Eugene Ng@EugeneNg

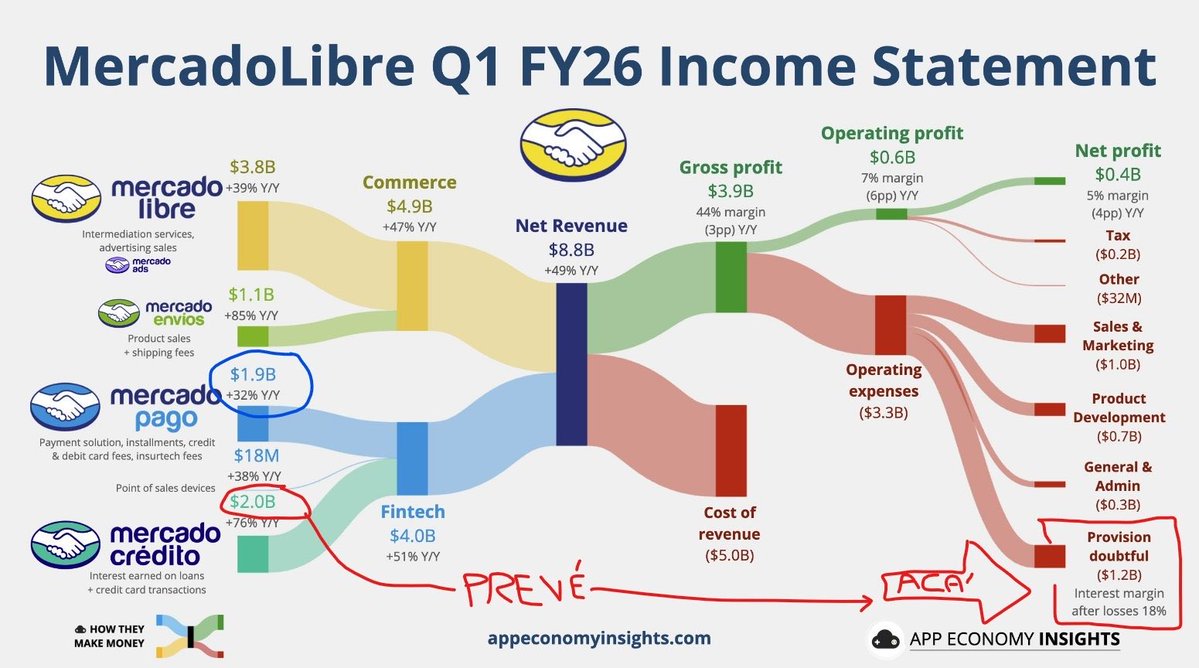

MercadoLibre $MELI 1Q26 Earnings

- Rev $8.8b +49% ↗️🟢

- GP $3.9b +39% ↗️🟢 margin 43.7% -303 bps ↘️🔴

- Adj EBITDA $857m -8% ↘️🔴 margin 9.7% -606 bps ↘️🔴

- EBIT $611m -20% ↘️🔴 margin 6.9% -595 bps ↘️🔴

- Net Inc $417m -16% ↘️🔴 margin 4.7% -361 bps ↘️🔴

- OCF $2.1b +101% ⤴️🟢 margin 23.5% +609 bps ✅

- FCF $1.8b +138% ⤴️🟢 margin 20.4% +761 bps ✅

Total

- Service Rev $7.7b +45% ↗️🟢

- Product Rev $1.1b +84% ⤴️🟢

- Commerce $4.9b +47% ↗️🟢

- Fintech $4.0b +51% ↗️🟢

Brazil

- GMV +30% FXN ↗️🟢

- Sold Items +45% ↗️🟢

- Total Rev $4.8b +55% ↗️🟢

- Service Rev $4.0b +49% ↗️🟢

- Product Rev $787m +92% ⤴️🟢

- Commerce $2.8b +51% ↗️🟢

- Fintech $1.9b +61% ↗️🟢

- Contribution $389m -28% ↘️🔴 margin 8.1% -944 bps ↘️🔴

Mexico

- GMV +23% FXN ↗️🟢

- Total Rev $2.0n +62% ↗️🟢

- Service Rev $1.8b +60% ↗️🟢

- Product Rev $202m +76% ⤴️🟢

- Commerce $1.2b +54% ↗️🟢

- Fintech $781m +76% ⤴️🟢

- Contribution $344m +59% ↗️🟢 margin 17.4% -35 bps ✅

Argentina

- GMV +126% FXN ↗️🟢

- Total Rev $1.7b +23% ↗️🟢

- Service Rev $1.6b +22% ↗️🟢

- Product Rev $91m +32% ↗️🟢

- Commerce $573m +21% ↗️🟢

- Fintech $1.1b +24% ↗️🟢

- Contribution $607m -6% ↘️🔴 margin 36% -1114 bps ↘️🔴

Others

- Total Rev $397m +59% ↗️🟢

- Service Rev $347m +53% ↗️🟢

- Product Rev $50m +127% ⤴️🟢

Commerce $274m +54% ↗️🟢

- Fintech $123m +73% ⤴️🟢

- Contribution $64m +42% ↗️🟢 margin 16% -195 bps ↘️🔴

Biz Metrics

- Unique Active Buyers 84.1m +26% ↗️🟢

- Fintech MAU 82.9m +29% ↗️🟢

- GMV $19b +42% ↗️🟢

- Items Sold 722m +47% ↗️🟢

- Items Sold per Unique Active Buyer 8.6 units +16% ↗️🟢

- Live Listings 773m +62% ↗️🟢

- Managed Network Penetration 95.5% +70bps ↗️🟢

- Same & Next Shipments 199m +39% ↗️🟢

- TPV $87.2b +50% ↗️🟢

- TPV Acquiring $56b +39% ↗️🟢

- TPV Acquiring (off) $36.2b +39% ↗️🟢

- TPV Acquiring (on) $19.8b +39% ↗️🟢

- TPV Fintech Svcs $31.2b +73% ⤴️🟢

- TPN 4.6b +39% ↗️🟢

- Monthly Active Sellers with Credit 36.0% total ↗️🟢

- AUM $19.9b +77% ⤴️🟢

- Credit Portfolio (CP) $14.6b +87% ⤴️🟢

- CP (Credit Card) $6.6b +104% ⤴️🟢

- CP (Consumer) $5.3b +79% ⤴️🟢

- CP (Merchant) $2.3b +64% ↗️🟢

- CP (Asset Backed) $0.3b +85% ⤴️🟢

- NIMAL 17.8% -980bps ↘️🔴

- Past Due 15-90 days 8.0% of NPLs/Total Portfolio ➡️🟢

- Past Due 90+ days 17.6% of NPLs/Total Portfolio ➡️🟢

- % Allowance of Doubtful Accts / NPLs >15 days past due 103% ➡️🟢

- % Allowance of Doubtful Accts / NPLs >90 days past due 149% ➡️🟢

1 | Q1 saw very strong growth as MELI heavily reinvested in its commerce and fintech business.

I'm pleased to report that we ended 2025 with robust operating trends that reinforce the strength of the MercadoLibre ecosystem. Our relentless focus on customer experience translated directly into strong financial performance with fourth quarter net revenues growth of 45% year-over-year. Our performance is supported by 2 primary growth drivers: the acceleration of our commerce business, and the rapid adoption and structural expansion of our fintech services.

2 | Near-term investments in Brazil lowering of shipping threshold, credit card in Brazil, Mexico, and Argentina, 1P commerce and cross-border trade (CBT) with China and US, pressured margins by 500-600bps.

We talked a lot about the results of those investments, but we wanted to give a sense of what those investments were in terms of margin compression….lowering of the shipping threshold that we did last year in Brazil. The credit card, we are investing in Brazil, Mexico and now Argentina, and the 1P, which is continuous its path to profitability, but still not profitable on its own. The same thing with CBT, which we are expanding now to the China and the U.S. corridor and then we also added the smaller countries where we continue to invest as we reach scale in those countries. So when we put all that together, we wanted to give you a sense of the pressure that, that generated on our margins and that gives you a range of between 5 and 6 points.

3 | Continued to enhanced the free shipping value proposition in Brazil commerce, lower free shipping thresholds, driving higher purchase frequency, new buyers, larger volumes, higher revenues, and improving efficiency.

Turning to commerce. In Brazil, our largest market, GMV grew an impressive 35% YoY alongside a 45% increase in sold items. This acceleration is the result of our strategic investments to enhance the value proposition, most notably the decision to lower the free shipping threshold. More free shipping is driving higher purchase frequency and bringing new buyers into the ecosystem. This volume is translating directly into efficiency. Our logistics network absorbed the increase in volumes while driving productivity gains, proving our ability to scale effectively.

4 | Confident of strong underlying unit economics that CBT, 1P and credit card when scaled will be profitable.

In terms of the trajectory, I think it's in line with what we have been talking about this in the past. CBT is a business that when it's locally fulfilled, is profitable, international fulfillment needs to continue scaling and moving in the right direction, but it will continue to scale and it will put some pressure on margins because of that.

When you look at our 1P, I think we talked a lot about 1P. It continues to be profitable on a variable basis level before allocating central cost, direct indirect cost is profitable. So the scale will play in our favor in terms of continuing to improve profitability.

I think the credit card, Osvaldo will talk about this, I'm sure, in some of the questions, but the credit card continues to improve its profitability, in particular in Brazil, where we're seeing already a significant part of the portfolio, the other cohorts being profitable….if you look at Brazil, which is the oldest cohort we have been issued credit cards in Brazil since 2021, cohorts that are older than 2 years are already profitable at a NIMAL level. So that gives us a lot of encouragement to continue expanding the user base.

5 | While NPLs decline slightly QoQ, NIMALs actually improved, more important to focus on what the risk was priced

regarding NPLs and the impact of a little bit -- a slight deterioration in NPLs from the third quarter to the fourth quarter. And that is -- so that is -- I would say that in general, NPLs of the credit card book fell to an all-time low of 4.4% in Q4. Nonetheless, the increase in NPL was mostly related to the consumer and merchant books. But having said that, I think that more important than NPLs are NIMALs and those improve, meaning we are more profitable than we were a quarter before. Therefore, what we did was we increased the number of people and the riskier number of people we give credit to, but we price that risk accordingly. And therefore, we ended up having a significant -- a larger spread than we did on the prior quarter. So I think this was a calculated risk and it worked out well.

6 | MELI remains focused to grow the credit book only if it stays healthy, confident about the quality and health of the credit portfolio with their models and collection.

I think the philosophy on credit has always been that we will grow our credit books as long as we have a healthy book. And as Osvaldo mentioned, you're seeing only part of it -- part of the equation on the NPLs. But obviously, we are pricing those ahead of time. And the margins in Argentina and Mexico are extremely high.

So we feel very, very comfortable about the quality and the health of our portfolio. And that's the reason why you see our credit book growing at 90% because we are confident in our models and our collection.

7 | However in the near-term given the mix of different growth rates and profitability, it is more unclear but confident of the long-term path.

So I think a lot of moving parts, right? The individual businesses are growing and moving in the right direction. Then you have a shift issue because some of these are growing at a faster pace. But the bottom line is that we're very confident that the investments that we're making in our platform and addressing the long-term opportunities that we see ahead of us, and we're also improving user experience in our platform.

This particular quarter, we mentioned that we have the highest NPS level in commerce and fintech in Argentina, Brazil and Mexico. So that's a consequence of investments that we have been doing, and we're very comfortable with these levels of investments in our ecosystem.

8 | Argentina saw margin compression largely due to the opening of new fulfilment centers, and higher bad debt provisions from the credit card launch last year, combined with higher funding costs.

We see, as you mentioned, some compression in Argentina. Keep in mind, Argentina continues to be the highest profitability market in terms of margins. But we did see some compression mostly coming from fulfillment. As you know, we opened couple of new fulfillment centers recently, so that generated some year-on-year compression on COGS. Also, provisions for bad debt because of the credit card. We launched the credit card in the middle of last year. So we're still -- we're seeing some compression because of that. As you know, the credit card requires investments upfront. And there is some year-on-year increase on funding costs. It's true what you said. Sequentially, QoQ, the funding cost of our credit portfolio was lower in Q4 relative to Q3, but it still was higher relative to a year ago. So those are the main reasons for the compression that we saw in this quarter.

9 | In agentic commerce, focusing most of efforts of developing with MELI instead, because they have the first-party data to create the best search, recommendation, discovery.

to complement this comment, I would say that the part where we're putting most of our efforts is in developing our own agentic experience inside MercadoLibre. We think and we are convinced that we have the first-party data to create the best search, best recommendation, best discovery engine on which we can personalize and lay over the agentic experience that the new technology drives.

So -- and by the way, if you believe that there is a world of agentic commerce, that could mean that retail will move even faster from the offline to the online world. So all this to say that I do think that we are well-positioned to actually capturing ad revenues in the future because we still think that MercadoLibre will be go-to place for demand to do shopping online.

10 | Because they don’t know which hardware, which model people will use, and customers look for value and for the best end-to-end experience, it makes sense to take the risk and focus all of their efforts to build their own agents and shopping assistant within MELI instead.

Let me try to rephrase what I meant earlier as I try to address your point. I think there are things that we know and there are things that we don't know. So we don't know which hardware people will use in 10 years to buy. We don't know whether the winning model will be X, Y or Z and so on. We do know that consumers do value or do look for the best end-to-end experience. We do know -- and that means not only searching for products, but also getting products fast, having the widest selection, pricing, the best financing alternatives, post-purchase support and so on.

We also know there's a technology today that can dramatically improve the product discovery process. And for that reason, we are putting all of our efforts and deploying lots of engineers in building our own agents and our own shopping assistant within MercadoLibre. It's early to know what will happen with other shopping assistant. I take your point that it might present a risk. I understand where you're coming from. But we are confident that we are playing this one from a position of strength that we have the relationship with consumers. We have a brand that Latin America loves.

11 | Advertising should benefit if MELI can capture more agentic commerce traffic.

So we eventually what I'm trying to convey is that on the one hand, we are confident on MercadoLibre's own ability to capture traffic through its own agentic experience. And on top of that, we do think that advertising represents an additional revenue opportunity in a world in which there is agentic commerce.

And by the way, the agentic world can also imply a faster shift of advertising dollars moving from traditional offline channels into digital advertising, which generates the opportunity to be even bigger. So we remain positive, we remain focused. The only thing that we know for sure is that we need to put our developers to work to have the best tech stack for advertising and the best agentic experience inside MercadoLibre.

12 | Advertising revenue grew 67% in 1Q26 on broad base strength, driven by higher adoption and tech-stack improvement, excited about the long-term opportunity.

we are very pleased with the performance we had in ads this quarter. Revenue accelerated to 67% on an FX neutral with higher adoption and spend basically driven by improvements in our tech stack. It's broad-based. So there's no one silver bullet driving that growth.

But basically, we are attaching our product in the different parts of the value chain, right, auction bidding, placement optimization, demand generating initiatives and all that powered by an improved an easy-to-use platform in terms of front end for our customers. So extremely, extremely satisfied with that.

So penetration of ads with revenues as a percentage of GMV is still small compared to its potential. So very happy with the results so far, but even more encouraged with the potential looking ahead.

13 | Mercado Pago's AI assistant is solving 87% of interactions without the need for human support, right now it is largely servicing, but excited with it cross-selling and recommending services.

We are very excited by Mercado Pago's AI assistant it is already helping mostly with solving questions and concerns from our users. We have built a lot of functionality into our agent. Basically you can do pretty much everything you do with Mercado Pago with the agent.

Our Mercado Pago AI assistant is solving 87% of interactions without the need of human support. Millions of users already adopt this conversational tool to manage their credit card, make transfers and understand their credit offerings.

And beyond cross-sell, it will also become more proactive in terms of acting like a personal banker. So helping you, I don't know, allocate your portfolio or make the recommendations of what kind of credit is better for you. So we believe here that the opportunity is significant.

14 | AI seller assistant is currently already helping sellers with 20% of GMV

Just to complement Osvaldo here on the marketplace side, while we have many, many features that are powered by AI, starting with our search algorithm, our recommendation and so on, I think it's worth highlighting the fact that we have a seller assistant today running in our platform, basically 20% of our GMV is somehow advised by our assistant. It's actually proving to be pretty successful in helping sellers improve their live listing, reduce their lead times to get better reputation in our platform, capture some of their questions and requirements in terms of customer support.

15 | MELI’s lower margins comes not from weakness but from deliberate decisions to pursue growth opportunities that will gradually become more profitable over time. It is already showing up in improved customer metrics, NPS, higher revenue growth.

first, it's important to put in context when we talk about margins, the growth that we're delivering. Most of the margin pressure comes from deliberate decisions that we're making in terms of pursuing investments that are generating tremendous growth and improving user experience. As you mentioned, in Brazil, in particular, we have been growing our GMV and gaining market share, mainly because of these investments. Our top line grew by 45% year-on-year. As I mentioned earlier, our NPS is at record levels, and that's because of the investments that we have been doing. You mentioned CBT, 1P, the lower shipping presold, expanding more free shipping, increasing booking capacity. So we feel very comfortable with these investments and the current margin levels because we are seeing the results in terms of growth, market share gains and improvements in user experience and engagement.

16 | MELI will not hesitate to invest to capture these opportunities even if there will be short-term margin pressure, because they are not optimising for short-term profitability, but seeking to grow the business for the long-term.

As I said in the past, our main focus is on capturing the large opportunities in front of us in commerce, fintech and advertising. And we will not hesitate to invest and to order to capture those opportunities as we have done in the past, even if that puts some short-term margin pressure, we're not trying to optimize short-term margin. We manage the business for long term -- from a long-term perspective, we believe these investments are creating a foundation for future growth, and we remain confident in our long-term margin trajectory.

➡️ Key takeaways for MercadoLibre $MELI

MELI continues to grow as LATAM’s dominant e-commerce and fintech platform with a long growth runway with still low penetration. Unsurprisingly, the market in the near term often does not like companies who reinvest heavily and profitability falls. The difference is that the reinvestment is already showing up in strong growth and the underlying profitable unit economics are there, all MELI needs is time to grow and scale each opportunity. Confident in management taking the long-term to grow the business rather than to manage short-term profitability which is what we are not interested in.