Sabitlenmiş Tweet

New Year... first tweet... Building a reading list specifically for aspiring credit analysts and credit investors. Some suggestions below, any thoughts on what's missing? 🙏

1/4

English

HY Credit Geez

520 posts

@HYcorps

HY credit analyst. Sell side, then buy side. ~15 years. Pro rugged individualism.

@HYcorps DBOX is laughable here. Apparently people don’t realize they can track the box office in near real time.

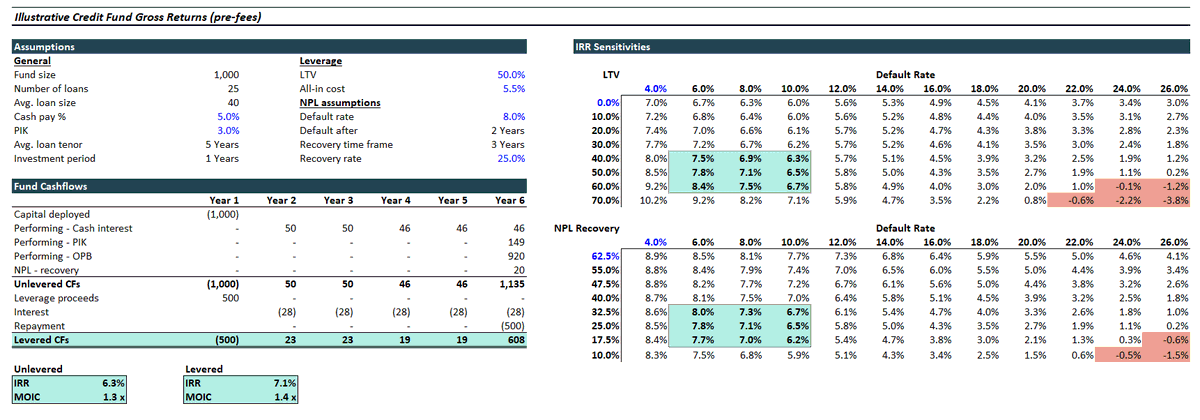

Let’s do some basic math 8% default rate (extremely high) 25% recovery (extremely low) 6% credit losses Avg coupon is Cash+ ~5% Slightly less than cash, a bit worse with management fees/expenses (no carry) in this scenario This is not the end of the world. Someone want to run this for PE if we get large losses and multiple compression and weak/negative earnings growth 😏

@StocksEddie No, no, noooo… seeing some terrible takes in the comments. Time for a rethink: invest exclusively in obscure, Canadian microcaps. Preferably unprofitable, and ideally on the venture exchange. Remember to size large or it doesn’t count. This IS financial advice. You’re welcome.