Cute Jia

3.5K posts

Cute Jia

@Jiaweb3

Cutie Girl Contributor at @RialoHQ @0xfairblock @ColbFinance

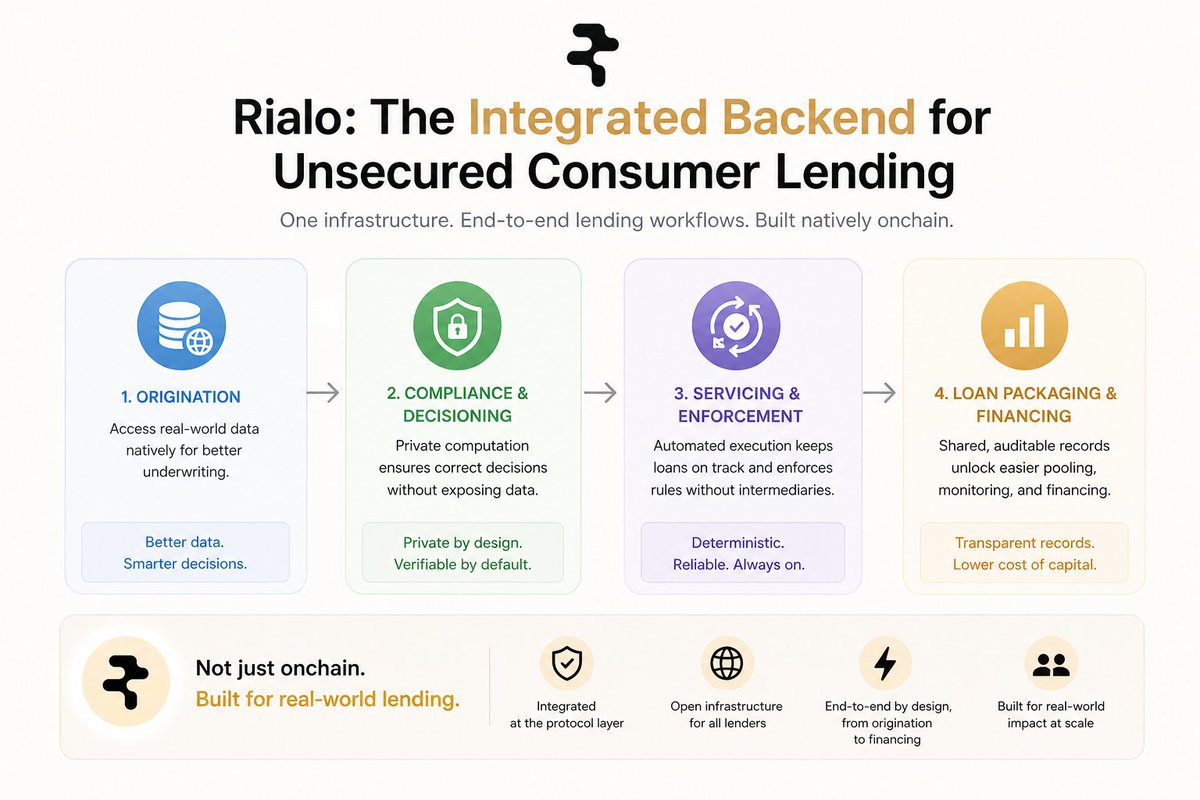

Onchain unsecured lending isn’t about reinventing lending it’s about rebuilding the infrastructure behind it A real lending system still follows the same core lifecycle: assess borrowers, verify compliance, service loans, and package them for capital. Moving this process onchain doesn’t remove these steps it changes how they are executed. The key shift is from fragmented systems to integrated execution. In traditional setups, each stage depends on separate providers, APIs, and manual coordination. That fragmentation introduces delays, costs, and inconsistencies. Onchain infrastructure, when designed properly, brings these workflows into a single programmable environment. Origination becomes data-driven and dynamic, with access to real-world inputs instead of limited onchain signals. Compliance can be enforced with verifiable logic while preserving user privacy. Loan servicing evolves into an automated state machine, where repayments, delinquencies, and defaults trigger deterministic actions without human intervention. And loan packaging benefits from transparent, auditable histories that reduce reliance on trust-based reporting. But the real value isn’t just transparency or lower fees. It’s coordination. When data access, execution, and verification live in the same system, lending stops being a patchwork of integrations and becomes a cohesive, programmable workflow. That’s what makes unsecured lending viable at scale onchain not just cheaper transactions, but better infrastructure. In the end, onchain lending isn’t about putting loans on a blockchain. It’s about building a system where every part of the lending lifecycle works together by design. @RialoHQ

Better underwriting alone won’t fix consumer lending At a glance, lending seems straightforward: evaluate a borrower, price the loan, send funds, and collect repayments. But in reality, the process spans multiple stages origination, underwriting, servicing, and loan packaging each often handled by different providers. That’s where the real problem lies: fragmentation. Even if one part improves, the rest of the system can still hold it back. A lender might upgrade its risk model, but still depend on weak servicing. A servicer might improve collections, but work with poorly originated loans. By the time loans reach investors, inefficiencies from earlier stages are already embedded in the data. So improvements don’t compound they stay isolated. This fragmentation also drives up costs. Every additional provider adds integration overhead, operational complexity, and margin. For smaller loans, these fixed costs can make entire products uneconomical, even when real demand exists. The lenders that outperform today don’t just have better models they control more of the data and the lifecycle. By integrating more of the stack, they gain a clearer, continuous view of the borrower and can make better decisions over time. But building a fully integrated system from scratch isn’t realistic for most lenders. That’s where new infrastructure comes in. Instead of stitching together fragmented services, lenders can build on integrated systems where data access, execution, and coordination are native. Blockchains, when designed this way, can act as a unified backend reducing fragmentation, lowering coordination costs, and enabling end-to-end workflows within a single environment. The shift isn’t about cheaper transactions. It’s about moving from disconnected components to integrated systems where improvements finally compound. @RialoHQ