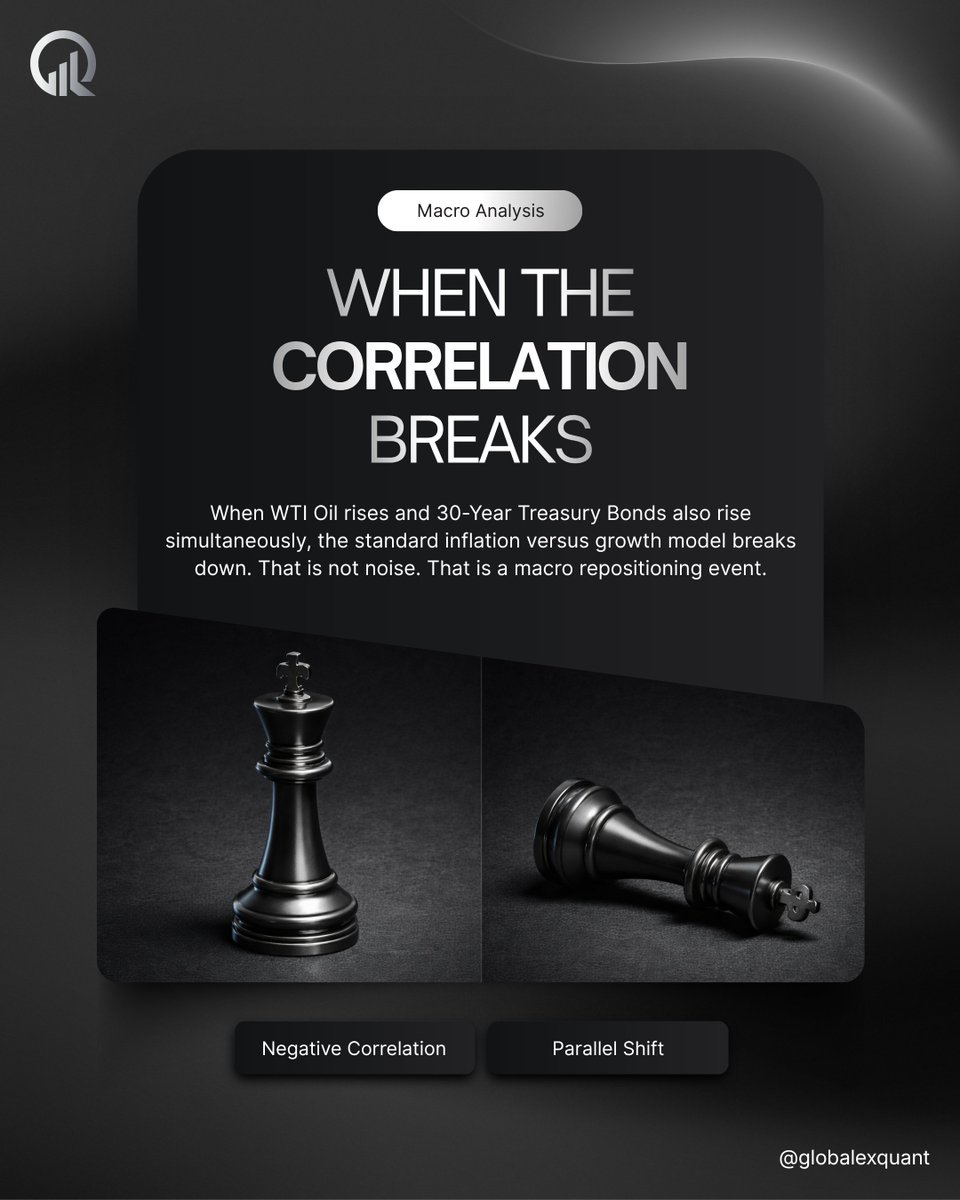

The oil-bond negative correlation is one of the most reliable macro relationships in institutional analysis. Until it is not.

Here is what happens when the correlation breaks, and what the correct response looks like.

OIL UP. BONDS DOWN.

The standard negative correlation runs on yield mathematics. Rising oil signals rising inflation expectations. A fixed bond yield becomes less attractive in real terms when inflation moves against it. Institutional participants sell the back end of the bond market before the move becomes visible on an equity chart. This is the baseline relationship that macro frameworks are built around.

THE PARALLEL SHIFT.

When WTI and 30-Year Treasury Bonds both rise simultaneously, that baseline breaks. Both sides of the negative correlation are moving in the same direction, which means the inflation versus growth model is no longer the dominant force in the market at that moment. Something larger is overriding it.

MACRO REPOSITIONING.

A parallel shift signals institutional repositioning across multiple asset classes at the same time. The inflation versus growth model has not permanently broken. It has been temporarily overridden by a force large enough to move both correlated markets in the same direction. The key distinction is that this is not noise or random divergence. It is a structural event with implications beyond the two markets directly involved.

PAUSE. REASSESS. THEN ACT.

Continuing to apply the standard oil-bond directional framework during a parallel shift means executing against a temporarily broken model. The correct institutional response is not to find an alternative trade within the same framework. It is to step back entirely, reassess the macro narrative from the top, and wait until the standard relationship reasserts itself before any new position is executed.

Which market do you read first? Drop it in the comments.

:shield: Educational content only. Not financial advice.

#globalexquant #macrotrading #intermarketanalysis #institutionaltrading #tradereducation

English