Sabitlenmiş Tweet

GrumpyFreud 🔮

2K posts

@GrumpyFreud

Communty Lead at @openservai

SERV’s Vision and Plan for Banking In this post we're going to lay out our plans for the banking industry in 2026. Our goal is to bring SERV reasoning into the world’s largest global enterprise markets and establish it as the new industry standard. The strong interest we’ve already received from enterprise is a clear testament to the significant demand for this technology, with banking and finance emerging as one of the most active sectors of interest. The opportunity in this market for SERV is enormous: - Financial institutions are projected to spend $97 billion on AI by 2027, growing at a 29% CAGR, exceeding $200 billion annually by 2030. - McKinsey est. the annual value of AI in banking at $200–340 billion. - Citi projects that AI will add $170 billion in global banking profits by 2028, helping push sector profits toward $2 trillion. This is the trillion-dollar opportunity we are targeting. Why financial institutions are turning to SERV: In banking, where trillions of dollars are at stake, the top three roadblocks preventing widespread AI agent adoption are trust, reliability, and cost-effectiveness. This is exactly why leading financial institutions are turning to SERV. Our technology, built in close collaboration with our enterprise partners, allows financial institutions to accelerate their AI adoption while ensuring it happens in a secure, reliable, and commercially viable way, delivering breakthrough performance without compromising on risk, control, or regulatory compliance. ——- What a bank actually requires to implement agents Every automated system that touches a regulated decision passes through model risk management - SR 11-7 in the US, SS1/23 in the UK - and in most cases, a named bank executive is personally accountable for every AI-driven outcome. That machinery is what we are currently preparing our engine for, fitting all markets SERV is targeting including the US, UK / EUR, Africa, and Singapore. Just a brief look through current compliance ecosystem gives us a good understanding of where things are going: - last April, US regulators revised their model risk guidance (SR 26-2) and explicitly placed generative and agentic AI outside its formal scope. The assurance playbook for agents now has to be built, not inherited from official policies. - this month, the FCA published the Mills Review, laying the foundations for agentic finance in the UK: autonomous agents are coming to retail banking, the regulator will supervise them with its own AI, but accountability stays with named humans. - the EU AI Act classifies creditworthiness assessment as high-risk. After the Digital Omnibus, those obligations land on 2 December 2027 - a fixed deadline banks are being told to spend on governance work. - Singapore's MAS is finalizing AI Risk Management Guidelines that explicitly cover AI agents: full AI inventories, risk materiality assessments, lifecycle controls - and no shifting of accountability to vendors. Four jurisdictions, with one convergent demand: reliability, explainability, auditability, bounded autonomy. None of it can be satisfied by a smarter model. These are precise architecture requirements that our system is ready to meet. The industry's own numbers describe the gap precisely. 99% of companies plan to put agents into production; 11% have (KPMG). 57% of banking executives expect agents fully embedded in risk, compliance, audit and fraud functions within three years (Accenture). ——- How SERV clears the bar Validation: SERV Reasoning Graph Sharding decomposes every agent decision into bounded, schema-forced steps - deterministic code where it can be, model calls only where it must be. A model-risk team reviews a reasoning graph, not a prompt, and the same input produces the same reasoning trace - the property that validation, revalidation, and challenger testing actually require. Auditability: SERV Audit allows insight into decision chains as first-class artifacts: inputs, rules applied, intermediate conclusions, confidence, approvals - exportable as evidence packs shaped for model-risk validation files and AI governance review, and explainable to a supervisor or a customer. Reliability: Shadow Agents and Verification Hints validate every draft at runtime against the brief, policy and constraints before anything ships, and gate irreversible actions behind explicit checks and human checkpoints. Multipath Reasoning lets contradictory rulebooks - credit policy, risk appetite, regulatory constraint - coexist in one reasoning graph, because that is what real banking decisions look like. Security: PromptGuard screens every request inbound for injection before the model runs, and every output outbound for leakage before release. Prompts and data are never stored or trained on, and private, encrypted inference (TEE plus end-to-end encryption) is built for regulated data and residency requirements. Economics: Verification only matters if it pays for itself. Bounded Reasoning Graphs are authored once and amortized across millions of runs, so smaller models execute them reliably - frontier-grade results without frontier-grade unit costs. ——- SERV Roadmap for the Banking Industry H2 2026: - First PoCs / pilots signed with banks and financial institutions - Banking benchmark program opens - Legal entities live across US, Europe, Singapore, Africa - Banking-grade hires: model risk (SR 11-7/SS1/23) - Certifications secured (SOC 2 / ISO 27001) - Neobank integrations - Major DeFi protocol integrations - Fintech pilots converting to paid production 2027: - First Tier 1 bank in production - Agents touching payments under SERV verification - Agentic commerce verification layer ——- Why the window is now Agent-executed payments went live across 30+ card issuers just this month. Regulators on three continents have published their assurance bars. And yet, up to 40% of enterprise agent projects are still expected to be cancelled by 2027 on cost and risk controls. The institutions that win the agent era will be the ones whose agents can be validated, audited, and trusted with real money. One bank becomes the reference, the next ten follow. SERV layer is already running in government production. Banking is next.

SERV’s Vision and Plan for Banking In this post we're going to lay out our plans for the banking industry in 2026. Our goal is to bring SERV reasoning into the world’s largest global enterprise markets and establish it as the new industry standard. The strong interest we’ve already received from enterprise is a clear testament to the significant demand for this technology, with banking and finance emerging as one of the most active sectors of interest. The opportunity in this market for SERV is enormous: - Financial institutions are projected to spend $97 billion on AI by 2027, growing at a 29% CAGR, exceeding $200 billion annually by 2030. - McKinsey est. the annual value of AI in banking at $200–340 billion. - Citi projects that AI will add $170 billion in global banking profits by 2028, helping push sector profits toward $2 trillion. This is the trillion-dollar opportunity we are targeting. Why financial institutions are turning to SERV: In banking, where trillions of dollars are at stake, the top three roadblocks preventing widespread AI agent adoption are trust, reliability, and cost-effectiveness. This is exactly why leading financial institutions are turning to SERV. Our technology, built in close collaboration with our enterprise partners, allows financial institutions to accelerate their AI adoption while ensuring it happens in a secure, reliable, and commercially viable way, delivering breakthrough performance without compromising on risk, control, or regulatory compliance. ——- What a bank actually requires to implement agents Every automated system that touches a regulated decision passes through model risk management - SR 11-7 in the US, SS1/23 in the UK - and in most cases, a named bank executive is personally accountable for every AI-driven outcome. That machinery is what we are currently preparing our engine for, fitting all markets SERV is targeting including the US, UK / EUR, Africa, and Singapore. Just a brief look through current compliance ecosystem gives us a good understanding of where things are going: - last April, US regulators revised their model risk guidance (SR 26-2) and explicitly placed generative and agentic AI outside its formal scope. The assurance playbook for agents now has to be built, not inherited from official policies. - this month, the FCA published the Mills Review, laying the foundations for agentic finance in the UK: autonomous agents are coming to retail banking, the regulator will supervise them with its own AI, but accountability stays with named humans. - the EU AI Act classifies creditworthiness assessment as high-risk. After the Digital Omnibus, those obligations land on 2 December 2027 - a fixed deadline banks are being told to spend on governance work. - Singapore's MAS is finalizing AI Risk Management Guidelines that explicitly cover AI agents: full AI inventories, risk materiality assessments, lifecycle controls - and no shifting of accountability to vendors. Four jurisdictions, with one convergent demand: reliability, explainability, auditability, bounded autonomy. None of it can be satisfied by a smarter model. These are precise architecture requirements that our system is ready to meet. The industry's own numbers describe the gap precisely. 99% of companies plan to put agents into production; 11% have (KPMG). 57% of banking executives expect agents fully embedded in risk, compliance, audit and fraud functions within three years (Accenture). ——- How SERV clears the bar Validation: SERV Reasoning Graph Sharding decomposes every agent decision into bounded, schema-forced steps - deterministic code where it can be, model calls only where it must be. A model-risk team reviews a reasoning graph, not a prompt, and the same input produces the same reasoning trace - the property that validation, revalidation, and challenger testing actually require. Auditability: SERV Audit allows insight into decision chains as first-class artifacts: inputs, rules applied, intermediate conclusions, confidence, approvals - exportable as evidence packs shaped for model-risk validation files and AI governance review, and explainable to a supervisor or a customer. Reliability: Shadow Agents and Verification Hints validate every draft at runtime against the brief, policy and constraints before anything ships, and gate irreversible actions behind explicit checks and human checkpoints. Multipath Reasoning lets contradictory rulebooks - credit policy, risk appetite, regulatory constraint - coexist in one reasoning graph, because that is what real banking decisions look like. Security: PromptGuard screens every request inbound for injection before the model runs, and every output outbound for leakage before release. Prompts and data are never stored or trained on, and private, encrypted inference (TEE plus end-to-end encryption) is built for regulated data and residency requirements. Economics: Verification only matters if it pays for itself. Bounded Reasoning Graphs are authored once and amortized across millions of runs, so smaller models execute them reliably - frontier-grade results without frontier-grade unit costs. ——- SERV Roadmap for the Banking Industry H2 2026: - First PoCs / pilots signed with banks and financial institutions - Banking benchmark program opens - Legal entities live across US, Europe, Singapore, Africa - Banking-grade hires: model risk (SR 11-7/SS1/23) - Certifications secured (SOC 2 / ISO 27001) - Neobank integrations - Major DeFi protocol integrations - Fintech pilots converting to paid production 2027: - First Tier 1 bank in production - Agents touching payments under SERV verification - Agentic commerce verification layer ——- Why the window is now Agent-executed payments went live across 30+ card issuers just this month. Regulators on three continents have published their assurance bars. And yet, up to 40% of enterprise agent projects are still expected to be cancelled by 2027 on cost and risk controls. The institutions that win the agent era will be the ones whose agents can be validated, audited, and trusted with real money. One bank becomes the reference, the next ten follow. SERV layer is already running in government production. Banking is next.

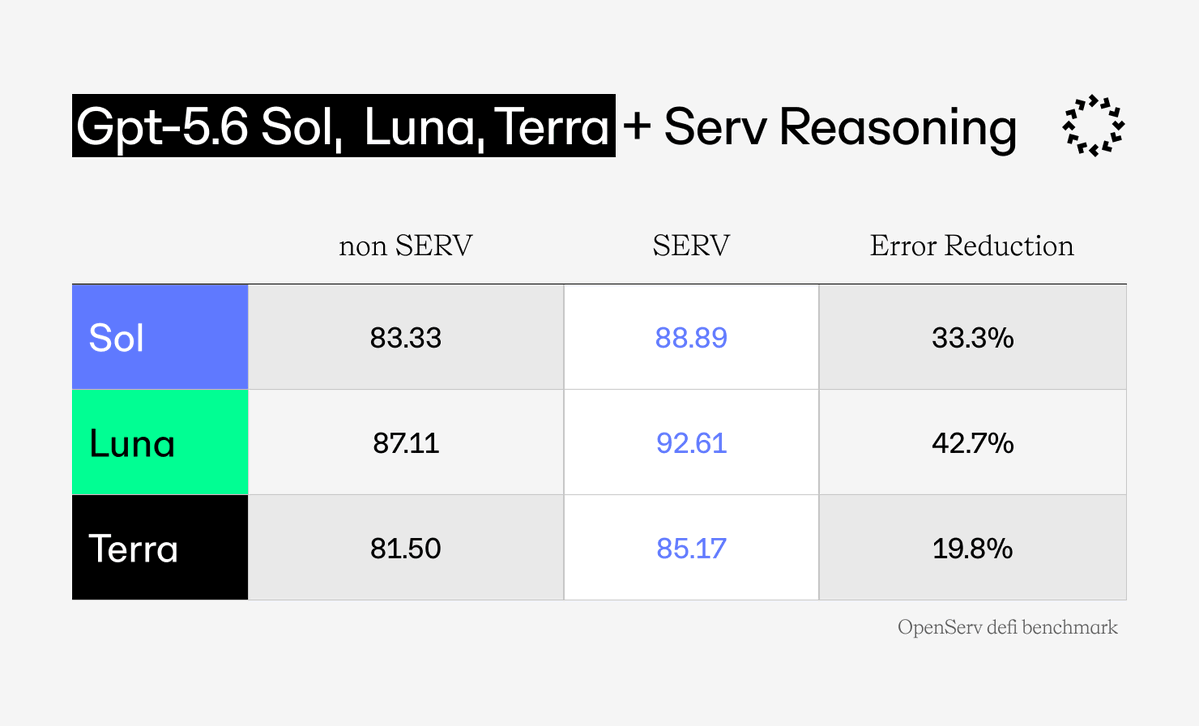

OpenAI's new GPT-5.6 $1 model (Luna) just beat the $5 flagship (Sol) on our agentic benchmark. With SERV Reasoning, all three models performed better, while Luna outscored every configuration tested. Thanks to SERV, failure rates dropped by up to 42.7%.* That's the thesis SERV is built on: Reliability in AI is the real product. Large-scale AI adoption is waiting on the layer that makes AI dependable enough for production. Standout findings: - Luna + SERV tops the table at 1/5 of Sol's price. - These tiers behave less like mini/nano distillations and more like independent takes on one architecture with distinct post-training. - Luna behaves like a smaller model RL-trained hard for agentic instruction-following and steerability, which would explain why it takes the biggest lift from SERV. *i.e. the relative drop in failure rate: Luna went from 12.89% failed tasks to 7.39%. More results and insights coming soon.

SERV Reasoning v2.0 Release Launching mid-July, SERV v2 is the most significant upgrade we've ever done to the SERV Reasoning engine. Our goal remains the same: SERV becomes the foundational AI agent infrastructure that enterprises, global financial institutions, governments, and humanoid robotics companies use to run AI agents at scale. We believe the lack of enterprise trust in AI agent reasoning is the #1 barrier holding back the mass adoption of AI agents in high-stakes industries like banking, robotics, and government workloads. That's why the enhancements in SERV v2 focus on making AI agents more trustworthy, reliable, and more cost-efficient than ever before: exactly what our target customers require. We are going to be explaining the architecture of each feature in more detail over the coming weeks. Here is what SERV v2 update enables: - Multipath Reasoning: This foundational upgrade changes the core of the SERV Reasoning engine. Decision making in the real world is complicated, messy, requires orchestration among multiple actors, and can be contradictory. The same will be true when enterprises implement fleets of AI agents at scale. Multipath Reasoning allows complex decision trees with contradicting rules to coexist in one reasoning graph, upgrading the ability of AI agents on SERV to reason through complicated real-life situations. - Shadow Agents: With the goal of increasing the reliability of outputs to 100% - a baseline requirement for high-stakes environments - Shadow Agents are separate verification agents paired with the main agent. They review every draft against the original brief before anything ships. Missed requirements get caught and rewritten, and only the version that passes gets delivered - preventing errors from poisoning downstream outputs. - Verification Hints: To reduce re-work, cut costs, and increase the accuracy of outputs as we work towards our goal of 100% reliability for enterprise applications, AI Agents will now be able to receive extra signal about what a correct output should look like before they produce one. - Benchmark Tooling: Potential enterprise customers can now see the cost savings and reliability improvements of switching to SERV on their own workloads before integration. For existing enterprise customers, their engineering teams can optimize existing prompts to get even more cost efficiency from the SERV Reasoning engine. - Prompt Guard: Security and privacy are minimum requirements for any infrastructure implemented in high-stakes environments like banking and financial services. Prompt injection is a serious risk for banking AI agents handling trillions of dollars. Prompt Guard's built-in security layer protects AI agents from injection attacks. SERV v2 goes live mid-July with all of these upgrades. Each element in SERV v2 solves an issue that's preventing the adoption of AI agents within enterprises, financial institutions, governments, and fast-growing markets like humanoid robotics. Multipath Reasoning lets agents work in the real world. Shadow Agents and Verification Hints increase reliability. Benchmark Tooling increases cost efficiency and brings new customers through the door. Prompt Guard increases security and privacy. 79% of enterprises need to adopt AI agents in some form (PwC), and SERV v2 enables them to run those agents on OpenServ. The future is looking bright.

Our vision is to become the #1 player in every market we enter. We just announced Q3 plans: expansion into global banking and fintech, alongside humanoid robotics - and the release of SERV v2 in mid-July. Everything shipping in v2 is a direct answer to what banking demands before it trusts AI agents with real workloads. TLDR: The financial services AI agent investment cycle is starting right now, with hundreds of billions in spend coming. First movers among the banks stand to capture billions in extra profit while the latecomers get stuck with an uncompetitive cost structure. Adoption is being held back by two things - trust in agents and the cost of running them at scale. Those are the exact problems SERV was built to solve, and v2 is the biggest step we have taken toward solving them. Some key metrics and trends we are looking at: - Financial institutions are on track to spend $97B on AI by 2027, growing at a 29% CAGR - implying $200 B+ annually by 2030. - 83% of financial services professionals plan to increase AI spending. - McKinsey puts the value of AI in banking at $200-340 B per year. - Citi projects AI lifts global banking profits by $170B - 9% - by 2028, pushing sector profits toward $2 trillion. - BCG's 2026 estimate: AI can raise bank profitability by 30% and cut costs 30-40% by 2030. This is the trillion-dollar market we keep pointing at: AI adds $13T to global GDP by 2030, and banking's slice alone surpasses $150 B. Why the urgency by banks? Because the first-mover math is brutal. Banks that lead on AI gain a projected 4-point ROTE advantage over laggards. For a T1 bank, 4 points of ROTE is billions in extra profit, every year. Early adopters see 2.84x ROI on AI investment versus 0.84x for the laggards. In our research about 70% of banking executives believe AI will directly drive revenue growth while 32-39% of work inside financial institutions has high potential for full agent automation, another 34-37% for augmentation - up to 76% of all work, with cost reductions of up to 70% in some categories. The trend is clear. In 2025 alone, 50 of the world's largest banks announced over 160 agentic AI use cases. AI is being adopted faster than PCs, mobile phones, and the internet itself. The cycle has started. And yet almost nobody has actually deployed: 90% of enterprises want AI agents in production but only 11% have them there, with most deployments killed by unclear ROI and weak risk controls. A third of reported negative consequences from AI adoption come down to one word: unreliability. It is the most aggressive adoption curve of any emerging technology - and the largest gap between ambition and execution. Look closely at that gap and you will see why SERV v2 feature list is constructed the way it is: - Unclear ROI: Benchmark Tooling lets a bank measure cost savings and reliability gains on its own workloads before integrating anything. - Reliability: Shadow Agents verify every decision before it ships, pushing agent fleets toward 100% reliability - the only acceptable number where there is zero margin for error. - Contradictory rulebooks (in banking, this is called compliance): Multipath Reasoning lets agents reason through complex, conflicting rules in a single graph. - Cost at scale: Verification Hints and bounded reasoning cut re-work and tokens, so agents reach reliable decisions cheaper. - Security: Prompt Guard protects agents handling money from injection attacks, by default. With a lot happening behind the scenes, some of the work is already public. Our leadership already sitting in boardrooms with Tier 1 banks holding billions in collective assets. OpenServ on its way to securing certifications regulated markets require - unlocking pilots across banking and fintech, a $460B market in 2026. Neol running SERV Reasoning at 100% reliability in production with the UAE government. ThoughtProof - agent verification layer for banking, compliance, and onchain settlement - hitting 107x performance per dollar on SERV with zero failed calls. We believe this is the biggest economic shift since the steam engine, and financial services is where it lands first and hardest. SERV v2 exists so that when banking moves into AI - and it is moving now - it runs on OpenServ. The future is bright.

CRYPTO-FOCUSED VC FIRM PARADIGM RAISES $1.2 BILLION FOR AI BETS: BBG