Sabitlenmiş Tweet

@WallStreetMav $VRT for cooling, $MU and $SNDK for memory , $PWR for power, $CRWD for cybersecurity $NVDA, TSM and $AVGO for the chips, $TSLA for the robots and $GOOG for the cloud

English

Ari.Is.Investing

2.6K posts

@InFoTheLongTerm

I analyse individual stocks, beat the S&P 500, no paywall. My five heaviest positions are $MU, $TSM, $VRT, $NVDA, and $NBIS. I favor AI, space, and robotics

Took a $QCOM position pre-earnings because the setup was favorable.. Stock at ~11x, sentiment anchored to “handsets are dead” while the real story = edge AI + NPUs was barely priced. market was treating it like a cyclical laggard, not a structural winner. that’s the mispricing I was buying.. Post-earnings? First validation, not the full one. they beat, margins held, and the stock ripped. That tells you positioning was wrong. But the guide was soft that’s the market saying “prove it” fair enough. So yea thesis partially played out. You got the re-rate from too cheap.. what hasn’t played out yet is the actual edge AI S-curve. that’s my real bet..

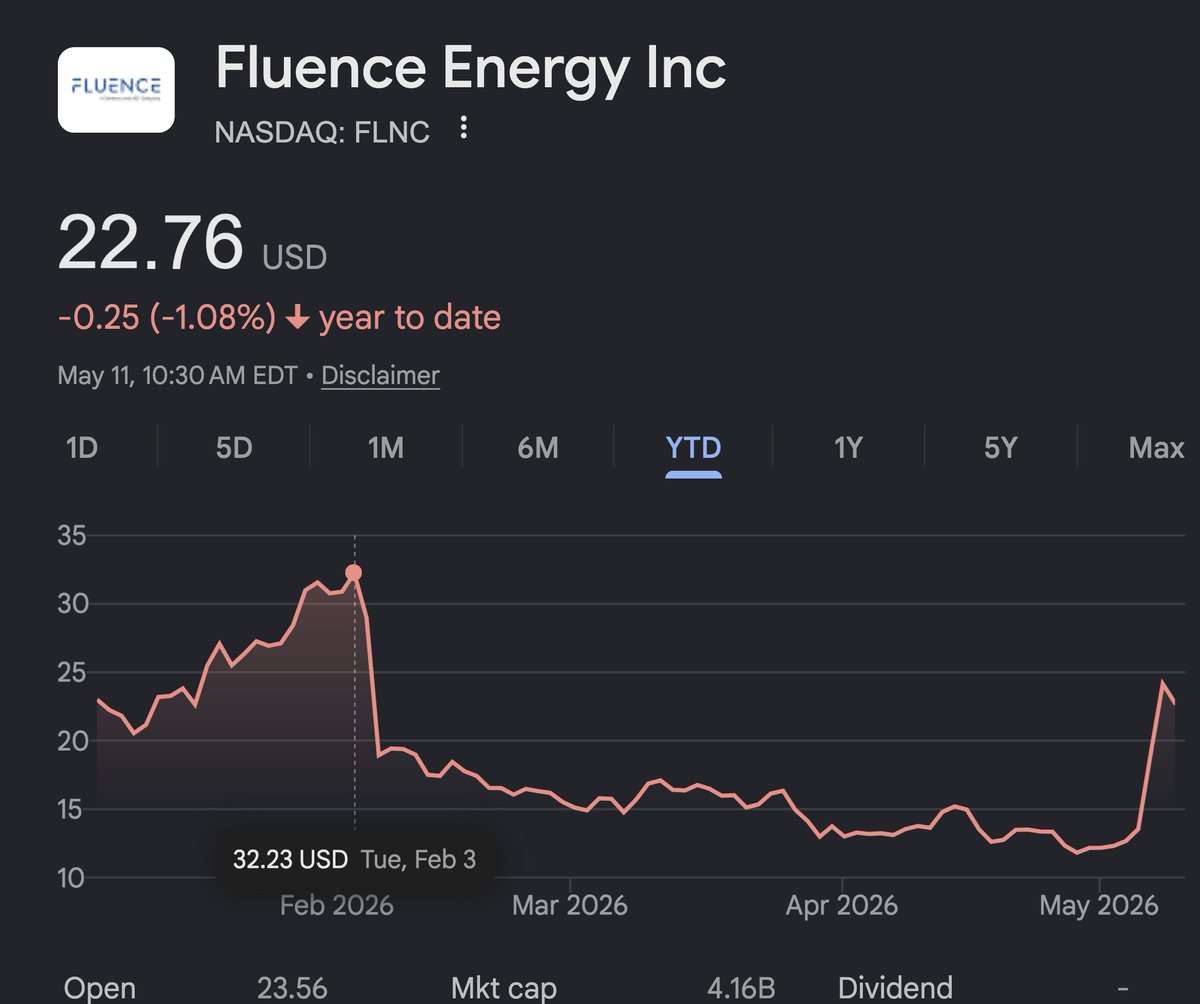

@aleabitoreddit @Jess252530 Buying the flnc dip as well

Posting this on a day where $OUST drops 16.6% to show my conviction: Some back of the napkin maths to get $OUST to be a 4x from my $23 average cost 👇 Assume $OUST hits $1B in revenue in 2030... that's a 42.5% CAGR from FY25 revenue. With that kind of revenue growth, and OpEx growing at 6%, the math points to EBITDA margins ~20% by 2030. That's $200M in EBITDA by 2030. Fwiw, some analysts are predicting 42% EBITDA margins by 2030 but that seems insane to me. Some analysts are very bad lol. $CGNX is doing ~$275M in EBITDA in FY26 growing EBITDA at 29%. They trade at 35x EBITDA. I'm happy to even go conservative here and take EBITDA down to 30x even if $OUST's growth rate is likely to be much higher. $200M * 30x = $6B (which is a 3x from today and a very conservative one). $200M * 40x = $8B (4x from today). I see us something in the middle of that in the next 3-4 years.