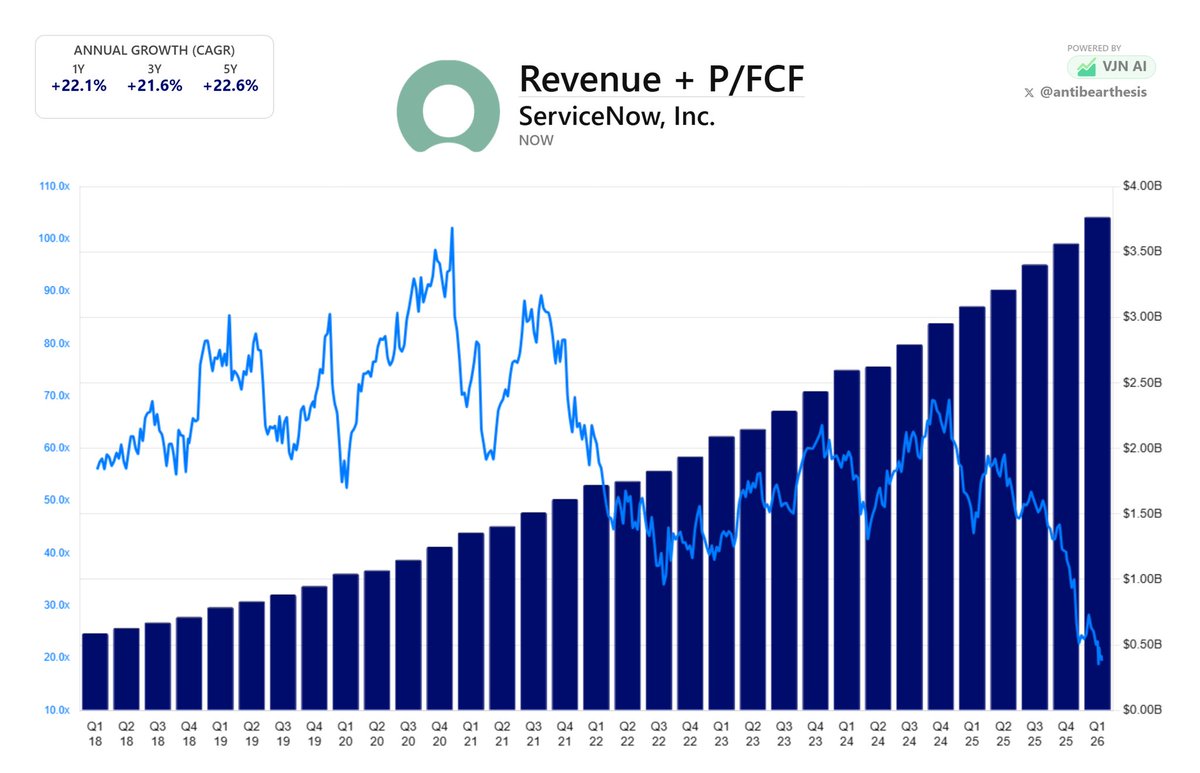

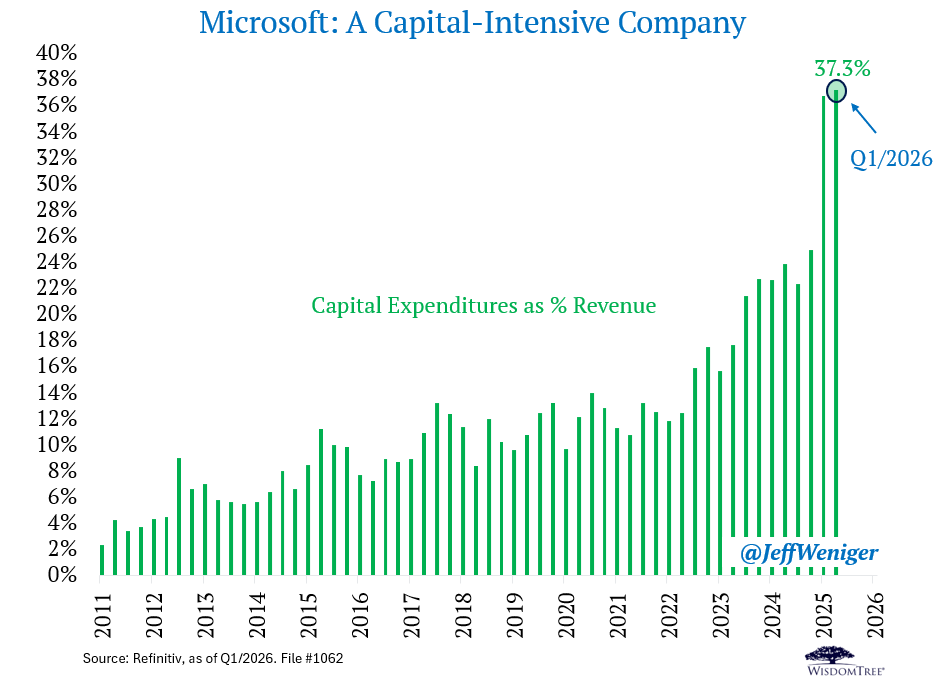

@JUST_KAWS $NOW is fundamentally strong and the fair value is well supported. Recently the fair value band declines slightly due to extensive capital spending.

English

Nick from The Inside Analyst

662 posts

@Inside_Analyst

Sanity-checking stocks through a structured Financial X-Ray. → Weekly insights + full access to S&P company analysis https://t.co/6gVVZKn8oM