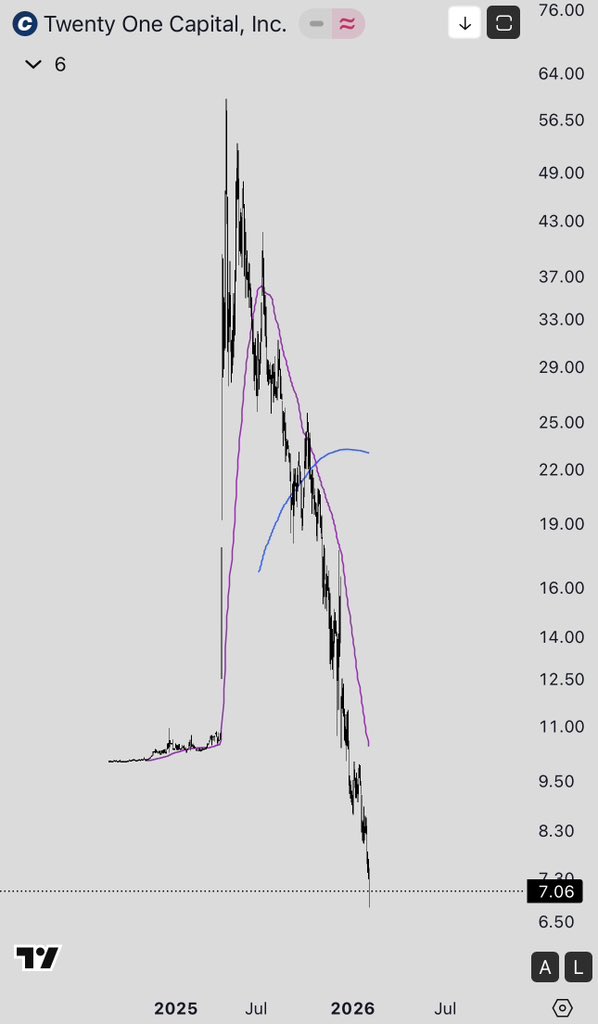

MicroStrategy is selling equity while the stock is weak to build a cash buffer. This is not a sign of strength. It is a sign of stress. Until now the model was simple: sell equity near the highs, buy BTC, wait for the rally, refinance. When the stock is strong, refinancing is trivial. When the stock is weak, refinancing becomes dangerous. A company that truly believes in an imminent bull market for its main asset does not dilute at depressed prices. It only does that when the priority shifts from “growth” to “survival”. And the fact that MSTR is doing it now, with the real risk of being removed from MSCI indices and losing billions in passive inflows, makes the message clear: they are buying time. At the same time Fundstrat publishes an outlook projecting BTC at 60k and ETH below 2000 in 2026, yet keeps pushing a permanently bullish narrative. It is a blatant contradiction, useful only for shaping sentiment and protecting their own positions. Saylor and Tom Lee represent the most toxic side of this industry. This is not analysis. It is marketing disguised as truth. They sell mandatory optimism while their models are collapsing, and the market funds them only as long as people fail to notice the gap between narrative and reality. When the cycle finally breaks, it will be clear who was building and who was manipulating. And the illusion that these figures are “visionaries” will disappear. In reality they are one of the biggest threats to BTC and ETH: they distort cycles, mislead retail investors, and manufacture artificial confidence that does not exist in the data. The market will clean this up. And it will not take long.