HUNGRY PANDA

52 posts

HUNGRY PANDA retweetledi

HUNGRY PANDA retweetledi

From the moment I discovered cryptocurrency, until the moment it ran through my veins and became the air that I breathed, I vowed to make my contribution. I won’t stop until our dream is realized: make money for the people, not the banks.

San Francisco, CA 🇺🇸 English

HUNGRY PANDA retweetledi

Drop your Webauth @ and I’ll send you something on the XPR Network. DM okay if you wanna stay in the shadows.

English

Bring all of your favorite assets to the @XPRNetwork and start using your crypto.

Supply assets like $SOL and $LTC on @MetalXApp Lending and earn competitive APY instantly.

No gas. No friction. Just yield.

Try it: app.metalx.com/lending

LOAN Protocol@LOAN_Protocol

Top Lending Markets APY Snapshot. ⛓️ app.metalx.com/lending Deposit assets and start earning immediately. No Transaction Fees, No Minimum Lock.

English

HUNGRY PANDA retweetledi

HUNGRY PANDA retweetledi

HUNGRY PANDA retweetledi

Best video yet.

Cut the red wire and cut the blue wire.

No cut the wire in the back of our heads.

We are feeding the machine.

English

HUNGRY PANDA retweetledi

We must not forget what we are fighting for in crypto. We are fighting for our freedom. We are fighting for open money that is transparent and unalterable. Something we have never had before in human history, true freedom, is now within grasp.

English

HUNGRY PANDA retweetledi

DARK POOLS 😈

$XRP & CRYPTO HOLDERS 👀

LETS BLOCK OUT THE NOISE IN 2026 AND

LOCK THE F**K IN 🔒

Cypress Demanincor@CDemanincor

Oh ZACK Our institutional professional is patiently waiting for your response We’ve opened the door for the invite Ball is in your court now and everyone is watching 👀

English

HUNGRY PANDA retweetledi

Please I will gladly set up the call

with our in house institutional scalper and he can GLADLY take you to school on how institutional pricing actually works.

Our Algorithms that track dark pools aren’t seeing trades at those levels they’re seeing liquidity, orders, and institutional interest sitting at those levels.

A market doesn’t need to trade a price for that price level to exist.

It just needs resting liquidity.

On chain spot markets only show you executed prices. (What Zack is mentioning)

Dark pools and institutional order books show you intended prices.

Resting limit orders far above or far below current price

Large conditional blocks of liquidity

Iceberg orders that reveal only tiny portions of their real size

Pegged orders that automatically adjust relative to NBBO, VWAP, or delta zones

None of these require the asset to have touched that price.

If XRP is trading at one price and an institution quietly parks a massive block order far above or below it, retail will never see that level. On chain won’t show it. CEX order books won’t show it. But our institutional routing systems and dark-pool tracking software can see the footprint of that liquidity long before price ever gets near it and we have the track record to prove it.

Dark pools don’t operate on price history they operate on price intention.

They function more like matchmaking engines and liquidity balancing networks where institutions place conditional orders that say, “If the market ever gets here, fill me.” That intention alone creates a level.

Zack please educate yourself before you speak to someone who has 9 years of market experience and works with professionals who have over 13 years of professional hedge fund experience.

The asset doesn’t need to touch the price for our algorithm to detect the size, the interest, and the probability of that zone being targeted in the future.

That’s why our institutional software consistently maps levels days in advance accurately because liquidity is the real magnet.

Again I would love to set up a call with you and our professionals to teach you a lesson.

Serve you bullish moon boys up on a silver plate with some REAL institutional insights 🍽️

English

HUNGRY PANDA retweetledi

HUNGRY PANDA retweetledi

Wife was right. Next month is gonna be brutal

Teneika Askew | Analytics & Automation@teneikaask_you

SNAP (food stamps) will be cut off after October due to the shutdown

English

HUNGRY PANDA retweetledi

$XRP $XPR 💥CRYPTO & THE FINANCIAL CRISIS💥 x.com/i/broadcasts/1…

English

HUNGRY PANDA retweetledi

Everybody who takes showers daily in 🇺🇸America is in 💀DANGER☠️

peep what’s in your TAP water, just input your Zip code on this site below

ewg.org/tapwater/

English

HUNGRY PANDA retweetledi

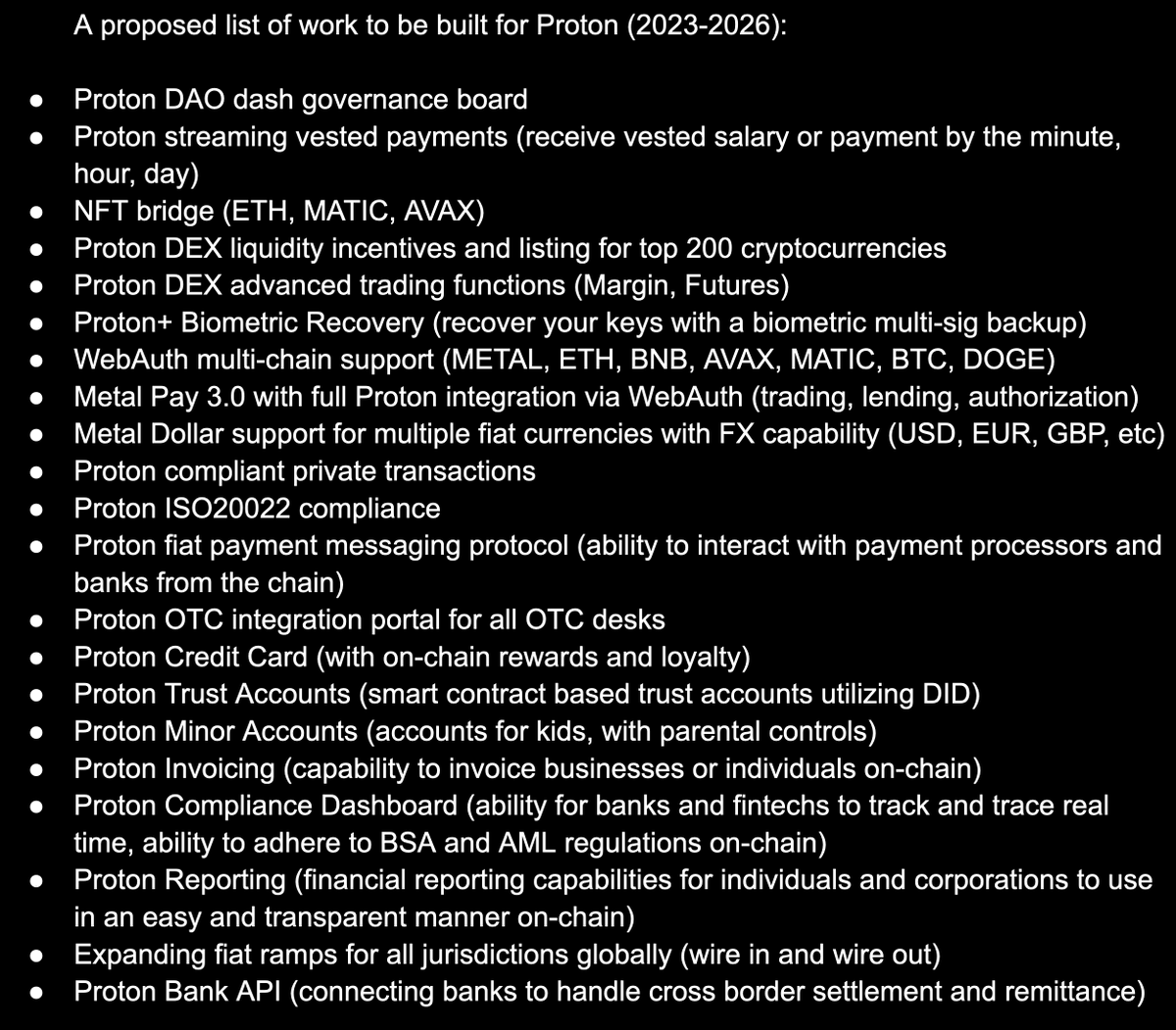

This is how Metallicus’s “LOAN card” system could actually function in the wild once the architecture’s fully online.

Not fantasy—just extrapolating from what’s already coded into $XPR, $XMD, $LOAN, and $METAL.

*Powerful,Innovative*

1. The Setup — You as a Staker

You deposit, say 100,000 LOAN into a staking contract.

That does three things at once:

Locks collateral that determines your credit limit (let’s say $5,000).

Starts generating staking yield (APY on LOAN).

Writes your on-chain credit identity — a verifiable smart profile showing repayment history, stake size, utilization, etc.

You’re now your own bank. No FICO, no background check, no clerk.

2. The Spending — “Credit via #Blockchain”

You swipe your LOAN card (or use an app wallet) to buy a $500 flight.

Instead of Visa approving you, the @LOAN_Protocol auto-verifies that you have available credit based on your staked amount.

The merchant receives XMD stablecoin instantly via the @XPRNetwork, no fee.

You now owe $500 in credit, just like a card balance.

⬇️

But no interest—because your stake’s yield will start paying it down automatically.

3. The Repayment Loop — #Yield Eats Debt

Let’s say your staked LOAN is earning 12% #APY. That’s about $1,000 per year in yield.

The protocol can auto-route that yield to your outstanding credit balance.

So instead of paying 20% #APR like a normal credit card, your balance is shrinking every day you hold your stake.

That’s the “negative interest” @MarshallHayner’s hinting at—a self-liquidating credit model.

Over time:

The longer you hold, the less you owe.

The more you stake, the higher your credit limit.

Your credit score becomes a mathematical output of your blockchain history, not a centralized file.

4. The Merchant Side — The Silent Revolution

Merchants get paid in XMD instantly and can convert to fiat, hold in crypto, or stake back into Metal’s ecosystem.

They don’t pay interchange fees.

Visa takes ~2–3% of every transaction in the old world—this model takes 0% and rewards both sides instead.

That’s how #adoption snowballs: merchants chase higher profit margins, users chase yield-backed spending.

5. The Network Effect — Institutional Scale

Here’s where METAL and $MTL enter:

Banks, fintech apps, or even countries can spin up #subnets (L3s) using Metal’s protocol.

Each subnet could issue its own #stablecoin—say, “JUPUSD”—anchored to XMD but used for localized markets.

All those subnets connect back through METAL as the cross-chain settlement #rail.

So you get a federated credit system where every participant—user, merchant, institution—earns yield from the same base token: LOAN.

6. The Endgame — “The LOAN flywheel”

Picture this flywheel:

1. Users #stake LOAN → earn yield → get credit line.

2. They spend via XPR → repaying in XMD.

3. Merchants accept XMD → stake for yield or liquidity.

4. Staking feeds yield → yield pays off loans.

5. The cycle repeats, compounding protocol demand and token lockup.

Every swipe locks more $LOAN, burns more supply, and pushes the protocol toward self-sustainability.

Why It’s Massive

This model doesn’t just disrupt banks—it removes the concept of debt slavery.

Credit becomes a collateralized privilege, not an obligation.

And the more people join, the more the system rewards good behavior instead of exploiting it.

It’s #DeFi with a moral spine: yield replaces interest, transparency replaces exploitation.

-it’s the kind of system that could make traditional credit cards look medieval.

The biggest signal to watch next: when they start testing on-chain credit scoring or LOAN-backed stable credit lines on XPR Network Testnet. #Crypto

English

HUNGRY PANDA retweetledi

I hate to be the one to spoil the surprise...

...but back in May, a proposal was passed to add the 3 — $XLM, $ADA, & $SOL — to the Metal X DEX & $LOAN Protocol!

-------------------------

DEX: 3/3 ✅

LOAN: 2/3 ⏰👈

-------------------------

Again, this was made possible due to the passing of a proposal on the @XPRNetwork Governance Dashboard.

Whether $XDC, $AVAX, $SHX, $FUZZY, $QNT, $VELO, $ZBCN, or $LINK gets added to the @MetalXApp DEX or @LOAN_Protocol Lending Markets, it is ***YOU*** who plays a part in getting that done & to expand the ecosystem.

⚛️Add XDC Network $XDC To The LOAN Platform:

gov.xprnetwork.org/communities/5/…

⚛️Add Telcoin $TEL To The LOAN Platform:

gov.xprnetwork.org/communities/5/…

$XPR $METAL $LOAN $XMT $MTL $XMD

LOAN Protocol@LOAN_Protocol

Any guesses which market we're adding next?

English

I wish _______, my favorite financial institution supported Metal. List them below 👇✍️

English