JPPY retweetledi

JPPY

6.5K posts

JPPY retweetledi

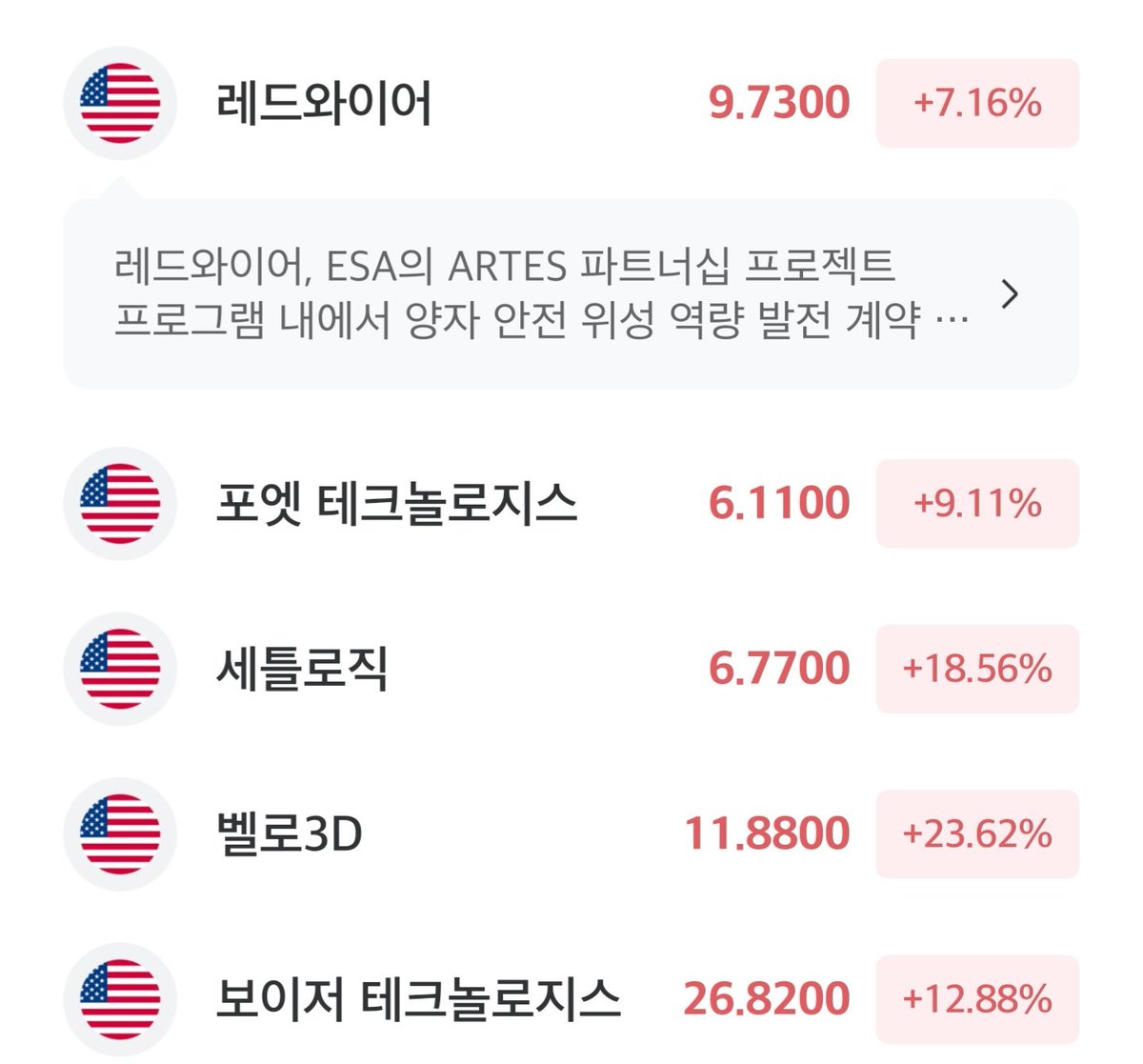

$VELO +23.62%

One thing a lot of new investors may not be aware of is that Musk/SpaceX were interested in acquiring Velo3D back in 2021, but the company chose not to sell.

The CEO at the time rejected the offer. Instead of an acquisition, SpaceX became a major customer and close partner, using Velo3D’s Sapphire machines to manufacture parts for its Raptor engines, including the latest Raptor 3.

This wasn’t a small relationship either. SpaceX started with a single machine in 2018 and scaled to 22 systems by 2021. Today, they operate around 25 machines and continue to expand their usage.

When one of the most advanced engineering organizations in the world tries to acquire you, gets turned down, and then keeps buying your machines anyway, that says a lot about the quality of the product.

English

JPPY retweetledi

JPPY retweetledi

$VELO: 2025 10K was filed this morning.

* Named customer relationships include RTX Corporation, Honeywell International, Lockheed Martin, Ursa Major Technologies, Vast Space, Avio, and Lam Research. Over 50% of customers own multiple Sapphire systems. 126+ total systems shipped as of 12/31/25.

* SpaceX (largest customer) and expected to remain an important relationship going forward - driven by timing of its major orders for 3d Printer and parts.

* Bookings nearly doubled in one year: $59M in 2025 vs $31M in 2024 (a 90% jump). Backlog doubled too ($31M vs $16M). Book-to-bill ratio is running well above 1.0x, meaning demand is outpacing recognized revenue.

* 26% organic revenue growth in 2025: Headline says +12.1%, but 2024 included a one-time $5M SpaceX IP licensing payment. Strip that out and core revenue grew $9.4M or 26.1%. 3D Printer and parts revenue specifically grew 54.5% YoY ($39.2M vs $25.4M).

* Defense now 56% of revenue (hypersonics, munitions, propulsion): The 10-K explicitly calls out active DoD engagements across munitions and munition support components, hypersonic propulsion, thermal management systems, and aerospace propulsion. With U.S. military branches (Navy, Army, Air Force) named as customers, and the Iran conflict explicitly flagged as a potential demand accelerant. "We may experience increased demand for our additive manufacturing solutions from government and defense customers" given active DoD support for "munitions and munition support components, hypersonic propulsion and thermal management systems, and aerospace propulsion."

* Company guides for gross margin improvement in H2 2026: Direct quote from the MD&A: "We expect to accelerate production cycle times and further improving efficiencies on the production floor to lower our cost of revenue, which we expect will improve our gross profit and gross margins in the second half of 2026." Gross margin was -16.1% in 2025, heavily burdened by RPS ramp costs and $7M of inventory write-offs.

*57 issued patents, earliest expiring 2035: 45 U.S. + 12 foreign issued patents, 34 pending applications. Earliest expiry is 2035, latest 2047.

*RPS is the new growth engine (low capital entry for DoD customers): Rapid Production Solutions lets customers access Velo3D manufacturing without buying a printer. This lowers adoption friction for defense programs with slow procurement cycles, while Velo3D captures recurring parts revenue. Management is monitoring RPS as a separate segment and will expand segment reporting in 2026, a signal the business line is material enough to break out.

ir.velo3d.com/sec-filings/al…

English

$velo

내가 계속 이놈에 소금이 보다 애정이 가는이유

국방부 계약이 꾸준히 늘어남

재정적 리스크를 감안하고 베팅

우주와 국방이 더해지면 지금 가격은 지하실 바닥이겠지

Arun Jeldi@AJeldi2

한국어

세틀 또 다시 유증

이런 소형주는 늘 유증을 조심해야함

내가 현재 들고 있고, x 에서 핫한 $satl $velo $poet

모두 유증으로 인한 주가 등락폭이 매우심함

velo 엑친님의 말을 빌리면 정부대출을 알아본다고 하나

유증의 옵션이 아직 살아있음

치보님, 무니님이나 이런 소형종목은 소액으로 접근하자고 하나

한국사람 전투민족 성향상 대부분 본인 투자자산의 몇프로 보단 50%이상 100%까지 올인함

특히 소액, 1억 미만의 투자자들은 분산 투자 보단 한방을 노리기에 이런 종목들에 올인함

본인의 자산 증식에 이만큼 베팅을 할 수 있는 종목도 몇 안되기에 그마음이 이해가감

등락폭을 버틸 수 있는 분들은 감내하셔서 큰 수익

야수모드 감자🛰@skrr_potato

$SATL 5천만달러치 유증...? satellogic.gcs-web.com/node/9081/html

한국어

JPPY retweetledi

지지대 없이 날아오르는 금속 부품 — Velo3D $VELO 가 여는 ‘제조 불가능’ 시대

2025년 말 Velo3D의 backlog은 3,100만 달러로 전년 대비 94% 증가했다. 동시에 RPS(Rapid Production Solutions, 고객 대신 부품을 직접 생산해 주는 서비스) 비중이 빠르게 올라가고 있다는 사실이 실적 발표를 통해 드러났다. 시장은 여전히 이 회사를 ‘고변동성 적자 하드웨어 판매사’로 분류하지만, 실제로는 Intelligent Fusion 기술이 기존 CNC 가공과 주조 공정의 물리적 한계를 한 번에 뛰어넘으면서 ‘제조할 수 없었던 영역’ 자체를 새로 열고 있다. 이 기술이 단순한 3D 프린팅 업그레이드가 아니라 제조 패러다임의 전환점이라는 점이, 지금 Velo3D를 둘러싼 가장 강한 긴장이다.

Sapphire 프린터, Flow 지능형 준비 소프트웨어, Assure 실시간 품질 보증 소프트웨어가 하나의 패키지로 통합된 이유는 명확하다. 개별 장비를 팔던 시대에서 벗어나 고객이 원하는 복잡한 금속 부품을 처음부터 끝까지 책임지기 위해서다. Flow는 설계 데이터를 받아 자동으로 최적 프린트 경로를 계산하고, Assure는 레이저가 금속 분말을 녹이는 순간마다 1,000분의 1초 단위로 데이터를 기록한다. 이 세 요소가 실시간으로 피드백을 주고받는 구조가 Intelligent Fusion의 핵심이다. 결과적으로 프린터가 단순한 ‘도구’가 아니라 ‘지능을 가진 제조 시스템’으로 진화한다.

그 지능이 가장 극적으로 드러나는 부분은 SupportFree 기술이다. 기존 레이저 파우더 베드 퓨전(LPBF) 방식에서는 복잡한 내부 구조를 만들 때 반드시 지지대(support structure)가 필요했다. 지지대는 부품을 고정하고 열 변형을 막아주지만, 완성 후 제거 과정에서 시간과 비용이 폭발적으로 증가하고, 제거 흔적이 남아 정밀도가 떨어지는 치명적인 단점이 있었다. Velo3D는 Intelligent Fusion 프로세스를 통해 지지대를 아예 없애는 데 성공했다. 소프트웨어가 레이저 출력, 스캔 속도, 냉각 속도를 부품 형상마다 실시간으로 조정하면서 열 응력을 스스로 제어하는 방식이다. 쉽게 말해, 금속이 녹아 굳는 순간의 물리학을 예측하고 조작해 ‘공중에 떠 있는’ 구조를 안정적으로 쌓아 올리는 것이다. 이 기술 덕분에 항공우주용 연료 분사기 내부의 미세 유로, 국방용 Ground Vehicle의 복잡한 냉각 채널, 에너지 분야 초고압 밸브 같은 부품이 기존 방식으로는 불가능했던 속도와 비용으로 제작된다.

이 변화가 왜 중요한가. 기존 제조에서는 ‘복잡하면 비싸지고, 비싸지면 포기한다’는 공식이 지배적이었다. CNC는 5축 이상 가공이 필요하고 주조는 금형 비용이 천문학적이며, 둘 다 설계 자유도가 극도로 제한된다. Velo3D의 SupportFree는 그 공식을 깨뜨린다. 부품 무게를 30~50% 줄이면서도 강도를 유지하거나, 내부에 기존에는 만들 수 없었던 미세 냉각 채널을 새기는 것이 가능해진다. 결과적으로 항공우주·국방·에너지 분야에서 ‘미션 크리티컬’이라고 불리는 부품 시장 전체가 확대된다. 기존 점유율을 뺏는 경쟁이 아니라, 아예 새로운 시장을 창출하는 기술이다.

사업 모델도 이 기술을 따라 움직이고 있다. 과거에는 Sapphire시스템을 한 대 팔고 끝이었지만, 이제는 RPS로 고객에게 “부품을 대신 만들어 드리겠다”고 제안한다. RPS는 단순 아웃소싱이 아니다. Velo3D가 프린터를 고객 공장에 설치하고, 실시간 데이터를 모아 Assure로 품질을 보증하며, 반복 생산까지 책임진다. 매출 믹스에서 RPS 비중이 올라갈수록 recurring revenue가 늘어나고, 동시에 140대 현장 프린터 플릿에서 쌓이는 생산 데이터가 ‘디지털 매뉴팩처링 인텔리전스 플랫폼’으로 진화한다. 이 데이터는 다음 설계의 최적화에 바로 투입되며, 고객 입장에서는 전환 비용이 극도로 높아지는 lock-in 효과를 만든다. 기술이 단순한 하드웨어에서 소프트웨어·데이터 생태계로 확대되는 순간이다.

여기에 미국 중심의 규제·공급망 해자가 더해진다. Velo3D는 ITAR(국제무기거래규정)과 DoD 인증을 통과한 미국 유일의 대형 LPBF OEM이다. 2026년 NDAA(국가방위수권법)에서 중국·러시아산 AM 시스템 사용을 제한하는 조항은 Velo3D에게 구조적 우위를 제공한다. DoD Project FORGE(3,260만 달러)와 미 육군 Ground Vehicle Systems Center의 AM 벤더 자격은 단순 수주가 아니라, 기술이 국가 안보 공급망의 일부가 되었음을 의미한다. 기술 우위와 규제 우위가 결합되면서 경쟁사(EOS, Nikon SLM, Colibrium Additive)가 규모나 소재에서는 앞서더라도, 미션 크리티컬 + 방산 niche에서는 따라오기 어려운 구조가 완성된다.

물론 기술이 아무리 뛰어나도 실행이 증명되지 않으면 시장은 믿지 않는다. 2025년 gross margin이 -16.1%였고 Q4에 700만 달러 규모 재고 폐기가 발생한 것은 사실이다. RPS ramp-up 속도와 H2 2026 gross margin 30% 달성 여부가 아직 미해소된 변수다. 그러나 Intelligent Fusion이 실제 부품 시장을 확대하고 RPS가 recurring 기반을 강화하는 인과 관계는 이미 실적 숫자 속에 드러나고 있다. 현재 주가가 리버스 DCF 기준으로 요구하는 19.01% CAGR는, 기술이 창출하는 새로운 TAM과 데이터 플랫폼 잠재력을 고려하면 과소평가된 수준으로 보인다.

결국 Velo3D의 Intelligent Fusion은 아직 ‘미래 기술’이 아니라 현재 진행 중인 제조 혁명이다. 지지대 없이도 안정적으로 쌓아 올리는 금속 부품이 실제로 날아오르고 있고, 그 부품이 항공기와 전투차량과 발전소에 들어가는 순간, 기존 제조의 벽은 이미 한 조각씩 무너지고 있다.

$VELO

한국어

JPPY retweetledi

$VELO – New stock, holding for medium-term.

The U.S. defense industrial base has a manufacturing problem. It was built for a Cold War‑era pace of production, not for speed or flexibility.

Producing complex metal parts for missiles, aircraft, ships, and other critical systems still depends on traditional methods like casting and forging. These processes require custom tooling, specialized suppliers, and long lead times that can stretch into many months. In many defense programs, strict approval requirements and limited supplier capacity push timelines even further.

The Department of Defense has publicly acknowledged that current supply chains are not responsive enough for modern warfare.

Additive manufacturing directly targets this constraint by eliminating the need for custom tooling and enabling parts to be produced directly, compressing production timelines from months to weeks.

But speed alone is not sufficient. For a part to actually enter production and be used in defense or aerospace systems, it must go through a formal qualification process that proves it meets performance and reliability standards. That qualification is the core barrier to adoption.

Velo3D builds industrial metal 3D printers that manufacture parts that are impractical or uneconomical to produce with traditional methods.

Their core system, the Sapphire platform, uses high‑powered lasers to print metal parts layer by layer. What sets it apart is the ability to handle highly complex geometries, including internal channels and overhanging structures, without the extensive support structures other metal printers require. This makes it relevant to aerospace and defense, where the most valuable parts are also the most geometrically complex.

All Sapphire printers are assembled in the United States and meet Department of Defense cybersecurity standards, including secure network compliance that allows connection to military systems. This domestic build and security compliance are material competitive advantages given U.S. policy and procurement rules.

The FY2026 National Defense Authorization Act formally designates additive manufacturing as critical national security infrastructure. It also implements procurement restrictions that prohibit the Department of Defense and its contractors from using 3D printing equipment made in or connected through China, Russia, Iran, or North Korea. These provisions create a legal competitive barrier that excludes major foreign suppliers from defense programs, narrowing the field of eligible additive manufacturing vendors.

That regulatory backdrop matters because it positions Velo3D to win real production/government work/contracts.

Velo3D has already secured multiple U.S. defense and government contracts that reflect this shift.

> In late 2025, the company won a $32.6 million contract under the U.S. Defense Innovation Unit’s Project FORGE, aimed at prototyping and qualifying additively manufactured components to eliminate bottlenecks in critical weapons system programs. The contract includes collaboration with the U.S. Navy and a major defense prime contractor to qualify components that can scale production rates for key systems.

> In early 2026, Velo3D secured an $11.5 million full‑rate production contract from a key U.S. defense prime contractor for a sensitive national security program. Full‑rate production means a customer has cleared qualification and is ordering at volume.

> Also in 2026, Velo3D was selected as the first qualified additive manufacturing vendor for the U.S. Army’s Ground Vehicle Systems Center, meeting all qualification criteria under a Cooperative Research & Development Agreement. This opens the Army’s ground vehicle supply chain as a new category with long‑term parts demand requiring qualified additive solutions.

+ Velo3D participates in collaborations with the Navy and other defense partners to advance advanced materials and additive manufacturing applications for flight and mission‑critical systems.

Qualification is the moat and the most important concept in this thesis. Before any component can be used in a defense or aerospace program, both the part design and the process that made it must be formally qualified. That process is expensive, slow, and technically rigorous. Once Velo3D’s platform is qualified for a specific part on a specific program, that position stays locked in for the life of the program. Defense programs often run for decades. Switching to a different manufacturer means restarting qualification from scratch.

The moat also rests on the integrated system. The combination of proprietary hardware, process control software, and quality assurance creates a level of repeatability that matters deeply to defense and aerospace customers. Printing one part on a good machine is straightforward. Printing hundreds of identical parts across multiple machines and locations that all meet the same specification is not. Velo3D’s system is built for that level of industrial reliability.

That moat is great but not invulnerable. Larger competitors including EOS and Nikon AM via Morf3D are investing in similar capabilities, and new domestic players may emerge. Velo3D’s edge is that it focused earlier and more narrowly on the hardest problems in aerospace and defense and built production qualifications others have not yet matched. Competitors could close this gap over time.

Note that revenue is lumpy because large system sales and government contract timing swing quarterly results.

The Bottom Line:

The core thesis is straightforward and backed by explicit CEO confirmation.

The U.S. government has identified domestic metal additive manufacturing as critical national security infrastructure and enacted procurement restrictions that exclude major foreign competitors. It is actively contracting with Velo3D to solve defense supply chain bottlenecks treated as urgent.

Crucially, the company’s CEO has publicly confirmed that Velo3D prints five major metal components that are specifically qualified for SpaceX’s Raptor engines and that the company is actively printing parts for the next‑generation Raptor 4 engine. He also confirmed that Anduril Industries is a current customer and that Velo3D is working on multiple programs with them.

Being an embedded supplier for SpaceX and Anduril matters because both companies are major players in high‑growth markets. Anduril is widely expected to pursue an IPO this year, and SpaceX’s rapid product and engine iteration cycles create recurring demand for qualified additive parts. Qualification on these platforms means Velo3D is integrated into critical supply chains that extend beyond single orders.

This is the core of my thesis:

"Qualification is the moat. Once Velo3D’s platform is formally qualified for a specific part on a specific program, it stays locked in for the life of that program. Defense and aerospace programs often run for decades, and qualifying a new supplier requires restarting the entire process from scratch."

The risk is execution. The company still needs to execute cleanly over the next 18 months to prove the model works at scale and deliver sustainable profitability. The company must maintain its relationships with SpaceX and Anduril, as both companies have the potential to drive the share price significantly higher.

Not financial advice. I bought recently and am holding for the medium term.

English

$velo $crcl

고백과 결정

나: 3/25 velo 126주 진입 현재 -16퍼

와이프: 3/25 crcl 42주 진입 현재 +2퍼

하루만에 -16퍼?

더 내려와봐 임마

내려와 보라고(눈물을 흘리며)

조용한간호사@teslamania4477

$velo $crcl $poet 약간의 현금 여유가 있어서 고민된다. 뭘 살지. 기업들은 좋은데 낙폭이 좀 큰 친구들. 전문가분들 많아서 고견 부탁드립니다. 포엣은 물타기, 벨로,써클은 신규진입입니다.

한국어

장기적인 게임체인저

지금은 수주나 재료 하나만 붙어주면

스페이스x, 안두릴

훅하고 날라갈수있음

$satl 시즌2

Arun Jeldi@AJeldi2

$Velo is longterm game changer . Last year has been all about stability of the company . Turn arounds are not easy when you have to clean all the mess . Very excited and super optimistic about the growth of Velo3D.. our Vision is very clear not moved by any noise .. I’m super humbled to serve as CEO of great national treasure .

한국어