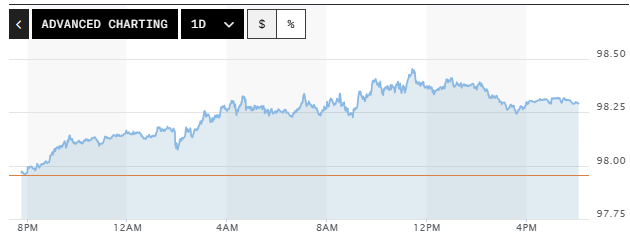

Bond yields lifted, a headwind for equities, US: S&P500 -1.24%, Nasdaq -1.54%. Europe/UK: Stoxx -1.81%, Nasdaq -1.71%. $AUDUSD fell to 0.7150. US 2yr yld +5bps to 4.07%, 10yr +11bps to 4.59%.

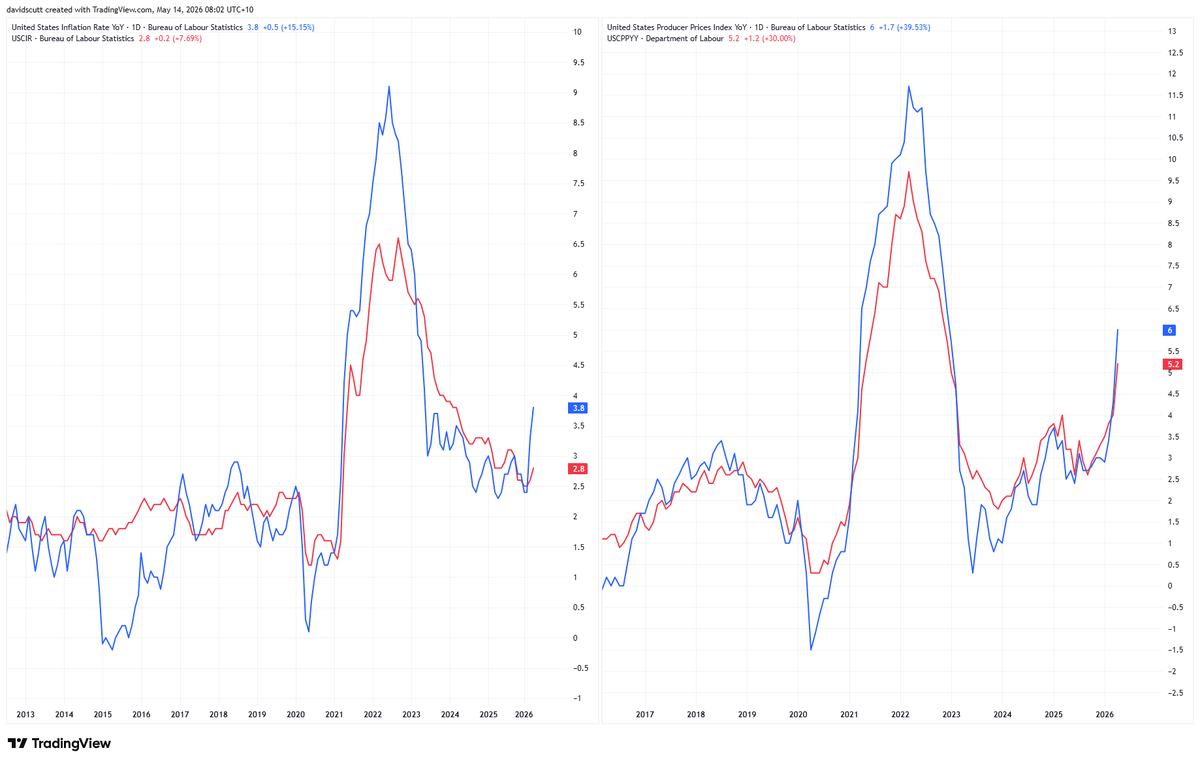

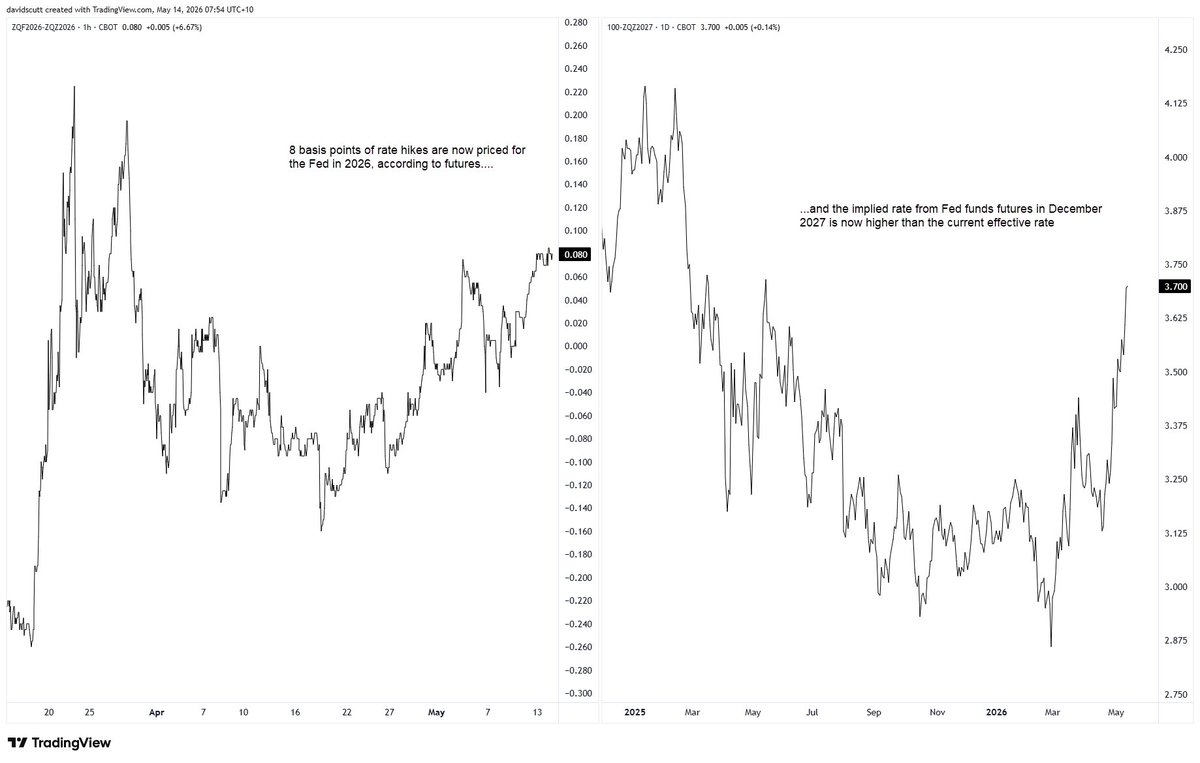

Look at those upstream price pressures heading the way of the US consumer. Notable Fed funds futures have now effectively priced out cuts throughout this year AND next. Volumes may be pitiful that far out, but good luck to Warsh in trying to push for easier policy.

US PPI Final Demand (M/M) Apr: 1.4% (est 0.5%; prev 0.5%; prev R 0.7%)

- PPI Final Demand (Y/Y): 6.0% (est 4.8%; prev 4.0%; prev R 4.3%)

- PPI Ex Food And Energy (M/M): 1.0% (est 0.3%; prev 0.1%; prev R 0.2%)

- PPI Ex Food And Energy (Y/Y): 5.2% (est 4.3%; prev 3.8%; prev R 4.0%)

- PPI Ex Food, Energy And Trade (M/M): 5.2% (est 0.3%; prev 0.1%)

- PPI Ex Food, Energy And Trade (Y/Y): 4.4% (est 4.1%; prev 3.6%)

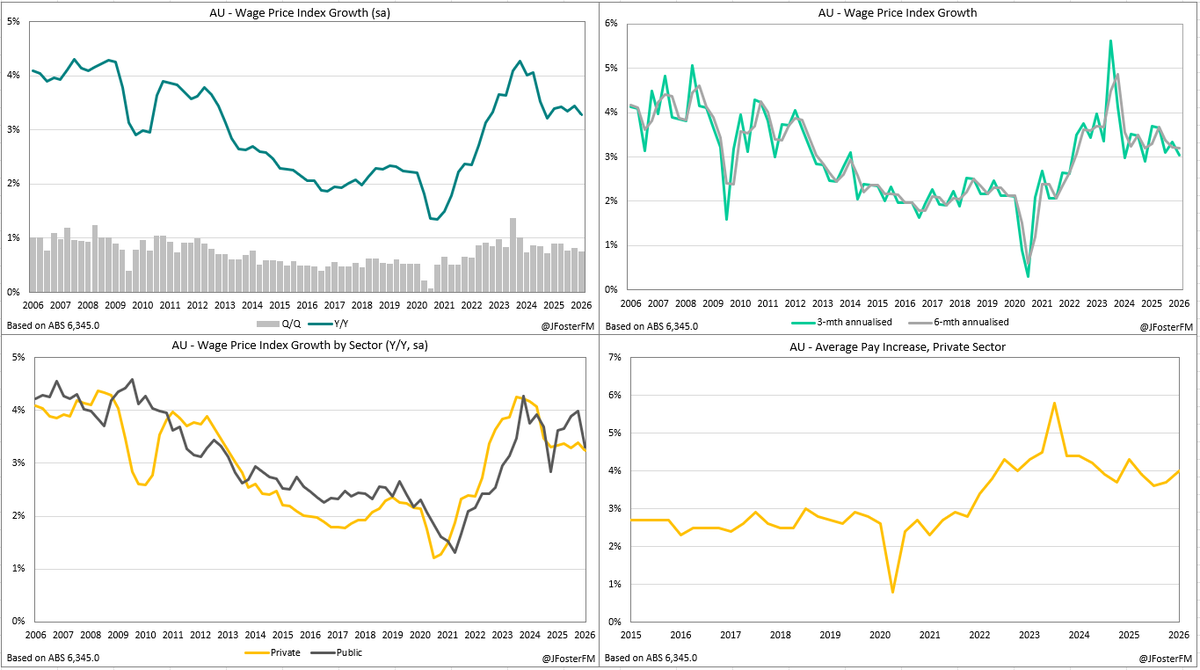

🇦🇺 Wages growth was 0.8% in the March quarter, same as in the December quarter. Annual growth slows from 3.4% to 3.3%.

- Private sector 0.8%qq, 3.2%yy (from 3.4%)

- Public sector 0.5%qq, 3.3%yy (from 4%)

#ausbiz

The "Liz Truss moment" of 2022 has turned into the UK's political reality, with 30-year yields soaring to their highest levels since 1998 and the pound weakening. "No matter who is in power, no matter their political leaning, there does not appear to be a credible plan to restore the country’s finances." bloomberg.com/news/articles/…

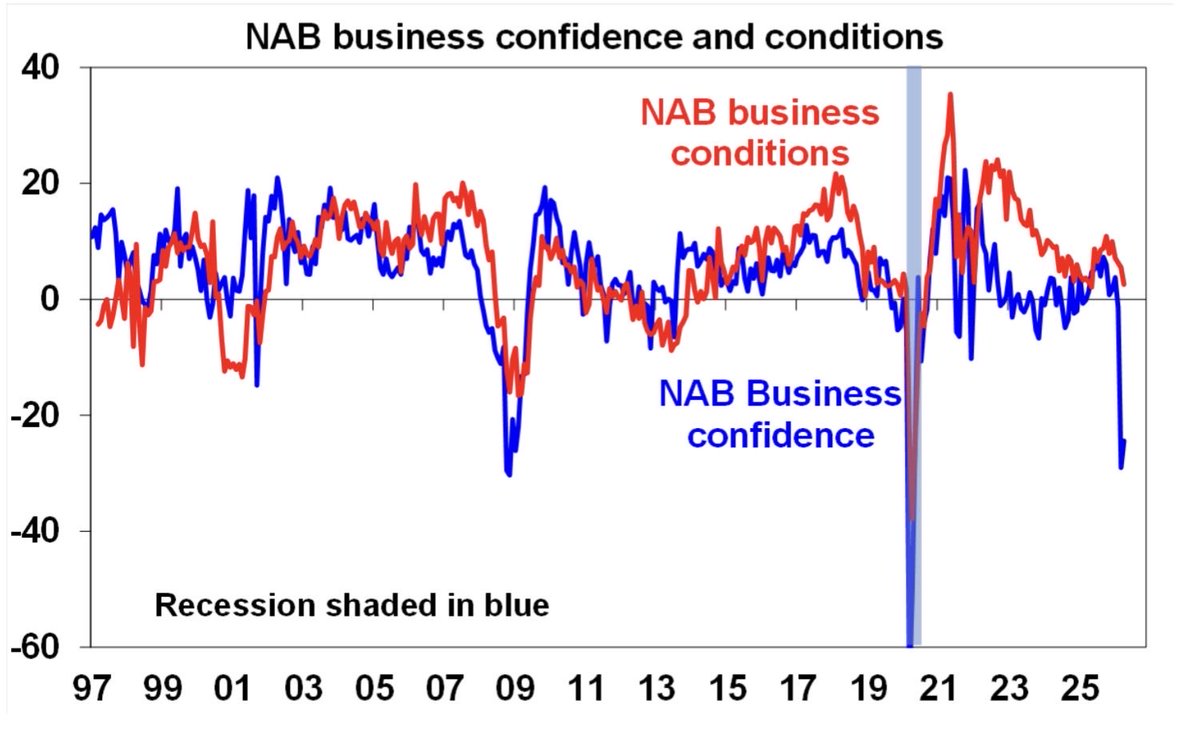

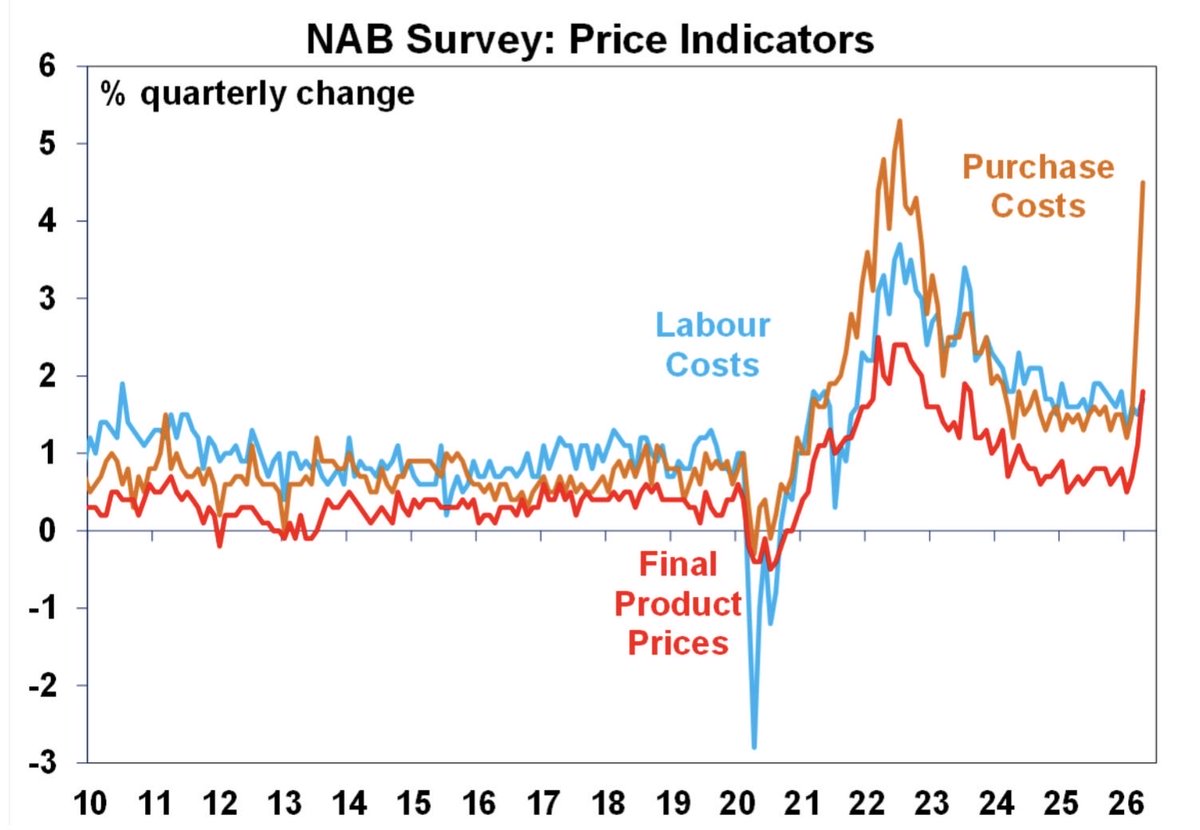

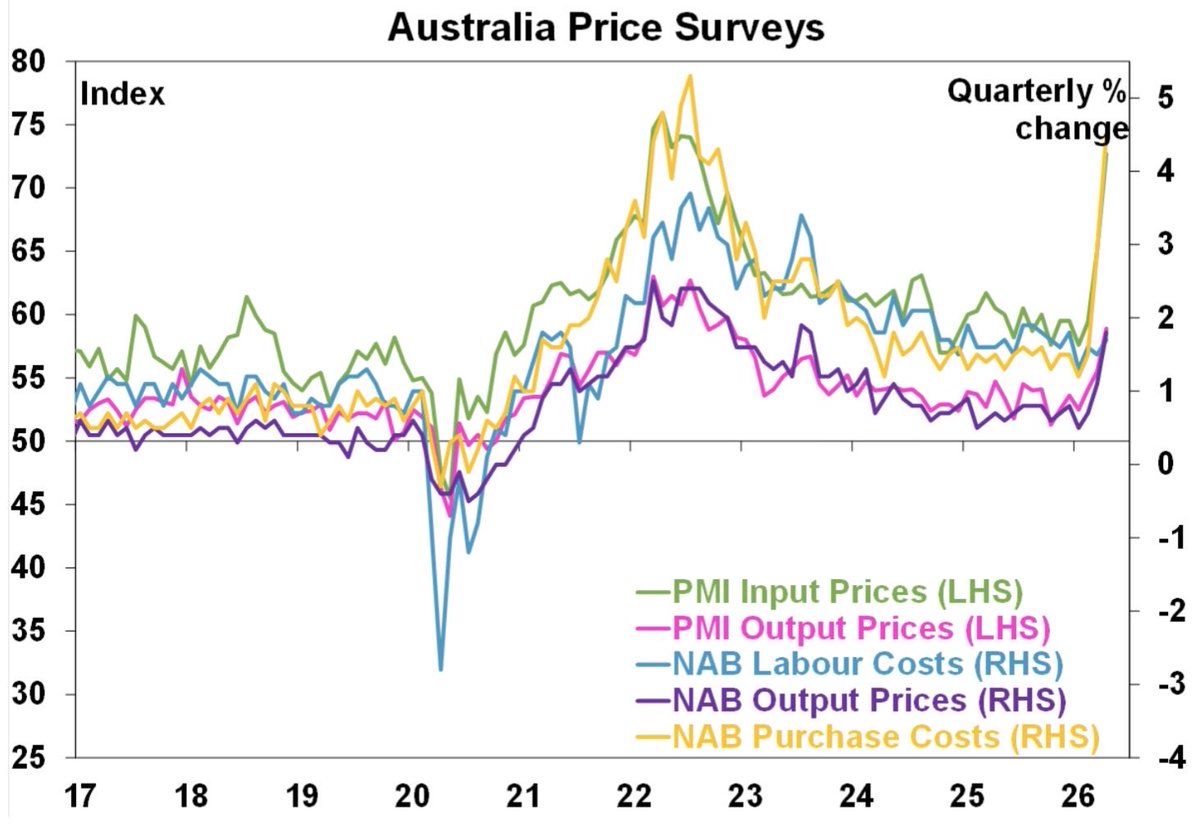

NAB April business survey not looking so good

Conditions fell only a bit to +3, but new orders fell to -5 & emp to just +1.

Confidence also remained very weak at -24.

Price pressures rose further (like PMI survey).

All up continuing to warn of a mild bout of stagflation.