Late Stage Capitalism retweetledi

Late Stage Capitalism

61.1K posts

@GlobalCollapse

Physician. 30yr investor. Jan 2026 Top 5: 1. IREN/IRE 2. APP/APPX 3. DGXX 4. DMGGF/DMGI 5. ZMDTF Honorable Mention: CIFR, BITF, TSM Longshots: MIGI TGEN

$20.7 million into these $IREN calls

Opened a new long position in $VIVO today. This one took some digging. Let me walk you through the full picture. I originally was going to wait to put this post out but seems like the market just now found this gem this week as it’s up 50%. $78 million market cap. And I think this is just the beginning. On April 21 VivoPower closed a $41 million acquisition of an operational 41.5MW data center in Mo i Rana Norway. Powered by 100% renewable hydroelectric energy at below $0.035 per kilowatt hour. One of the cheapest power costs for data centers anywhere in Europe. Zero equity raised. Zero dilution. Paid at a disciplined 4x EBITDA multiple. The company flipped from EBITDA negative to EBITDA positive in a single transaction. $31 million in annualized revenue and $10 million in EBITDA. Not projected. Operational today. And then six days after closing they announced something most people missed. The facility prequalified 30MW into Statnett’s ancillary services markets. The Nordic grid pays data centers to hold flexible load capacity in reserve. $1.9 million in additional annualized EBITDA. Zero incremental capex. Pure margin on top of existing operations. Three independent revenue streams from the same single asset. AI tenant lease in active tender with strong hyperscaler inbound interest. Grid demand response already paying. Waste heat district heating in feasibility. One facility. Three revenue lines. None cannibalizing each other. Now here is what sits behind it. Norway has a pending 40MW expansion. If it clears the site goes from 41.5MW to over 80MW. When a hyperscaler signs a long term AI compute lease the revenue per watt jumps 3 to 5x over standard hosting rates. That single facility at full capacity could generate $150 to $200 million in annual revenue. Behind Norway: 291MW of secured powered land in Finland. A 25MW sovereign AI data center platform already in place in the UAE. Power-secured land in constrained markets that hyperscalers cannot easily replicate. Tembo EV spin on deck at a targeted $838 million valuation. Nasdaq already approved the ticker TEMB. When that closes it strips $8 million in annual overhead from a company generating $10 million in EBITDA. Here is what the market is almost entirely missing. Management published a formal 10 year strategic growth plan with specific targets. By 2029: 2GW of controlled power sites. $1 billion in annual revenues. $200 million in operating free cash flow. By 2033: 10GW of power sites. $3 billion in annual revenues. $1 billion in operating free cash flow. By 2036: 20GW spanning EU, GCC, ASEAN, and Africa. $5 billion plus in annual revenues. A $78 million company with management formally targeting $1 billion in revenue by 2029 on assets they are already controlling today. Board bought 2.65 million shares personally. Terminated the $180M dilution shelf. Former Microsoft Global AI leader on the advisory council. GCC sovereign family offices backing the financing. The risks are real. Management has a history of big promises. The hyperscaler lease is not signed yet. The float is tiny. But $78 million market cap. $31 million in current revenue. Three revenue streams from one facility. $838 million spin on deck. Management targeting $1 billion by 2029. The asymmetry here is one of the more interesting setups I have seen in the small cap space in a long time. Long $VIVO. Not financial advice. DYOR. $VIVO

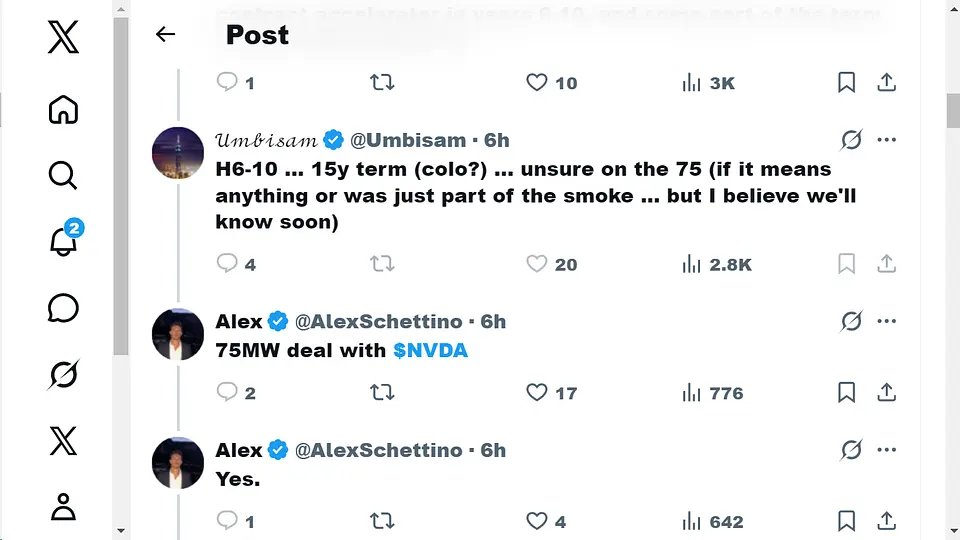

$IREN 🤔

This is what local accountability looks like: In Festus, Missouri, a town of about 14,000 people, the city council quietly approved a $6 billion Ai data center to be built on 360 acres just north of Highway 67. Residents say they were never properly heard. Meetings were held in private. Documents were released too late. A week after the approval, the town held a regular election. Voter turnout jumped 129 percent. Every single council member who had voted yes lost in a landslide. A 70-year-old first-time candidate beat an 8-year incumbent by 40 percentage points. Now a recall petition is circulating to remove the mayor as well. The lawsuit against the city is already filed. Has your local government ever been held accountable like this? 🔥

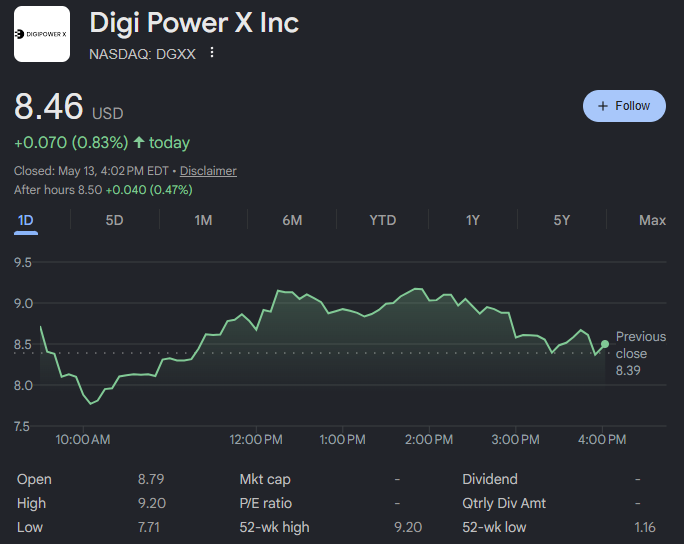

$KEEL Ben is one of the smartest ceos around. He actually puts in the work unlike Jason Les and Fred Thiel who steal shareholder money and do nothing. Ben said location is most important factor for these tenets. No doubt they will sign 3 leases that are A+++ this year. He confirmed what he has been saying all along with the cooler temperatures and closer to huge hubs in the NE and W coast with fiber optic cables. The leases signed in Texas are for AI training models and not actually using the AI applications. He also said the demand was so high at Mose Lake they didn't even need to offer gpus as a service, which now confirms to me that they should be able to beat DGXX $230 kw per month deal. That's exactly why they threw out buying their own chips. The demand is so high that they didn't need to do what Iren did. Think about that. Like if you AGREE. Finally,you can follow me,I'll be updating you with the latest info on KEEL and more related content.

$IREN has so much grid-secured power its insane. $HUT $WULF $GLXY $CIFR $KEEL dont even come close Imagine $2.5M-$3M per MW on 5000MW, because its already grid secured they can start colocation even for sites sitting out years away today. $IREN could collect between $12.5B-$15B in Revenue per year. Imagine that on 10-15 Year leases. What’s crazy is that they have even more undisclosed power and sites. Electrons are expensive and not easy to come by. They can pull a $SNDK and contract all the capacity in 2 years. The reality is that $IREN emerging themselves in the AI Cloud world and I believe they can successfully do it. But the issues is that they are slowed down by GPU delays and bottlenecks. It’s also allot more capital intensive. For the company I think AI Cloud is great but for my stock I think colocation is great. At these prices though I think most other colocation players are running out of secured power and Iren still doing AI cloud might give the better return from these levels.