Anurag Singh retweetledi

Risk in the market is not about losing money. The real risk is time frame.

Pure gold from Madhusudan jee 🔥

English

Anurag Singh

170 posts

@Investosphere21

Spirituality and Long Term Investing

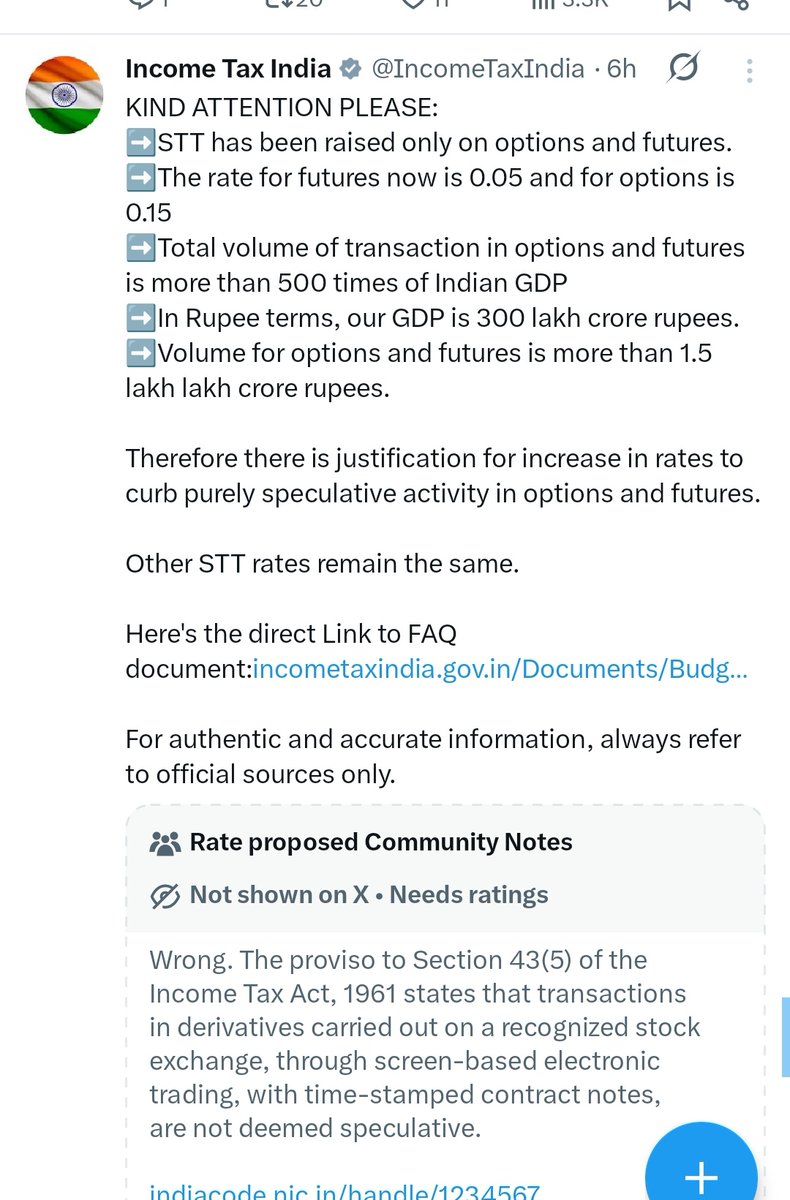

STT Hike Explained: How Much Will Trading Really Cost? 📊 After the STT hike, many investors & traders are confused about how taxation impacts market profits. 🔹 What is STT? STT (Securities Transaction Tax) is charged on the transaction value (sell value) - not on profit. New STT Rate - 🔹 Futures Trading Impact If a futures contract value is ₹10,000: Earlier STT @ 0.02% = ₹2 New STT @ 0.05% = ₹5 ➡️ Extra cost = ₹3 per trade 🔹 Options Trading Impact If option premium is ₹10,000: Earlier STT @ 0.10% = ₹10 New STT @ 0.15% = ₹15 ➡️ Extra cost = ₹5 per trade 🔹 Key Takeaways ❌ STT is not charged on profit 📉 Intraday, F&O & high-frequency traders are hit more 📈 Long-term investors face limited impact. Higher STT = higher churn cost. The more you trade, the more it pinches. This isn’t a marginal adjustment - it’s a liquidity shock. F&O costs jump meaningfully, hedging becomes less viable and participation is set to decline. #STT #StockMarket #TradingCosts #Budget

STT Hike Explained: How Much Will Trading Really Cost? 📊 After the STT hike, many investors & traders are confused about how taxation impacts market profits. 🔹 What is STT? STT (Securities Transaction Tax) is charged on the transaction value (sell value) - not on profit. New STT Rate - 🔹 Futures Trading Impact If a futures contract value is ₹10,000: Earlier STT @ 0.02% = ₹2 New STT @ 0.05% = ₹5 ➡️ Extra cost = ₹3 per trade 🔹 Options Trading Impact If option premium is ₹10,000: Earlier STT @ 0.10% = ₹10 New STT @ 0.15% = ₹15 ➡️ Extra cost = ₹5 per trade 🔹 Key Takeaways ❌ STT is not charged on profit 📉 Intraday, F&O & high-frequency traders are hit more 📈 Long-term investors face limited impact. Higher STT = higher churn cost. The more you trade, the more it pinches. This isn’t a marginal adjustment - it’s a liquidity shock. F&O costs jump meaningfully, hedging becomes less viable and participation is set to decline. #STT #StockMarket #TradingCosts #Budget

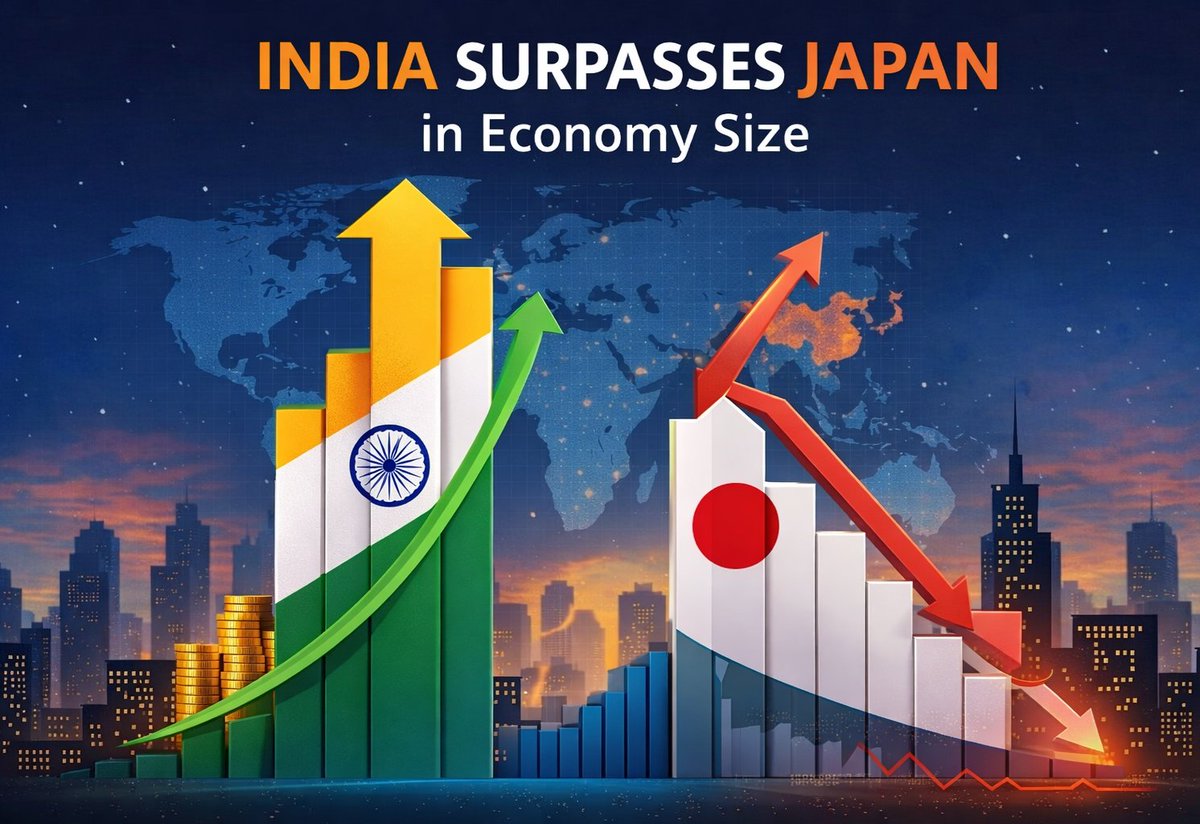

🇮🇳 “India could be the world’s No.1 economy in your lifetime.” - David Rubenstein (@CarlyleGroup) Despite: • Current market correction 📉 • FII outflows • Rising geopolitical tensions 🌍 India’s long-term story remains intact - driven by demographics, reforms & growth potential. Volatility is temporary. Structural growth isn’t. #India #IndianEconomy #Investing

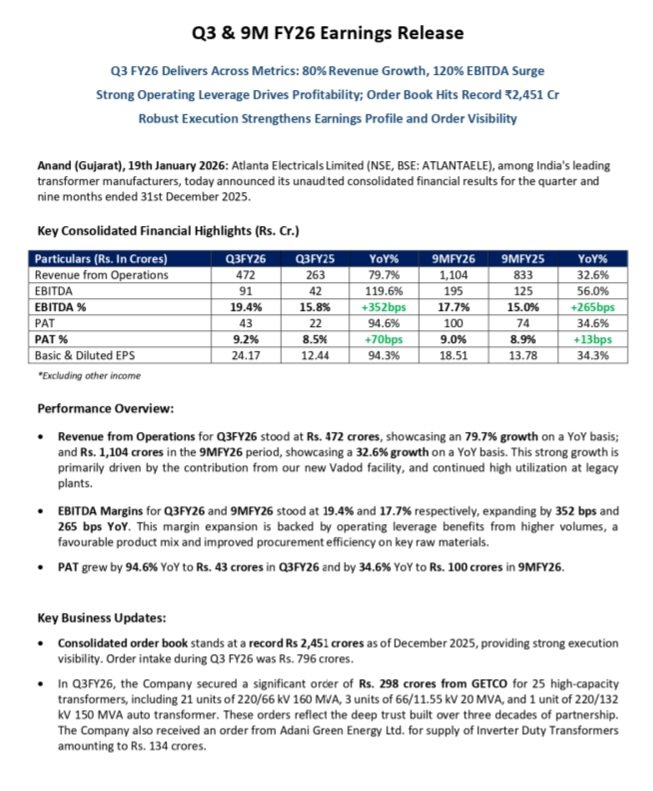

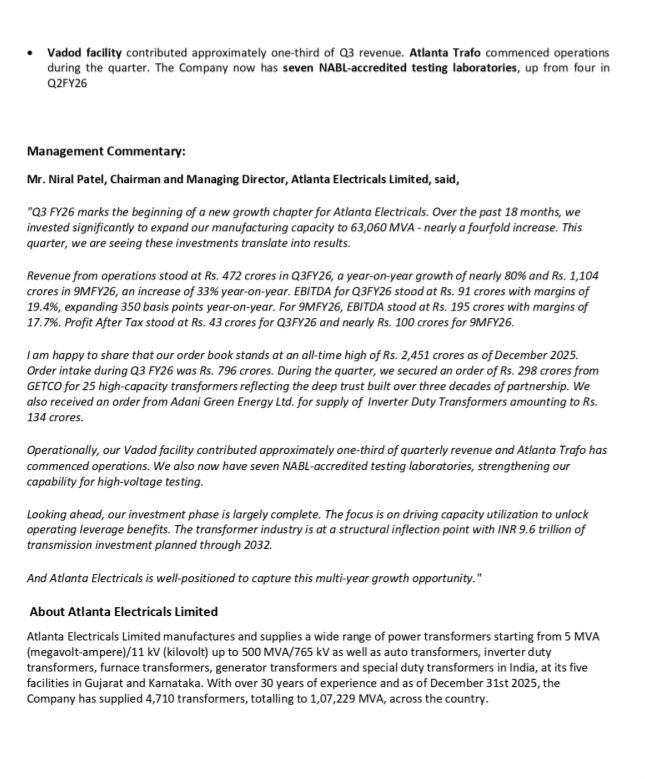

STOCK STUDY Atlanta Electricals Ltd CMP: 871 | Mcap: 6,700 Cr 🔹 Overview - • One of the India’s fastest-growing transformer manufacturers • Capacity: 63,060 MVA across 5 plants • Supplies to 19 states + 3 UTs • Capability up to 500 MVA / 765 kV (post Vadod expansion) 🔹 Growth Drivers - • 4.25 lakh cr T&D capex till FY27 • 500 GW renewable target, huge inverter/auto transformer demand • Railways, EV charging infra & data centers driving new demand • Strong order book: 2069 Cr • Specialty transformers (furnace/rectifier) growing fastest 🔹 Financials (Q-2 FY-26) - • Revenue: 317 Cr • EBITDA Margin: 18% • PAT: 30 Cr | EPS: 3.93 • ROE: 40.8% | ROCE: 50.2% • P/E: 54.9 (premium for high growth) 🔹 Shareholding - • Promoters: 87.28% • FII: 2.19% | DII: 3.86% 🔹 Key Updates - Capacity, Plants & Expansion - • Total capacity: 63,060 MVA - among India’s largest. • BTW acquisition + Vadod facility enable 400 kV & 765 kV capability • BTW alone can generate 600-700 Cr revenue at full utilization. • New IDT plant (65 Cr capex) to be completed in 9 months, adds 5,000 MVA dedicated solar capability. • IPO (Sept 2025) listed strong • Backward integration to lift margins • Targeting export markets 🔹 Verdict (My View) - A high-quality T&D + renewable play with strong execution, margin expansion, and multi-year visibility. If growth sustains, Atlanta can potentially scale to 50k Cr market cap over 5-7 years. Disclaimer: This post is for information only and is not investment advice. #Atlanta #AtlantaElectricals #Transformers