@PhilMickelson Hope everything is ok. Praying for you and your family.

Hope to see you at Shinnecock this summer and grab the Grand Slam!

English

Gavbear90

13.9K posts

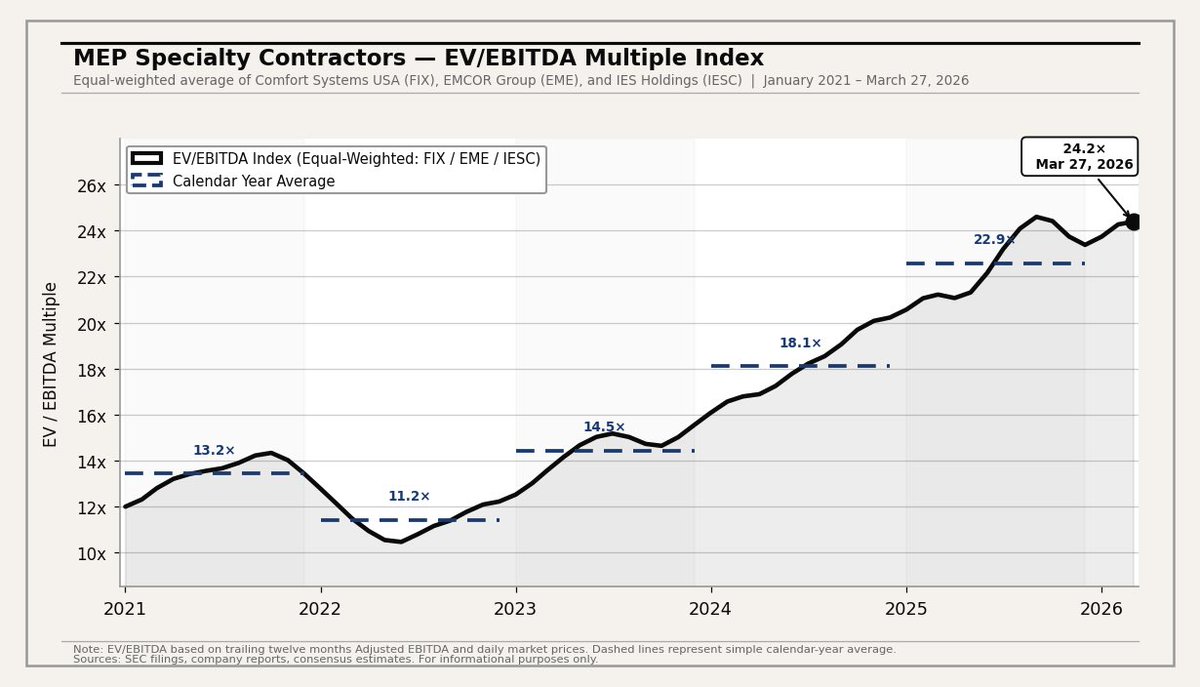

Private Equity-backed HVAC platform American Residential Services (ARS) is exploring a sale $3.5 billion expected EV, per Reuters ~17.5x 2026E EBITDA of $200 million ~20.0x 2025 EBITDA of $175 million Here’s why ARS might not get $3.5B: ARS started fireside chats so they’re early in the sale process ~$175 million Adj. EBITDA in 2025 and now mgmt is estimating $200 million for 2026E, or ~14%+ y/y growth That’s a lot, particularly if it’s all organic growth ARS would need a number of deals under LOI and try to get full credit for the pro forma adjusted EBITDA And ARS effectively stopped M&A two years ago, so it’s unlikely Second, ARS trading at a similar multiple as Sila (17x) Redwood (17x) and now Champions (18.5x) could be a stretch given their “big box” exposure Home Depot & Lowe’s are great for volume but its lower margin work and introduces concentration risks That’s another headwind to value Finally, estimated $1.5 billion 2026 revenue would only represent ~3.2% CAGR in top line revenue since 2022 ~13% EBITDA margins on a platform growing ~3% a year is not exactly a super compelling story Here’s an expected valuation range: $2.7B (15.5x @ $175M EBITDA) - Bear Case $3.4B (17x @ $200M EBITDA) - Bull Case

At least 4 more private equity-backed residential HVAC platforms will trade this year >$20 million EBITDA platforms Bookmark it

@realsashastone Love Megyn Kelly. Think Ben Shapiro is Israel first, not America first. Candace Owens is a grifter and a mean girl.