𝕁𝕠𝕟𝕒𝕤

730 posts

@TheApexSecret The past is in the past, the market is pricing in the future.

English

@aleabitoreddit Have you seen the company report that was released early

English

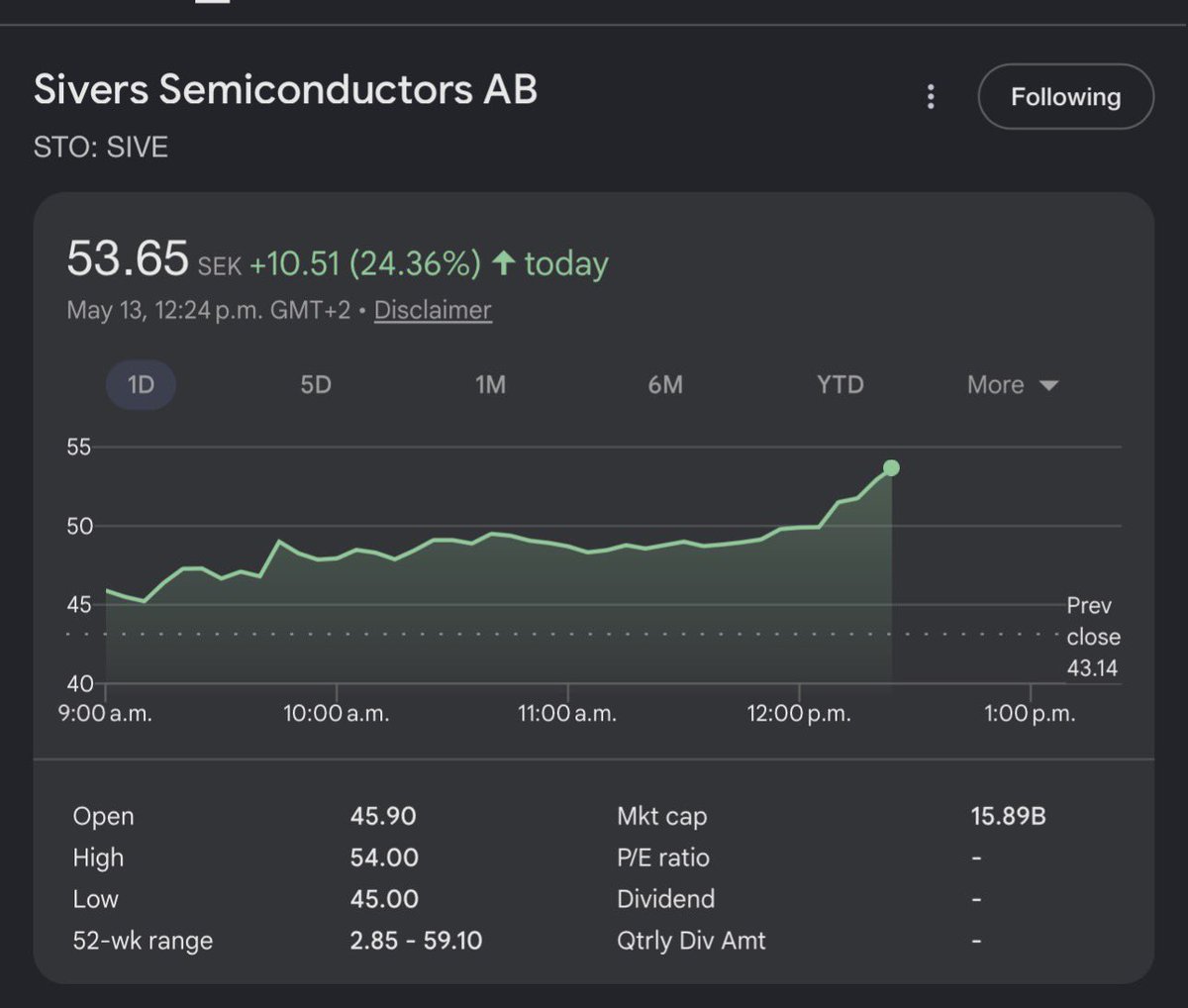

Wow, $SIVE to be listed in the MSCI Global Small Cap Index.

This is overwhelmly positively as it triggers more passive inflows as the MC grows.

Rebalancing takes places May 29th.

softcareline@user637826

@aleabitoreddit Now it’s also being listed to the MSCI Small Cap Index. Swedish article: di.se/live/kursraket…

English

@demarscrypto @aleabitoreddit Opportunities never end, but are you using margin

English

@JonasEmre7 @aleabitoreddit Bought at $119 😬 but definitely regret not buying more

English

I'm long $TSEM, the $TSM of photonics.

My top two picks for CPO are $SOI and Tower Semi.

Given the $NVDA GTC catalyst on new photonic related architecture next week:

I expect Tower Semi to get a huge catalyst.

Nvidia laready directly collaborated with Tower to scale 1.6T silicon photonics last month (hint hint for GTC), likely pushing the downstream players to use it.

And now, Tower is the leading supplier of 1.6T SiPh PICs and the primary foundry for scale-up CPO architectures. (the other being global foundries)

From my forward est:

2028 Forward P/E: ~16.8x to ~18.1x

(Tower set a target $2.84B revenue by 2028, with ~31.7% operating margin, ~$750M in net profit)

The thing to note is over 70% of their planned SiPh capacity is already reserved through 2028. And photonics haven't even ramped up yet.

So, I expect them to strongly beat earning projections due to extreme photonics scaling + allocations price hikes that's not modeled into projections.

Also, $TSEM is heavily de-risked by 70% of capacity already being reserved. MC is likely due to $TSEM being a very obscure upstream player in the photonics supply chain.

But I expect the $NVDA GTC conference to be that catalyst that brings it to premium valuations.

I'm long $TSEM as an asymmetrical upside for upstream photonics foundry layer.

English

@aleabitoreddit Stop bro I don’t have enough money to buy all this shit

English

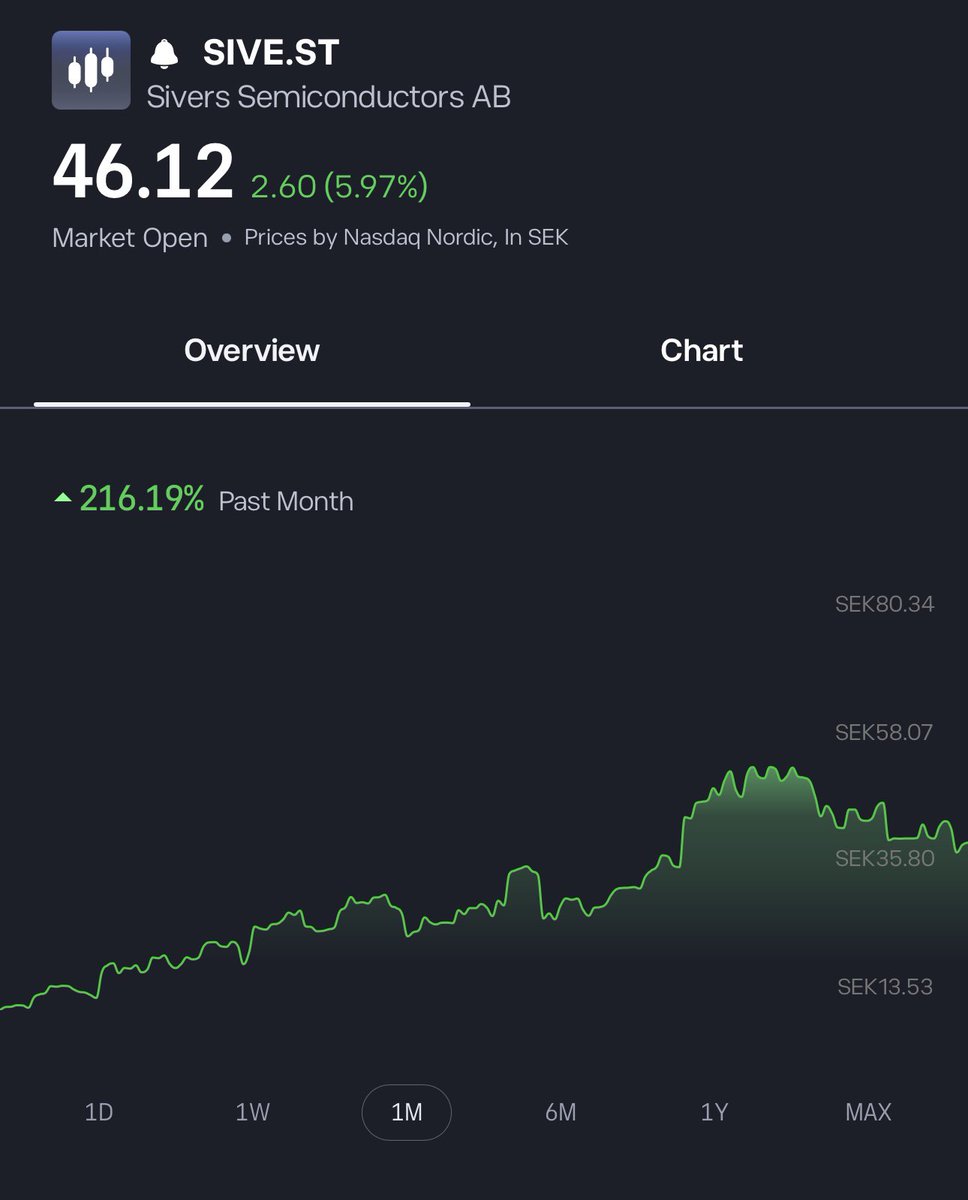

@Nektnor @Gubloinvestor Let's see how $SIVEF will perform in the US market

English

@EVSTAR8 @aleabitoreddit The Swedish Stock Exchange was open for half the day today.

English

@aleabitoreddit Think you are one of the reasons that sive gets listed in the MSCI Index lol.

English

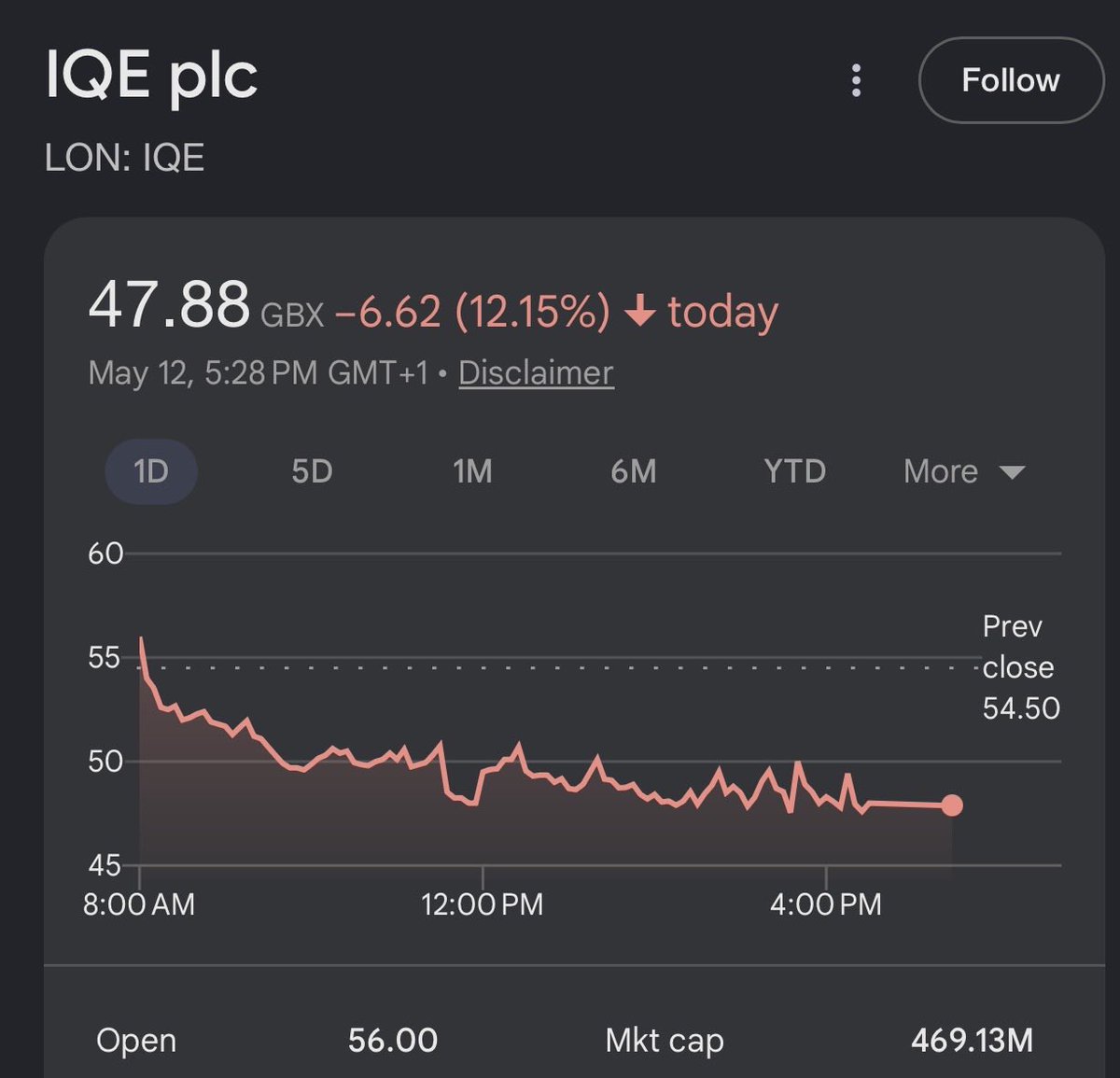

@goesrandom @aleabitoreddit It's a bad day for all semiconductor stocks; you shouldn't always expect an uninterrupted rise.

English

@aleabitoreddit Everything is trading down rn. $SIVE and $LPKF got smoken on no news.

English

$FLNC 20M share offering if you’re wondering why it’s trading down.

The 20M share is not dilution, but share unlock + transfer. So change of hands.

The biggest problem was the clause that made active shelf-registered resale capacity of the 117,666,665 shares, so there’s an unlock of the other remaining ~97m shares to my knowledge.

Net negative and very material to short term trade ideas. Since it expands the float and it introduces short term selling pressure.

That’s the overhang…

I personally cut concentration on the surprising news since it’s changes my trade idea with the float structure.

But holding some anyway to see where it heads after hyperscaler deals.

Definitely not telling people what to do, presenting new material overhang created by company management.

English

@aleabitoreddit A secondary public offering of 20 million shares was launched for $FLNC, what are your thoughts?

English

Agreed high-level directionally, $FLNC compelling at $3B valuation post-earnings after taking a closer look.

Very rare to see a US energy player that small get 2 direct Hyperscaler deals...

The $5.6B+ backlog derisks the company growth, not including new hyperscalers backlog like $GOOGL or $MSFT.

The hyperscaler deals were framework agreements, which are likely to convert "soon" Q3 this year, and aren't included in numbers.

Once that's released it's major positive catalyst, similar to qualification -> volume ramp in semi players.

Citi Analyst: "The possibility of a hyperscaler order will likely overshadow everything else in the quarter. We expect a positive reaction to the announcement"

I'm going to go ahead and guess they'll likely rerated once they announce their hyperscaler orders maybe anytime in the next 3 months so I jumped on the boat as a short term catalyst trade. (not just 1 but 2)

Also, if they hit ~$288M net income off gross-margin expansion ($6B revenue, 13.0% gross margins) from their software segment expansion, ~11.6x fwd p/e for 2027.

The current stock price is -50% Feb's prices despite hyperscalers + backlog de-risking the company looks like a great entry point to me (NFA).

KaizenInvestor@Kaizen_Investor

Just listened to the earnings call from $FLNC and decided to add to my position at $16.67. The earnings were spectacular in my opinion. Yes, they missed revenues due to a delayed shipment of $80 million, but the backlog keeps rising and Fluence management is confident they can deliver. 50% of the backlog comes from new customers and the main part of this backlog is for datacenter purposes. The datacenter backlog is around 12 GW, with the major part of this connected to 2 hyperscalers. To give you an idea, Fluence now have around 22GW deployed or contracted globally. So, this is a major deal. They announced 2 MSA's with major hyperscalers and are expecting a first order in Q3 already. They also said that they would speed up delivery for these hyperscalers and are expecting deliveries within a year. So, we should see first revenues from these deals in 2027. They also explained the heavy selection process for these hyperscalers. Apparently 26 companies were notified, but due to the difficult technical specifications most of the companies could not fit the standards. The main reason they were able to agree these MSA's was due to the fact that their technology is already proven. He spoke about the Fluence lab, so I suppose these Hyperscalers visited the lab and approved. The main focus remains on top-line growth. There were some questions about the high OPEX costs in percentage of revenues but Fluence want to control these by growing revenues instead of lowering costs. Happy to have started a stronger position here. Datacenters are looking for high quality of power to get them through the fluctuations and it looks like Fluence can provide it. Now valued at $3.4B with a $5.6B backlog, still looks pretty cheap.

English

@L9FRIENDLYSTYLE @aleabitoreddit I have no doubt about him he's just a good Korean trader who knows what he's doing man

English

For Towa (6315):

Earnings are very nuanced. I got the current ER "Beat" wrong in my original thesis (short term), my bad.

But it's an amazing structural long and setup for H2 2026 rather than H1.

TLDR: Near term bearish algorithmically since they miss the nuance, very positive H2 (markets are forward looking)

Revenue ¥54.36B (+1.7% YoY),

Net Profit at ¥4.59B (-43.4% YoY).

Operating Profit ¥6.91B (-22.1% YoY)

News headlines say "EPS crashed -43.4%" or "order miss" that might trigger an algorithmic selloff.

1. As you've seen with US Towa trading, "EPS crashing -43.4%", and algos might have sold headlines.

-> But this was due to last year, of one-off "compensation for damage" payout and one-time ¥1.3 billion yen stock sales from last year.

-> Also "increased initial costs for new customers in compression equipment." for new equipment is caused profitability losses this quarter.

So a bit of an accounting mirage, not really any profitability issues + scaling new orders, so one-off.

However:

Margin inflection point is already here. Which is the biggest signal.

Full year operating margin was 12.7%. For the annual average to reach 12.7% when Q1-Q3 was hovering around ~10%, Q4 should have been around ~18.4% or something?

Which is extremely bullish moving forward for profitability, and shows HBM compression machines are doing work, compared to legacy equipment.

2. Order book "miss":

"Acceleration expected during the second half of fiscal year 3/27 as front-end process production capacity expands."

This signals $MU, Sk Hynix, and others don't have the floor space ready yet, since they're still building front-end wafer fab lines.

But H2, is setup for massive beat. Demand visibility is there... just revenue/profit ramp deferred to H2.

_

Towa forward guidance forcasted ¥64.0B in Sales (+17.7% YoY) and ¥10.24B in Operating Profit (+48.0% YoY), which signals all time high profitability in the future.

IMO they also sandbagged revenue guidance, since they literally said acceleration second-half but didn't give much of a projection beat.

Japanese companies tend to be ultra conservative too, their dividend hike is a large signal too

Regardless, I think the US selloff was probably just due to negative accounting headlines + lower liquidity. Also I was a bit too early by like 4-6 months.

But Towa is an extremely positive setup for H2. Just not your explosive $SNDK $AAOI 10%+ a day type company.

TLDR: Long term bullish, short term lot of nuances missed with headlines.

Just need to wait a few more months if you have patience. Margins are increasing, revenue/orders deferred H2, dividend hikes, etc.

Oscar Molano@OscarReor

@aleabitoreddit @aleabitoreddit What do you think of TOWA earnings report? I'm thinking of adding a bit more today 🤔

English

@aleabitoreddit You got the boss call and deleted that post 5 mins ago huh

English

@Matrix_B0SS I thank the Swedish journalists for giving me the opportunity to buy more of this for 40 kron.

English

$SIVE move slowly because there are some Swedish journalists who are burning with this rapid fire

TopInvestor@Matrix_B0SS

Swedes selling and US buying $SIVE BUY SELL BUY SELL BUY again Then you end up having higher average Give more time to stocks and you will be surprised with laser chokepoint and CPO bottleneck $SIVE

English