tips. no timing the market. no expertise needed.

English

₹10,000/month at 22

sounds small right?

let me show you what it actually becomes

and why you’ll want to cry after reading this

English

@ardent__dev Mine is Finlo, a web app teaching young Indians personal finance in 60 second lessons. Think SIPs, taxes, credit scores, and spotting scams, learned a little each day instead of one boring crash course. Free to start at tryfinlo.co. Would love a look and any feedback.

English

I want to see what indie SaaS founders are building.

Drop your startup and link below 👇

English

@sureshbabudj Finlo. A money learning app for India that turns SIPs, taxes, credit, and insurance into quick daily lessons, plus the scam awareness most courses skip. Solo built, web first, free to try at tryfinlo.co. Cheering on everyone shipping outside big tech.

English

Indie devs,

What are you building right now?

Show me your app, your repo, your prototype, your chaos.

I want to see the cool stuff happening outside big tech.

English

The biggest roadblock for beginners is thinking term cover is only for married people with kids. If anyone depends on your income, or you carry an education or home loan, you need it now. Premiums are cheapest in your 20s and lock in for life, so buying early is the actual hack here.

English

Buying a ₹1 Crore Term Insurance plan blindly? You might be leaving your family completely exposed. 🚨🧵

Most people treat Term Insurance like a random checklist item: "Premium cheaper is better, let's buy a random cover." But a single mistake can turn your financial safety net into a nightmare during a claim.

Here is a quick, no-nonsense checklist you MUST check before signing the dotted line: 👇

1️⃣ The HLV Cap (Stop guessing your Sum Assured)

You can't just buy any cover you want. Insurers calculate your Human Life Value (HLV).

A standard thumb rule is 20x to 25x of your annual income.

If your annual income is ₹10 Lakhs, aim for a ₹2.5 Crore cover. Don't let agents under-insure you with a basic ₹50 Lakh policy just to show a lower premium! 📉

2️⃣ Claim Settlement Ratio (CSR) vs. Claim Amount Settlement Ratio

Don't just look at CSR (number of claims settled). Look at the Amount Settlement Ratio (the actual value of total money paid out).

Look for insurers with a CSR consistently above 98% over the last 3-5 years. Brand reputation and corporate governance matter when it's D-day for your family. 🏛️

3️⃣ The "Moratorium Period" is NOT a License to Lie 🛑

Under IRDAI rules, after 3 years (for term plans), an insurer generally cannot reject a claim.

BUT HERE IS THE CATCH: If the insurer proves willful fraud or deliberate hiding of chronic pre-existing diseases (like diabetes, heart conditions, or cancer) to get the policy, they can take it to court, cancel the policy, and forfeit your premiums.

Declare every medical checkup, smoking habit, and family history honestly. A rejection at the proposal stage is 100x better than a claim rejection for your grieving family. 📑

4️⃣ Skip the "Return of Premium" (TROP) Trap 🪤

Agents love selling "Term with Return of Premium" because you get your money back if you survive.

The Reality: These plans charge a significantly higher premium.

Better Strategy: Buy a regular, pure term plan. Take the money you saved on the premium difference and put it into a low-cost Index Fund or Public Provident Fund (PPF). You will end up with a much larger corpus! 💰🚀

5️⃣ Choose Policy Term Wisely (Don't insure till 85!)

You only need a term plan until your active working age and until your major liabilities (home loans, children's education) are cleared.

Taking a cover up to age 60 or 65 is usually optimal. Extending it to age 80 or 85 just inflates your premium unnecessarily for years when you no longer have active income to replace. ⏳

Bottom Line: Pure term insurance is the cheapest and most powerful financial gift you can give your family. Buy it early when you are young and healthy to lock in dirt-cheap premiums.

What is the biggest roadblock holding you back from buying a pure term insurance policy today? Share your doubts below! 👇

#PersonalFinanceIndia #TermInsurance #FinancialLiteracy #MoneyTips #InsuranceAdvice #TermPlan #FinancialPlanning #IRDAI

English

@Rojash020 Where you park it matters as much as the size. A normal savings account is too easy to raid during a sale. Keep it in a separate liquid fund or a no-card account, reachable in a day but not tempting. If monthly costs are 20k, aim for 60k to 1.2L.

English

The real gift here is time, not the amount. Compounding is a snowball: the early years look tiny and boring, then the final stretch does the heavy lifting. A small SIP from a newborn has almost two decades to roll before college fees arrive. Starting now always beats a bigger SIP started later.

English

Successfully registered a Minor Mutual Fund SIP for a 1-month-old baby. 👶📈

Most people wait for the “right time” to invest.

But when it comes to a child’s future, the best time is NOW.

I strongly believe that education is the biggest investment of life. 🎓

A small SIP started today can potentially create a meaningful corpus for higher education years later.

Start early. Stay consistent. Let compounding do the heavy lifting.

Because the future is built by the decisions we make now, not later.

#SIP #ChildEducation #InvestEarly #Compounding #MutualFunds #LongTermInvesting #AamInvestor #aaminvestor

⸻

Join Us for Lifetime FREE Mutual Fund Investment Guidance 🚀

AMFI Registered Mutual Fund Distributor

Registered Name :- Khushnuma Parween

Registration No :- ARN-236680

👉 Invest Now: aaminvestor.themfbox.com/signup

📲 WhatsApp: wa.me/919608999911

🌐 Visit: aaminvestor.in

Aam Investor के साथ Mutual Fund इन्वेस्टमेंट सही है

#MutualFundsSahiHai

#MutualFunds #SIP #WealthCreation #LongTermInvesting #aaminvestor

English