Sabitlenmiş Tweet

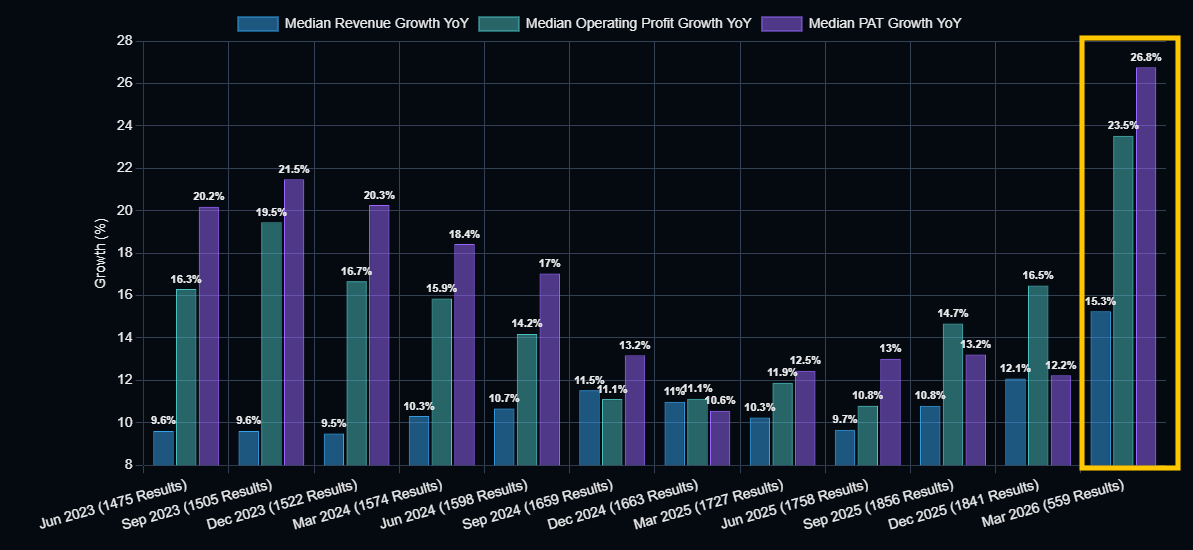

Result season so far looks Great.

Growth is primarily lead by-

🔷BFSI (Banking & NBFCs mainly SFBs and Mircofin) 🔥

🔷Infrastructure & Logistics

🔷Renewable Energy

🔷Specialty Chemicals & Metals

#EarningsSeason

English

Vaibhav Joshi

1.2K posts

@InvestWithJoshi

Everyone loves a stock after 5x. I like businesses before they become Twitter threads. 💻 Dev by profession | Investor 💰

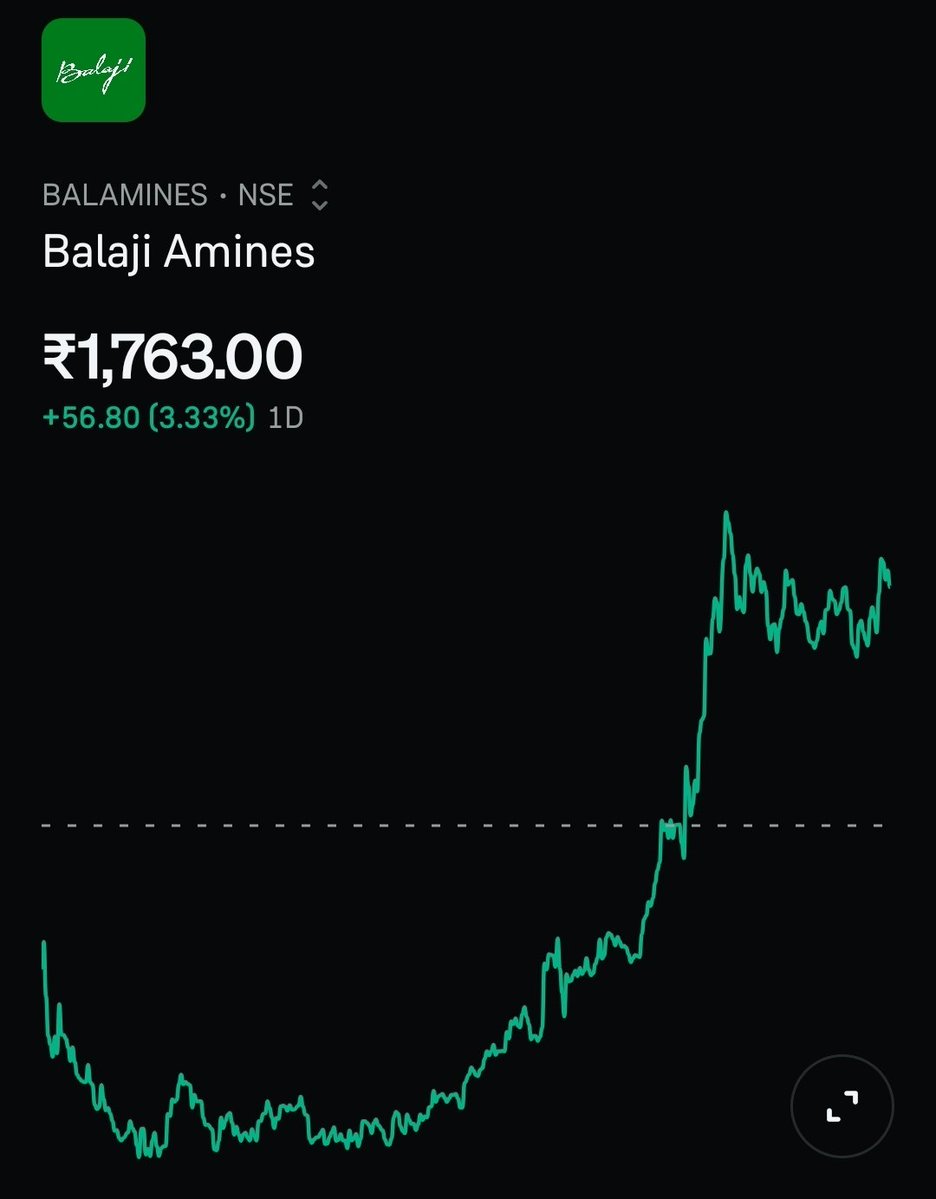

Keep a close watch on speciality Chemical 👀 looks like a start of an upcycle.

Regime change in West Bengal will benifit Baazar Style 🔥🔥

One thing I’ve realized in investing is that sometimes 2 companies can operate in the exact same sector… but management quality and expectation setting changes everything 👀 Best example right now is Kaynes Technology vs Avalon Technologies Both are riding India’s EMS manufacturing boom. Both are exposed to themes like railways, EVs, aerospace, industrial electronics and import substitution. But the market is treating them very differently now. Kaynes came into FY26 with massive hype. Management guided for around ₹4500 crore revenue which meant 50%+ growth. The market got excited and priced the stock like nothing could go wrong. Then reality kicked in. Railway approvals got delayed. Smart meter execution slowed. Working capital stretched. Guidance first got revised to ₹4100 crore and even that eventually got missed. Final FY26 revenue came around ₹3626 crore. That’s almost ₹900 crore lower than the original target. And when a stock is priced for perfection, these misses hurt badly. The stock corrected almost 48% from peak levels. Now look at Avalon. Completely different vibe. Management stayed conservative. No flashy promises. No unrealistic projections. Just steady execution quarter after quarter. And the market rewarded that consistency. The stock quietly delivered more than 54% returns in the last 1 year while sentiment around many EMS names remained weak 📈 What’s interesting is that I still think Kaynes can become a much bigger company over the next decade because the opportunity size in Indian electronics manufacturing is enormous. India is still in the early innings of EMS growth. But this phase is teaching an important lesson: Growth alone is not enough. Expectation management matters just as much. Right now Avalon feels like the steadier compounder while Kaynes feels more like a high beta execution story. And honestly… some of the best compounders are usually the companies quietly delivering numbers instead of aggressively selling future dreams.