IveBeenEatingWell

57 posts

IveBeenEatingWell

@IBeEatingWell

You can’t help what you’re born with, but it’s on you if you die broke

Katılım Kasım 2021

68 Takip Edilen16 Takipçiler

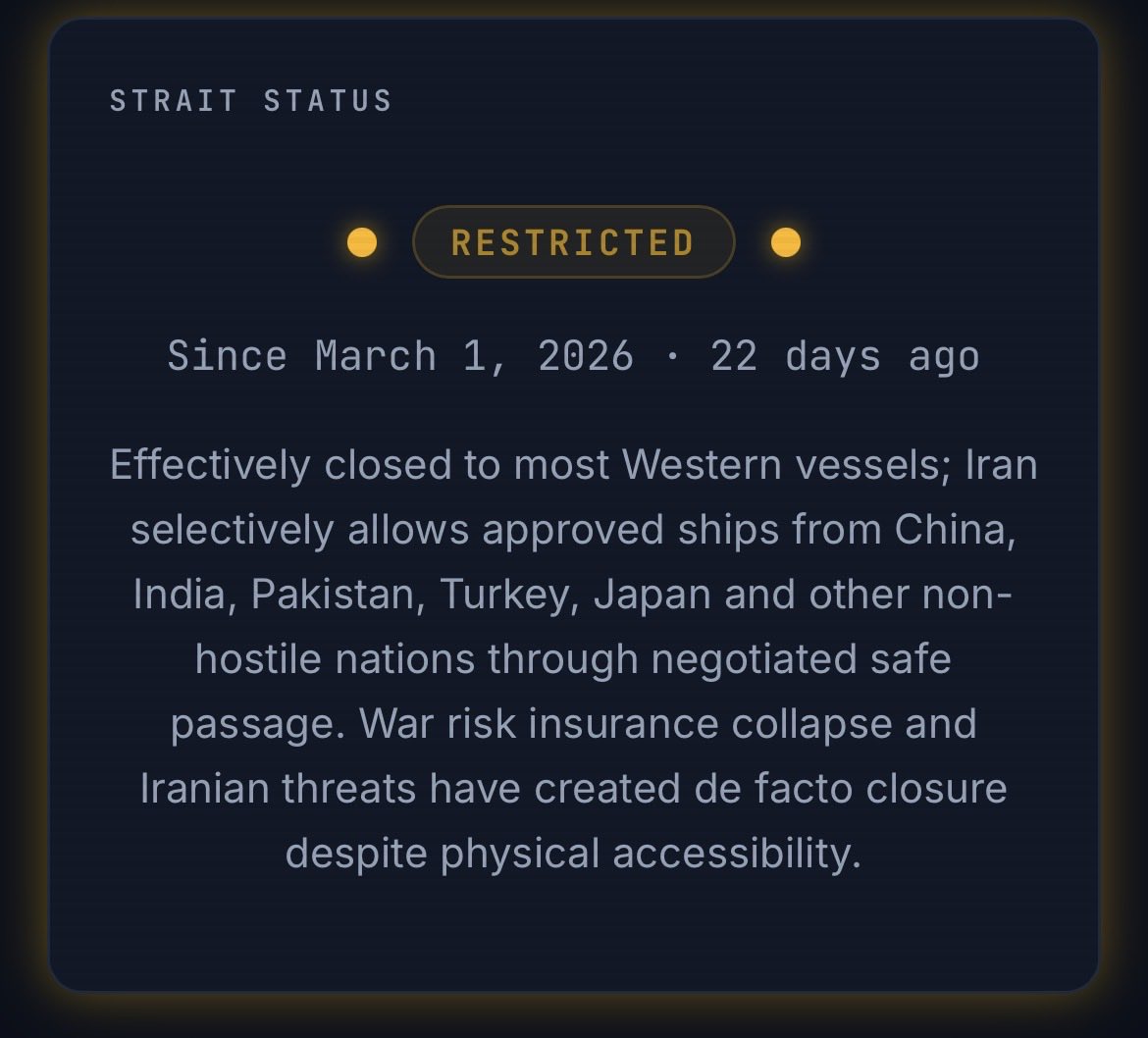

Iran just dropped the most humiliating ultimatum on Washington. They demand the closure of ALL US bases in the region, a $2M toll for Western ships in Hormuz, and $100 billion in reparations. They are treating the US like a defeated empire.

English

@IBeEatingWell @PCashmere81 @FurkanGozukara “Let’s just focus on this one objective instead of the 10 other ways Iran is being dominated”

English

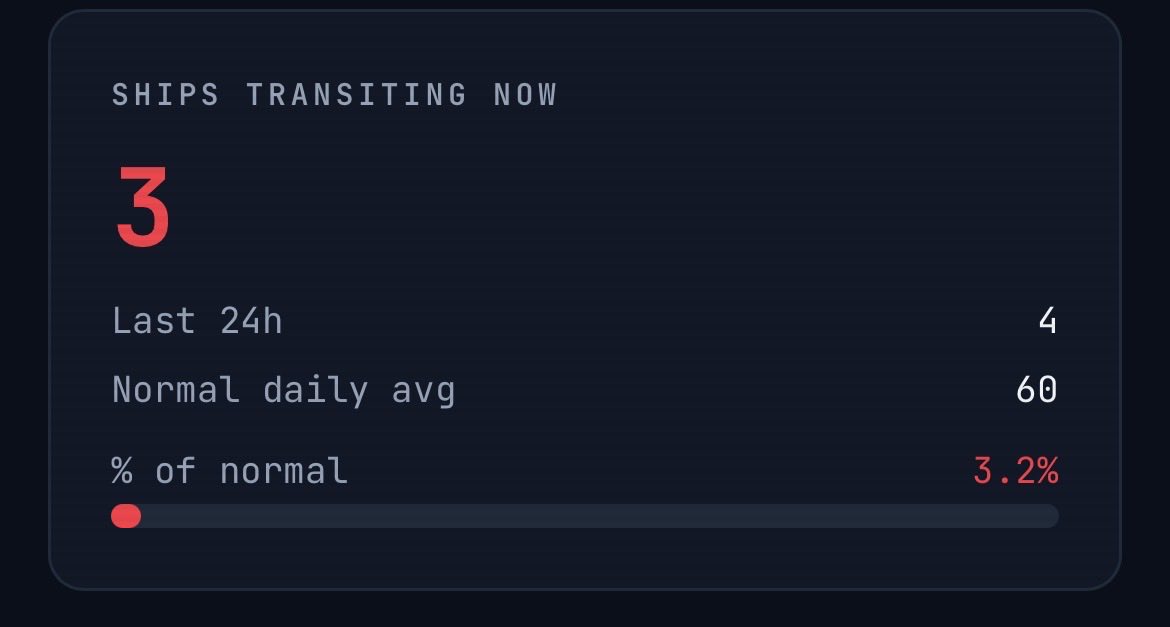

@PCashmere81 @FurkanGozukara Simple question, is the strait open? Enough said

English

IveBeenEatingWell retweetledi

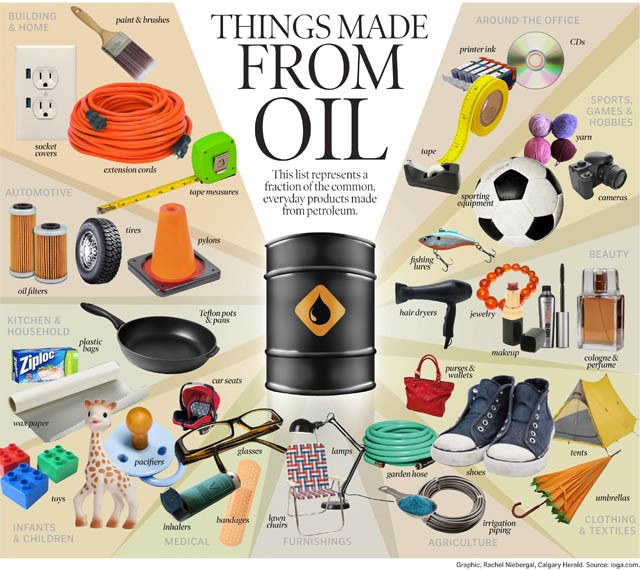

These "oil and gas are in everything" graphics are about to get very real super quick for a lot of people.

Brian Tycangco 鄭彥渊@BrianTycangco

Spoke with some friends in the plastics business. They are just about out of raw materials and cannot find new supplies as China restricts exports of petroleum-related downstream products. This is going to get much worse before it gets better.

English

@Elon_fanboy77 @jukan05 Same reason Lisa visited South Korea for the first time since she took helm in 2014, because memory makers call the shots now. reuters.com/world/asia-pac…

English

@ekwufinance I'm not too certain. Nvidia is investing in companies that transmit data and energy using light particles. Someone can correct me if I'm wrong

English

Copper relative to the S&P is back at 1999 levels.

Last time this happened:

- Copper outperformed the S&P 5:1 over the next decade.

- Major producers like Southern Copper outperformed 26:1.

History doesn’t repeat perfectly, but setups like this don’t happen often.

Life-changing money will be made in copper.

English

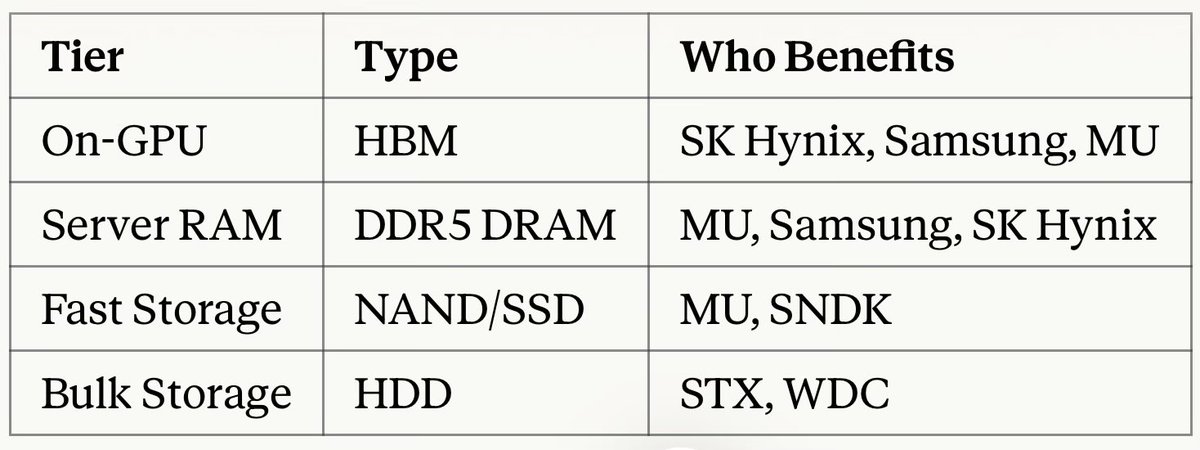

$MU $EWY $SNDK $WDC $STX

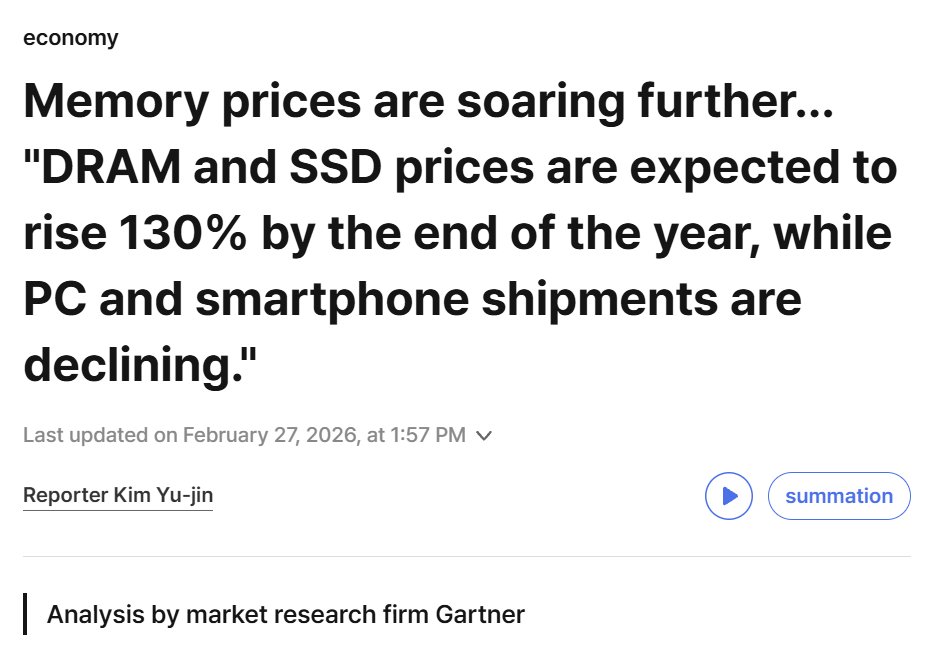

For AI Training/Inference (GPUs) we need HBM (High Bandwidth) Memory, stacked DRAM sitting directly on the GPU package (H100, B200, MI300X). Insanely fast bandwidth is critical for AI. This is the #1 most constrained and in-demand memory for AI. SK Hynix, Samsung and Micron are the top players in this category.

Equity investor@equitydd

$MU - Memory supercycle with 2026 HBM capacity fully booked and 300%+ earnings growth expected as AI-driven demand collides with tight supply. $SNDK - Up 1,600% post-spinoff from Western Digital, riding the severe NAND shortage with AI data center demand accelerating through 2026. $WDC - Dominant HDD market position (63% share) with sticky enterprise contracts offering downside protection as AI storage needs explode. $STX - AI data storage demand surge with quarterly beats driving the stock 35%+ year-to-date alongside memory peers.

English

@stckpkr7000 @yianisz SK Hynix as well, which had a higher return over the 1 year.

2 of the 3 key beneficiaries of the projected memory crisis leading into 2028.

English

@yianisz It's basically up on It's Samsung position.

Hamilton, VA 🇺🇸 English

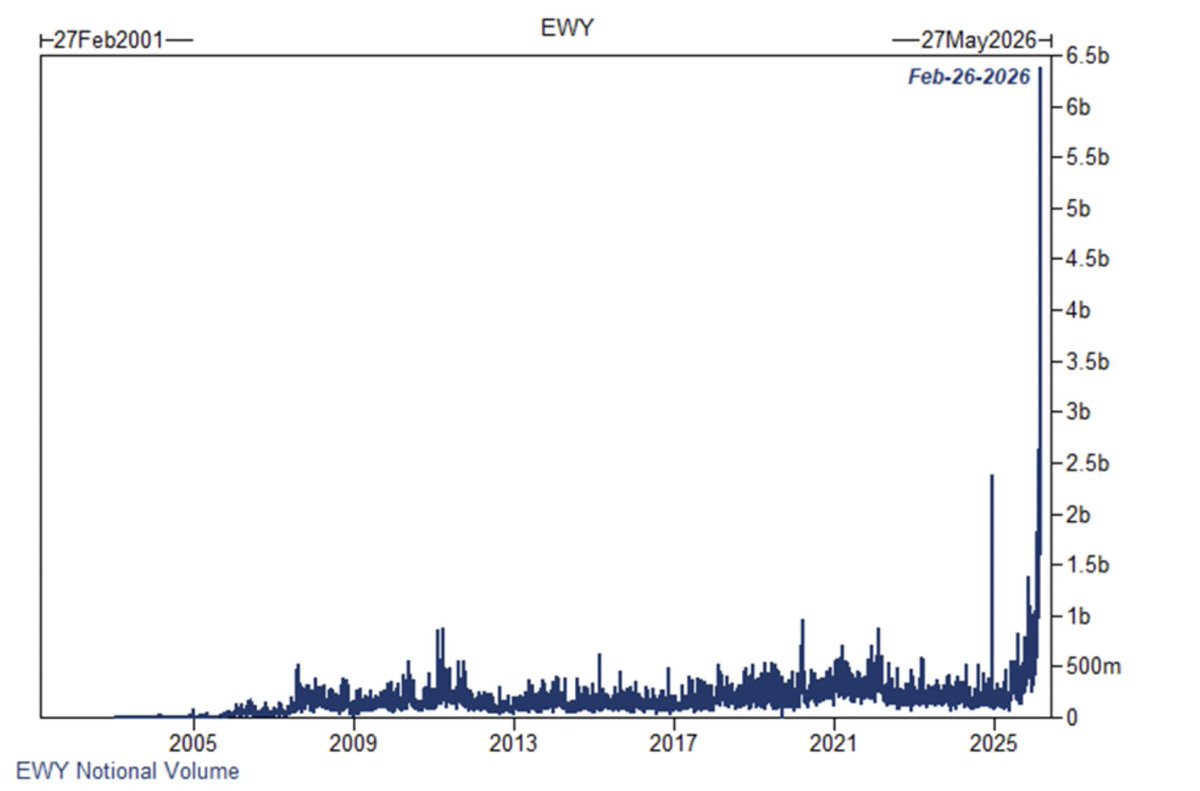

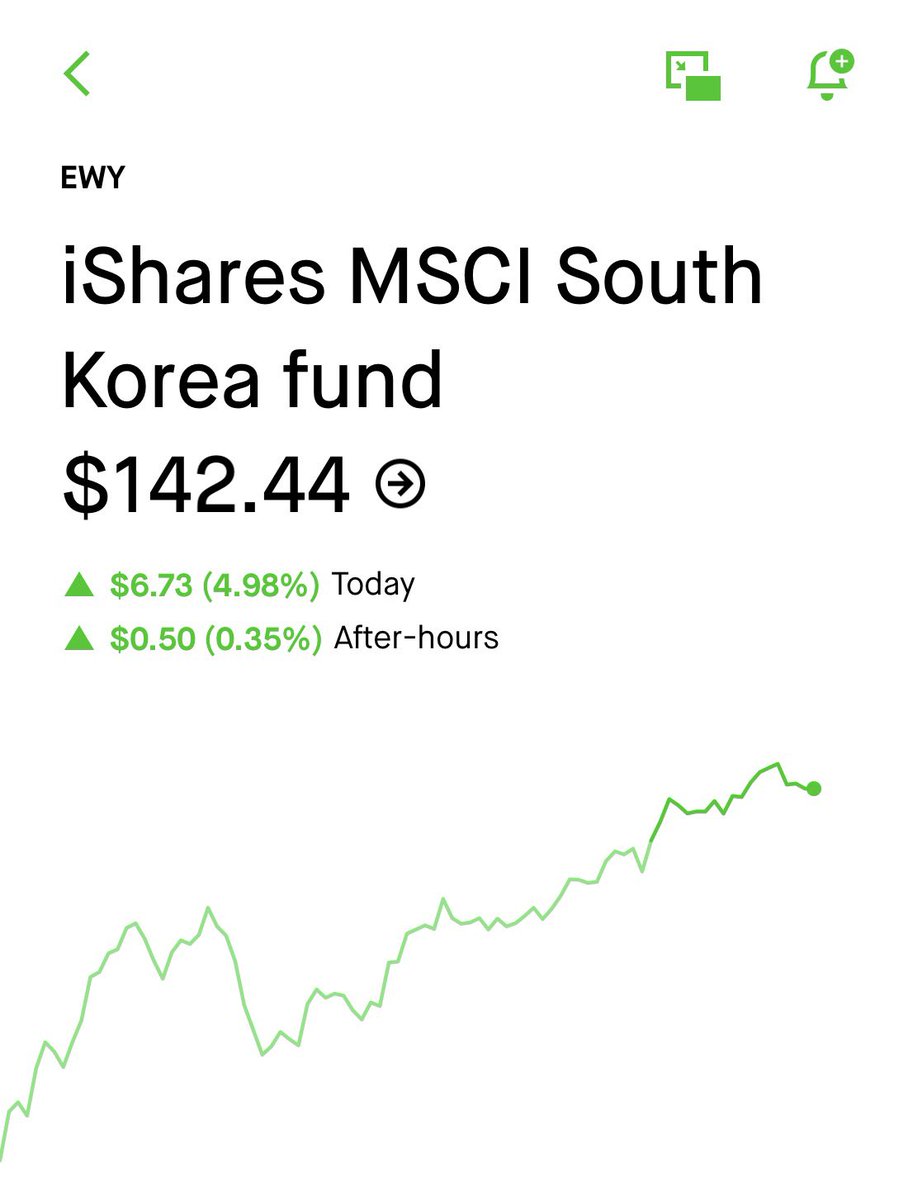

$EWY is more overbought than ever.

$17B volume. RSI screaming.

Everyone calling blow-off top.

Funny thing about breakouts?

They feel most dangerous right before they go vertical.

Overbought can stay overbought…

especially in a hardware supercycle.

English

@Etto_R_Flo @50ptMAE Over a 15 year period, the EWY had gained only 34.82% leading up to the Stargate announcement.

Since then, it has surged 91.92% due to nearly 50% of their holdings being a key beneficiary to the projected memory crisis leading into 2028

English

@Ron_Trades Over a 15 year period, the EWY had gained only 34.82% leading up to the Stargate announcement.

Since then, it has surged 91.92%

Driven by the fact that two of the ETF's major holdings, Samsung and SK Hynix, are key beneficiaries of the projected memory crisis leading into 2028

English

Stan Druckenmiller’s current positions:

- LONG Korea + Japan (+ Brazil)

- LONG Copper (AI + tight supply)

- LONG Gold (geopolitics)

- SHORT Bonds

Portfolio is no longer "AI-driven". He’s bearish on the Dollar but bullish on the US economy with disinflationary growth.

English

@TradexWhisperer I hope you’re right since months…after yesterday i lost fate.

English

@cfromhertz Two stock, Samsung and SK Hynix make up 40% of $EWY's holdings.

English

$EWY S. Korea

2nd largest volume day ever

may be time for some consolidation here...

English

@KakashiCapital_ @0xMentalIllness Asset allocation isn’t the same among those two for Samsung and SK Hynix, people are buying in for exposure Korean memory makers

$IEMG : 14.05% total (4.59% Samsung + 2.55% SK Hynix)

$EWY : 47.31% total (28.36% Samsung + 18.95% SK Hynix)

English

@aleabitoreddit I wanted exposure to Samsung/SK Hynix and loaded up on 2028 contracts Monday open, thanks 🙏

English

Probably up there with my most legendary calls to date?

Your portfolio would have doubled in a week off IV expansion alone.

Hope you listened anon - $EWY.

IV: 32% -> 44.7% and still going.

Serenity@aleabitoreddit

Trade idea that I published to my shower thoughts channel: Korean Index volatility arbitrage and taking advantage of Black-Scholes models. $EWY long options seem mispriced. This is Blackrock's Korea Index, which is majority memory (Samsung Electronics, Sk Hynix). The stock swings 2-5+% a day, and is up 136.25% 1Y, despite priced like a normal index IV. Samsung is volatile. SK Hynix is volatile (eg. 65% - 80% est). But the combination of the two through the index is priced way less than both low beta $GOOGL (37.33%) and $AMZN (39.12%) at ~32% IV. I've been watching $EWY for a bit and it does look volatile. As for pricing my guess is MMs priced in IV based on historical averages (5-10 years), where the Korean index was completely flat. And were expecting calls 2 years out to revert to the mean. But this volatility should be the new norm as markets price in the new memory supercycle (eg. $TSM went from 30% IV to 46.2% IV). Long calls should benefit from both Samsung + Sk Hynix carrying the index. And the main benefit is vega expansion that you won't get from $KORU. You also can't get this option MM pinning like individual US stocks since this is Korea's national index and long term. TLDR: Individual components SK Hynix + Samsung are highly volatile. They're basically half of the index, but options in index are priced with low volatility, perhaps due to historical 5-10 year data. Long calls benefit from vega expansion that weren't priced in correctly as MM forward vol estimates are anchored too heavily on historical realized vol, which was low for $EWY over the past 5-10 years

English

This snapback rally is not a sign of a healthy market.

English