Imran Mansuri

138 posts

The biggest mistake I made in stock market is selling my winners early

Here are few live examples👇:

Mistake 1-Deepak Nitrite at 400

Mistake 2-Shilchar technology at 800

Mistake 3-ACE at 180

Mistake 4-HAL took at IPO but sold due to underperformance in 2020

Mistake 5-CDSL at 260

Which stock have you sold early?

English

𝗧𝗼𝗽 𝟭𝟬 𝗕𝗶𝗴 𝗩𝗼𝗹𝘂𝗺𝗲 𝗕𝗿𝗲𝗮𝗸𝗼𝘂𝘁𝘀 🔥

20-30% upside targets 🎯

A Mega [ Thread ] 🧵

9 more below 👇

⭐️ 1] RPP Infra

English

@Chart_Wallah108 Sir KPI green energy me kya karna chahiye ?

Filipino

𝗙𝗿𝗲𝗲 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗻𝗲𝘅𝘁 𝟯𝟬 𝗠𝗶𝗻𝘂𝘁𝗲𝘀 !

Ask any stock market query

Kindly 1 person - 1 query : )

Ask below 👇

English

Your which stock has fallen the most In the recent correction ?

Tell below 👇

English

@vardhiitbhu Sir why Promoter holding decreased and public holding increased in October?

English

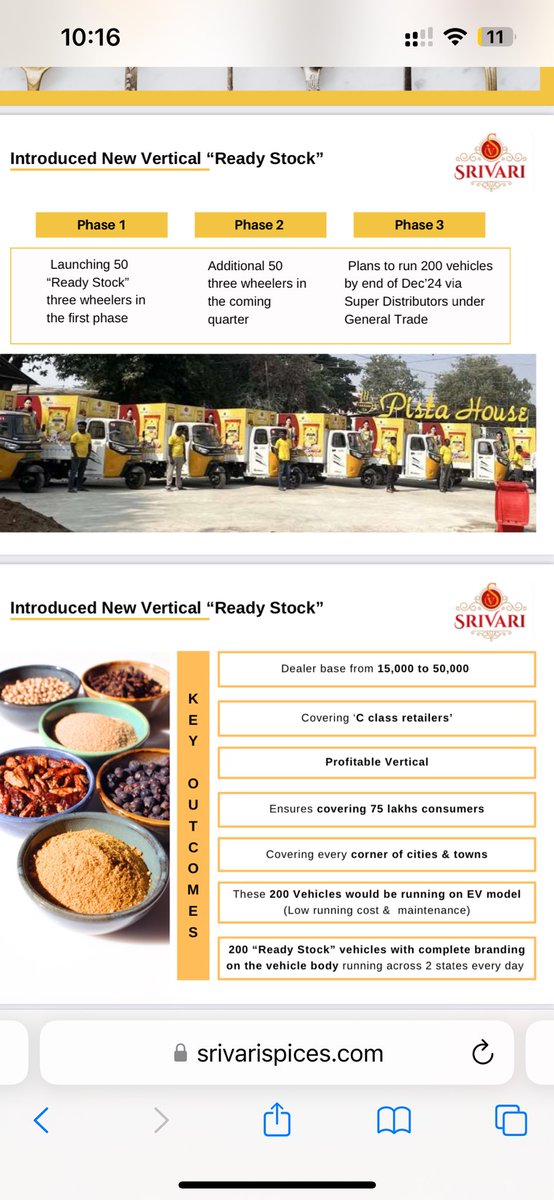

🚨 Srivari Spices (SSFL) Deep Dive 🚨

🔻 Stock has corrected from its peak, offering an attractive entry point!

Management is optimistic, targeting 100% growth over the next 5 years. Even if they achieve a more conservative 40-50% growth, this stock can turn into a multibagger 📈 with a current P/E of only 27. Here’s why:

1. New Vertical - “Ready Stock” Initiative 🚚

•Phase 1: Launched 50 three-wheelers for rapid stock delivery.

•Phase 2: Adding 50 more vehicles next quarter.

•Phase 3: Targeting 200 EVs by Dec ’24 for wider distribution, ensuring coverage across cities & towns with minimal running costs.

2. Dealer Network Expansion 📊

•Dealer base expected to jump from 15,000 to 50,000.

•Focused on covering ‘C class retailers’, expanding reach to 75 lakh+ consumers.

•Building confidence through dealer meets, engaging 1000+ wholesalers in Telangana & Andhra Pradesh.

3. New Product Launches 🌶️

•Adding 15 new masalas.

•Introducing groundnut oil (low fluctuation) and rare safflower oil (no other company serves this pure).

•Continuous pipeline expansion to capture unique product segments.

4. Entry into Modern Trade Platforms 🛒

•Successful presence in Ushodaya, BigBasket, DMart (Online).

•Entered Reliance Jio Mart’s top 50 stores.

•Plans for Lulu, Metro Cash & Carry, Swiggy Instamart, and more.

5. Brand Visibility & Market Penetration 🌍

•200 branded “Ready Stock” EVs for consistent exposure, operating across two states daily.

•Targeting rural penetration and A+ category retailers to maximize market share.

With strong growth catalysts, entry into modern retail, and a vast dealer network, SSFL is positioning itself for sustainable growth. 📈

#SSFL #Stocks #Multibagger #srivari

English

@Chart_Wallah108 Sir Aap konsa add kar rahe ho ye bhi bataiye 😃

हिन्दी

What are you adding in today's mahurat trading ?

Tell your picks 👇

English

Drone Destination H1FY25 Results!

Poor results in my opinion.🧸

Sales at 13.8 Cr ⏫ by 150% YOY and down 👎 by 47% from H2 FY 25.

👉Expectation of revenue was more than 150 Cr since they had an order of agri spraying of 30 Lakh Acres from IFFCO, to be completed by Sep 30.

👉Per Acre Average Revenue is Rs. 500.

Profits at 1.01 Cr ⏫ by 158% YOY and down 👎 by 84% from H2FY 24.

English

@ImranMansuri313 Margins of the business are recovering, their average margins are 20-21%

English

IRIS

Multibagger potential 🔥

Sector : IT

Microcap ✅

Undervalued ✅

Super high growth ✅

Note : already 2X from the initial levels, since I am telling

English

𝗪𝗵𝗶𝗰𝗵 𝘀𝘁𝗼𝗰𝗸 𝗶𝘀 𝗴𝗶𝘃𝗶𝗻𝗴 𝘆𝗼𝘂 𝗺𝗮𝘅𝗶𝗺𝘂𝗺 𝗹𝗼𝘀𝘀 ?

Comment below 👇

English

@Chart_Wallah108 Sir plz ur view on

Drone destination plzz

English

𝗙𝗿𝗲𝗲 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗻𝗲𝘅𝘁 𝟯𝟬 𝗠𝗶𝗻𝘂𝘁𝗲𝘀 !

Ask any stock market query

Kindly 1 person - 1 query : )

Ask below 👇

English

Good #Q2FY25-23/10/24 from 5pm till 7pm

Manorama Industries

#Manorama

#ManoramaIndustries

Blockbuster Q2FY25 🔥 👏

Record rev, EBITDA, PBT and PAT

Highest ever numbers 🔥

New capacity is operational now and should help in similar growth

Rev at 195cr vs 117cr, Q1 at 133cr

PBT at 35cr vs 12c, almost 3x YoY, Q1 at 18cr

PAT at 27cr vs 9cr, Q1 at 13.5cr

OCF at 13cr vs -153cr

PNGS Gargi Fashion Jewellery

#PNGSGargi

Very good Q2FY25👏 with solid QoQ n YoY uptick adjusted for one time sales of Q1FY25

Rev at 23cr vs 10.7cr

PBT at 7cr vs 2.5cr

PAT at 5.1cr vs 1.7cr

OCF at 9.6cr vs -11.7cr

H1 FY25 rev at 34cr vs 17cr

Krystal Integrated Services

#Krystal

Rev at 266cr vs 234cr, Q1 at 257cr

PBT at 16.3cr vs 14.6cr, Q1 at 15.3cr

PAT at 15.1cr vs 11.8cr, Q1 at 14.3cr

H1 PAT at 30cr vs 20cr

Sona BLW Precision

#SonaComster

#SonaBLW

Good set, but very rich valuations

Rev at 922cr vs 787cr, Q1 at 891cr

Other income at 21cr vs 6cr

PBT at 202cr vs 170cr, Q1 at 189cr

PAT at 143cr vs 124cr,flat QoQ

Healthy orderbook

OCF at 466cr vs 300cr

TVS Holdings

#TVSHoldings

Rev at 11562cr vs 10619cr, Q1 at 10483cr

PBT at 901cr vs 727cr, Q1 at 732cr

PAT at 599cr vs 457cr, Q1 at 481cr

OCF at 1633cr

CARE Ratings

#CareRatings

Steady Q2FY25

Post CRISIL, now CARE delivers

Rev at 117cr vs 96cr, Q1 at 78cr

PBT at 64cr vs 50cr, Q1 at 30cr

PAT at 47cr vs 35cr, Q1 at 21cr

Jagsonpal Pharma

#JagsonPalPharma

Good Q2FY25

Rev at 75cr vs 57cr, Q1 at 61cr

PBT at 15.3cr vs 10cr, Q1 at 10cr

PAT at 11.4cr vs 7.4cr, Q1 at 5.3cr

OCF at 40cr vs 17cr

English

@ImranMansuri313 @nikeshyadva I am not a registered financial advisor.

However, i hold it in my portfolio and think it can create good returns from current levels over long term.

English

@vandit_jain1994 @nikeshyadva Sir fresh entry kar sakte he ??

Plz share view

English

Drone Destination 🚀 can be one such stock!

Itis expected to generate a revenue of more than 200 cr in FY 25, which is significantly higher than 31 Cr Revenue in FY 24.

👉This includes one large orders for agri spraying of 30 Lakh acres of land by IFFCO.

Per acre revenue is 500-600 Rs.

👉Hence, this order alone can generate more than 150 Cr revenue and this order is expected to be of recurring nature and its value is likely to be increased in coming years. 🎯

Disclosure: Invested.

English

@Chart_Wallah108 Sir plz share ur view

Drone destination

Felix industries

English

𝗙𝗿𝗲𝗲 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗻𝗲𝘅𝘁 𝟯𝟬 𝗠𝗶𝗻𝘂𝘁𝗲𝘀 !

Ask any stock market query

Kindly 1 person - 1 query : )

Ask below 👇

English

Good #Q2FY25-21/10/24 till 6pm

Cyient DLM

#CyientDLM

Decent set, rich valuations

Rev⏫33% at 389cr

EBITDA ⏫34.4% at 31.6cr

Rev at 389cr vs 291cr, Q1 at 258cr

PBT at 21cr vs 17.5cr adj for other income, Q1 at 12.4cr

PAT at 15.4cr vs 12.4cr, Q1 at 8.4cr

OCF at -19cr, flattish

Orderbook at 1980cr

Crown Lifters

#CrownLifters

Rev at 7.5cr vs 5.2cr,flat QoQ

PBT at 2.8cr vs 1cr, Q1 at 2.3cr

Solid margin expansion QoQ and YoY

OCF at 31cr vs 25cr

Solara Active Pharma Sciences

#Solara

Turnaround qtr on PBT and PAT front

Guidance for FY25 intact which means H2 should be stronger

Rev down sharply at 346cr vs 425cr

PBT at 8cr vs loss in last 2 comparable qtrs

PAT at 9.7cr vs loss in last 2 qtrs

OCF at 100cr vs 87cr

Swaraj Engines

#SwarajEngines

Good set, slightly above ests

Rev at 464cr vs 388cr, Q1 at 418cr

PBT at 61cr vs 50cr, Q1 at 58cr

PAT at 45cr vs 37cr, Q1 at 43cr

Good OCF

Vinyl Chemicals

#VinylChem

Struggle on topline continues, however margin expands well

Topline flat at 150cr vs 154cr

PBT at 7cr vs 5.3cr, Q1 at 6.7cr

PAT at 5cr vs 3.8cr, Q1 at 4.9cr

OCF at 31cr vs 14cr

PMC Fincorp

#PMCFin

Rev at 7cr vs 3.5cr, Q1 at 8cr

PBT at 6.4cr vs 2.7cr, Q1 at 7.3cr

Gravita

#Gravita

Looks decent mainly due to higher other income

Excluding other income, there is degrowth

Rev at 927cr vs 836cr, Q1 at 907cr

Other income at 40cr vs 14cr, Q1 at 7cr

PBT at 85cr vs 67cr, Q1 at 75cr

OCF at 66cr vs 26cr

Valuations are rich for these nos

Pondy oxides had much better and stellar all-time high Q2FY25

Bajaj Housing Finance

#BajHousingFin

Rich valns, decent growth

Rev at 2420cr vs 1911cr, Q1 at 2209cr

PBT at 708cr vs 575cr, Q1 at 630cr

PAT at 545cr vs 451cr, Q1 at 482cr

GNPA NNPA slightly higher

Decent:

#HFCL

Healthy orderbook, execution hasnt been great

Rev down

EBITDA ⏫16%

Small margin expansion

H2 probably will see decent execution uptick

English

@ArindamPramnk Sir short term me 2050 ya 2100 tak hold kar sakte he ??

Indonesia

✔️Vatech Wabag another 6% rally

My target of 2100 intact

✔️Neuland Labs 8% down somehow feel price action is telling something else may be top is in making will make analysis on this next week

✔️Sahasra SME 13% down today as expected after 55% rally from listing day

We sold and booked profit when it was 6% down

English

@Chart_Wallah108 Sir Shivalik bimetal and Interarch for short term?

English

𝗙𝗿𝗲𝗲 𝗳𝗼𝗿 𝘁𝗵𝗲 𝗻𝗲𝘅𝘁 𝟯𝟬 𝗠𝗶𝗻𝘂𝘁𝗲𝘀 !

Ask any stock market query

Kindly 1 person - 1 query : )

Ask below 👇

English