Sabitlenmiş Tweet

February 2026 portfolio update is now available:

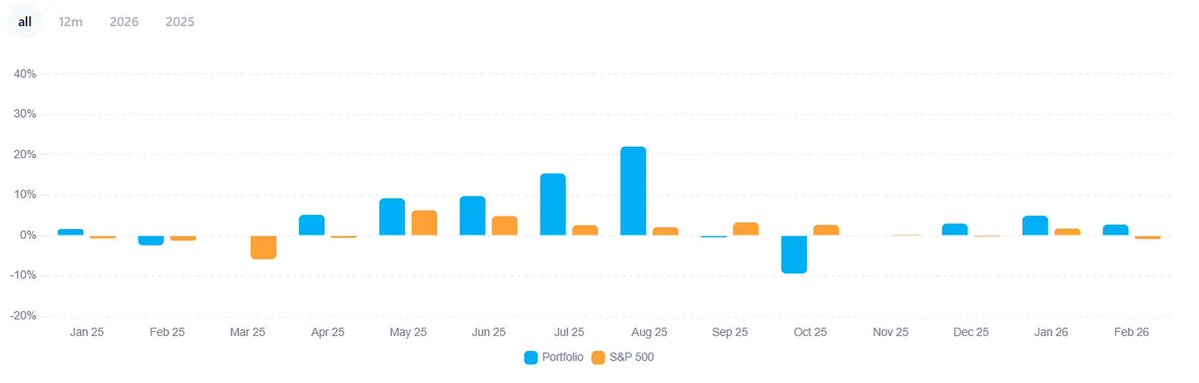

7.79% YTD performance (2025 returns were 64.3%)

Investing in small, cheap businesses with room to grow—mainly independent trend players that are relatively decorrelated from the market.

Full deep dives every week, management calls, and some macro notes. If that sounds interesting, check out Undervalued and Undercovered (link in bio).

English