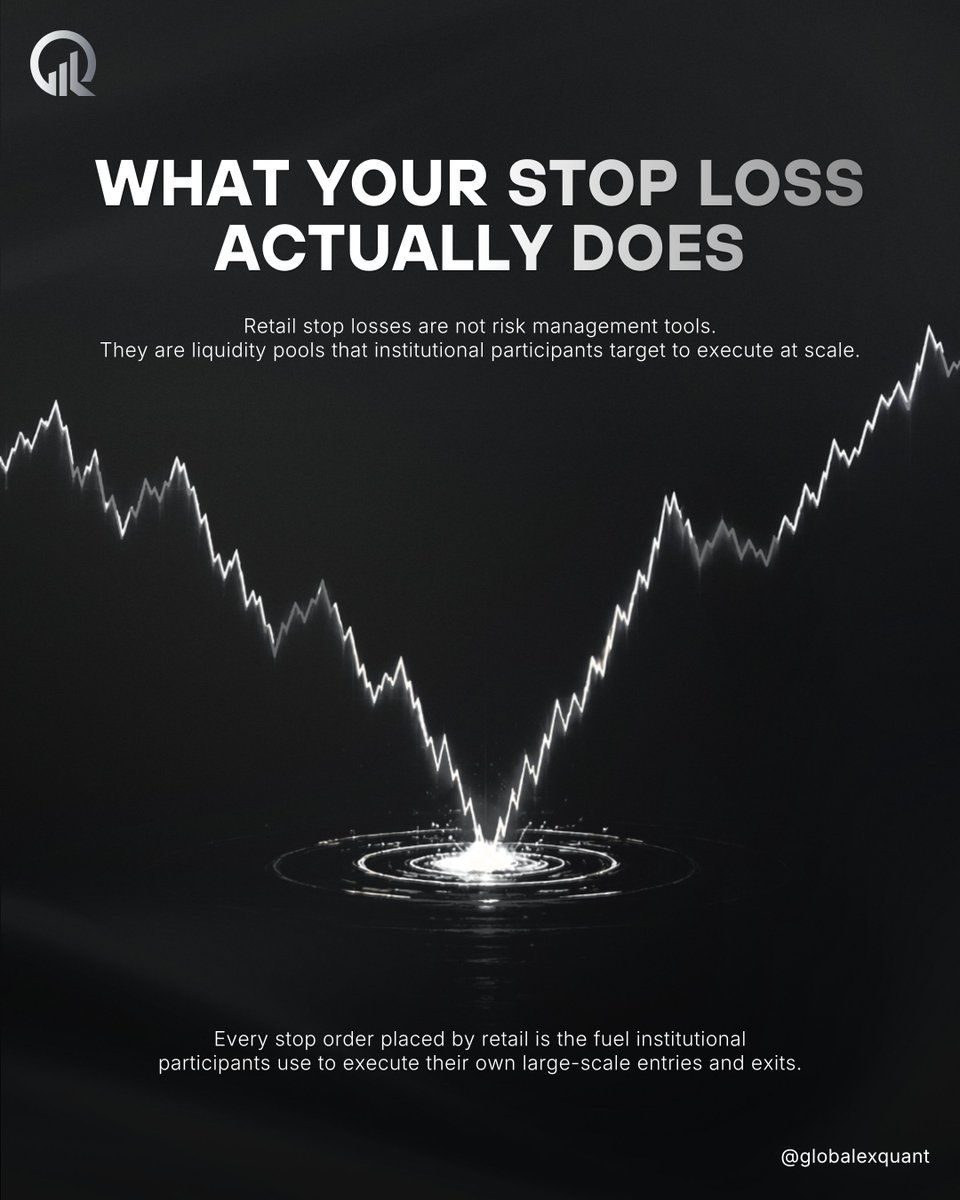

A stop loss placed just below a key level is not hidden. It is predictable.

And predictable order flow is what institutional participants need most.

The reason retail stop clusters are useful to institutional participants has nothing to do with targeting individual traders. It is a scale problem.

Executing a large block order in size requires a significant pool of counterparty liquidity at the same price level. Retail stop orders, concentrated at obvious structural points like session lows, day highs, or round numbers, provide that pool in a predictable location at a predictable moment.

The more universally recognised a level is as support or resistance, the more stop orders accumulate just beyond it, and the more attractive it becomes as a price discovery target. Price discovery in this context is not random volatility.

It is market makers testing whether genuine institutional limit orders are resting at that level by using the retail stop cluster as the fuel to reach it.

Understanding this does not mean removing stop losses. It means placing them at levels that are structurally justified rather than obvious, and sizing positions so that a sweep of a predictable level does not force an exit before the trade thesis has had time to develop.

🛡️Educational content only. Not financial advice.

#globalexquant #orderflow #marketstructure #institutionaltrading #tradereducation

English