Captain Kirk

42 posts

@Funmentalist You keep buying $NBIS

You also bought before at 185.00 and 195.00

Did you sell at 222.00

Or you just keep collecting.

Think you need to sell to get a profit.

Thanks.

English

$NBIS

One more little buy for $195

I just went over my assumptions and implied price targets, and I can’t help myself

Starting to make this position a generational one, either we eat on a yacht, or we will have to rebuild everything from scratch

English

@Fibonacci_TA @Fibonacci_TA

WTF you talking about.

It was down a dollar today.

La La Land maybe.

English

$ASTS - UP $3 PER SHARE CRAZY DAY

Marbella here I come.

Fibby.@Fibonacci_TA

$ASTS - I’M UP $1 PER SHARE INVESTING IS EASY

English

today we buy - $CRWV at 114.71

been on my radar for months. finally pulled the trigger.

CRWV is the cleanest AI infrastructure pure-play on this market. GPU cloud at scale. real revenue. real customer concentration with the right customers. picks and shovels for every AI workload that runs.

this is the AI infrastructure name I've been missing in the book and it's finally here.

ill add more if it breaks 120 with conviction. trim if it loses 95.

English

My guess on how things play out:

- We continue to chop around these lows for a week. Buyers who bought the top get frustrated staring at the loss and sell.

- Institutions buy big positions in AI names as weak hands are getting out from the chop

- We get a new catalyst about War "Officially" ending or something along those lines to mark the bottom. From here we see a nice +10-20% day across the board.

- Earnings report show increase in Capex spending from Amazon & Google.

- Optic earnings around the same time with solid rev ramp and increased projections because of supply/demand. Gross projections increased as well.

- We look back at this week and wish we bought more.

I could be wrong but that should be the script

English

@amitisinvesting I voted for the guy, but I’m really hating all the bullshit 😪

English

@CKCapitalxx Stop with the

Did you listen

You are not perfect

You are just annoying

English

@TW_trades_ Stupid chasers when they could have bought 2 days ago much cheaper

English

@steady_profits Ever heard of a stop when it is that high

Then buy in cheaper

Great idea????

English

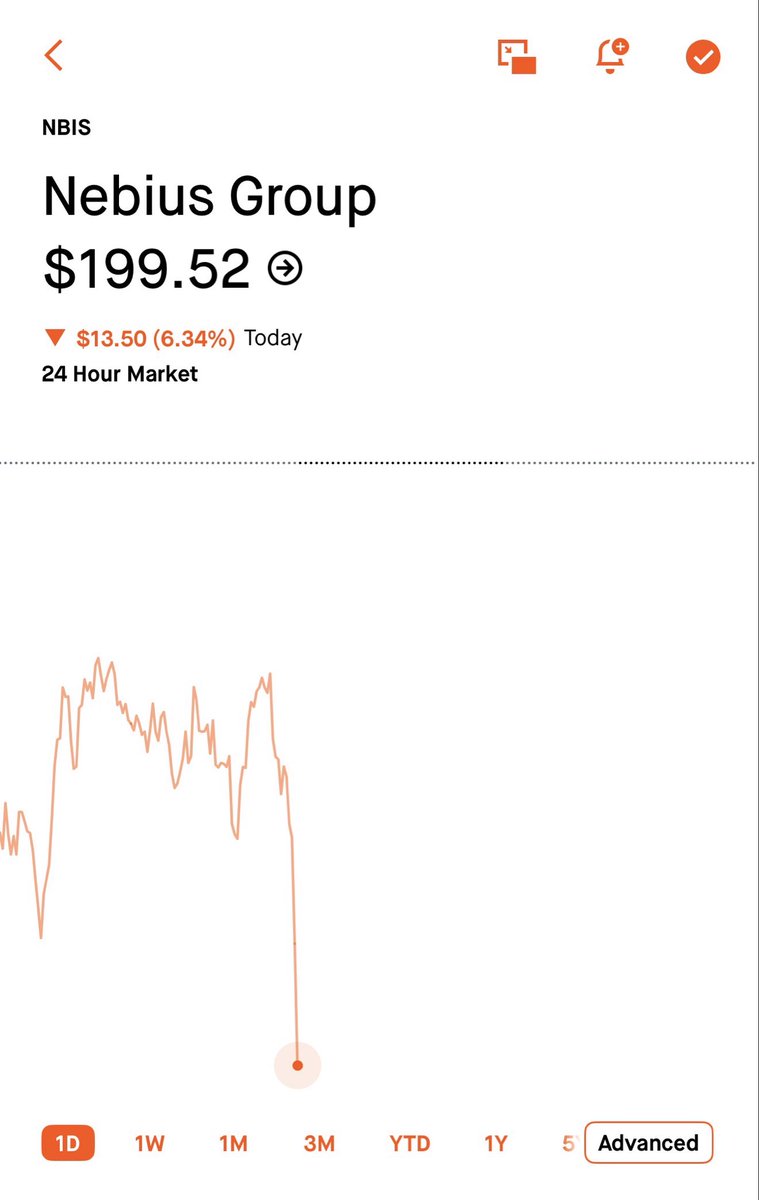

$NBIS has now dropped from a high of $287 to $203 in less than a week.

If it doesn't hold $200, I think it could easily drop into the 180s as well.

This could present a good opportunity to add to my already large holding, though, so I am trying to see the positives from this significant price drop.

The story hasn't changed at all for me. I am still very bullish about the company's long term prospects.

English

@peterli34923561 @peterli34923561

Awesome analysis.

Love it.

Keep it coming.

Thanks.

English

$CRM --- After $CRM’s stock got hammered down to the $160–$180 range, Wall Street is waking up to the brutal overcorrection in its valuation. Top sell-side firms including Guggenheim published high-profile research notes arguing the market’s hysteria over AI disrupting SaaS has spiraled into irrational territory, and Salesforce’s proprietary tech stack is irreplaceable.

The core bear fear had long centered on a simple thesis: if generative AI eliminates human agents within corporate call centers and sales teams, Salesforce’s seat-based software revenue model would collapse entirely.

CEO Marc Benioff rolled out the company’s game-changing Agentforce platform in 2026 to counter this narrative. Salesforce is formally shifting its monetization model from seat-based pricing to per-work-unit billing tied to tasks completed by AI Agents.

This effectively reframes customer spend from paying for human employee licenses to purchasing digital labor capacity. Full-scale adoption of this framework will not only prevent average revenue per customer (ARPU) from contracting but drive substantial ARPU expansion.

1. Data Is the Ultimate AI Moat — And Salesforce Owns Enterprise Core Data

Training sales, customer service and marketing AI models all hinges on years of proprietary customer relationship and transaction data accumulated inside corporate systems. Salesforce Data Cloud stands as its unrivaled competitive moat. No third-party large language model can build hyper-customized enterprise AI Agents without access to its foundational proprietary data layer.

2.Recurring Cash Cow Economics & Impenetrable Barriers

Even with revenue growth moderating to a mid-single-digit 9%–11% range, non-GAAP operating margins have climbed to nearly 34.8% amid sustained cost-cutting and operational efficiency gains. Operating cash flow is projected to approach $15 billion for 2026. Its steady recurring revenue model paired with ultra-low customer churn (driven by prohibitive switching costs) trades as a functional high-yield bond equivalent during Fed rate-cutting cycles.

3.Valuation Dislocation & Upcoming Mean Reversion

$CRM ’s forward P/E ratio has collapsed to roughly 17x. For context, this multiple sits far below the software sector’s 28x average and even undercuts the S&P 500’s aggregate earnings multiple. As the undisputed market leader in enterprise cloud CRM, the stock is now trading at a deep cigar-butts value discount with massive re-rating upside.

English

@BlackPantherCap They dont get paid otherwise.

Completely incorrect.

They can sit around for the next 5 years and get paid.

As a so called leader in trading you should have managed risk and sold in the high 60s with a profit instead of taking a bunch of unnecessary risk now and saying buy.

English

People keep saying the new $IREN pay package needed performance metrics attached to it. I don’t think that happens. They’re not rewriting the contract. This is just how it is now. It’s a time constraint, not a performance one, and the lock-up is already doing that job.

1/ Look at what the lock-up actually means. Nine million shares each, and they don’t see a dollar of it until 2031. That’s the whole trade. They can’t sell, so the only way this grant is worth anything is if the price gets there. Of course it’s in their interest the stock moves. They don’t get paid otherwise.

2/ The size of the grant makes sense too. Lock in a high share count while the price is still depressed instead of waiting until it’s $200 and needing three times the capital, or diluting the cap table harder to get the same ownership. When it does hit $150, they’ll sell some and cash out. That’s expected. That’s what a big grant at a low basis is for.

Call the whole thing FUD, because that’s what it is. People don’t have the patience for $IREN. $NBIS is converting signed contracts into delivered revenue right now. $IREN is still mid-buildout, and every capital or comp decision gets read through that lens instead of on its own terms.

3/ The patience gap exists because $NBIS posted $399 million in Q1, up 684%, AI Cloud alone up 841%, and EBITDA already positive. $IREN Q3 came in at $144.8 million against $220 million expected, a 34% miss, because they’re deliberately winding down bitcoin mining to make room for GPUs faster than AI cloud revenue is filling the gap. Nebius is proving the model right now. IREN is still mid-build. The market confirms one model and is waiting for the other, and every capital decision at $IREN gets read through the lens of transition still.

4/ Think back a moment. And compare the whole ‘FUD’ situation to $TE. They fired their CFO right before earnings. That’s a real signal, and the stock got hit for it.

$IREN hasn’t done anything like that. No violations, no major red flags, no moves that torch trust. They are STILL building and that perspective is lacking. $TE came back anyway. They dipped from $8 to $4 and ripped back to $12. $IREN will too.

5/ There’s an another thing nobody’s pricing in or considering. Everyone’s fixated on hyperscaler deals because they’re the biggest checks. But concentration in a handful of hyperscalers is its own risk. You sign 4 hyperscaler deals, 2 decide to build in-house and pull away, you’ve lost 50% of your business ‘overnight’. You sign 1-2 hyperscalers and build out 20 deals with other notable companies, and lose 3 of those, you’ve lost 3 out of 22. That’s under 14%. It’s an actual hedge I haven’t seen anyone talk about.

6/ Here’s the one thing I’d still like to see in the future, WHEN the ‘building’ part is done. I want the board to add performance triggers on future grants, not this one. When they actually need to KEEP performance steady. We are STILL building. And there’s a huge difference between building and scaling versus maintaining a business. That hasn’t happened. I’m not panic selling over it, but I’d rather have it than not.

7/ Lastly, I’m not trying to sweet talk anything here. I’ll be the first to admit I’m not satisfied with recent developments. But building a company takes longer than most people’s patience allows. Look at your own job, how many things you worried about that quietly got solved two years later while you’d already moved on to seven new complaints. That’s how the brain and ego works in its finest. It’s not the company. We’re mid-buildout. Some names here fail, some don’t. $IREN sits on 5+ GW, further ahead than 95% of their peers I could name in worse shape. I don’t expect them to be the ones that fail.

I’m taking outsized risk here. That’s not something I’d tell anyone else to copy. Added more $IREN yesterday at $38.

-BP

Not financial advice.

Black Panther Capital@BlackPantherCap

$IREN co-founders just got approved for a $1.14 billion pay package. It lands a week after a $50 million a year Warriors jersey patch deal, and four months after a $6 billion ATM that replaced the $1 billion they’d already fully tapped. The optics look like a management team spending someone else’s money. The mechanics say something different. Here’s what the package actually is: Nine million shares each, vesting in tranches through 2030. They have to hold every tranche two years before they can sell a single share. The board locked out any new grants until FY2031. Now the number that matters. Each brother owns about 3.9% of IREN today, 14 million shares. Add the new grant and they’re each sitting on roughly 23 million shares once fully vested. Combined founder ownership pushes toward 12%. That’s the same range Arkady Volozh holds at $NBIS, arguably the most founder-aligned name in this entire AI infrastructure trade. The Roberts brothers just bought themselves into that same tier. Here’s the part I’m not waving away. This grant is the third major capital and spending decision from this board in four months, after the $6 billion ATM and the Warriors deal. Stack a nine-figure equity package on aggressive share issuance and a Bay Area sponsorship splash, and you get a leadership team spending like the AI Cloud ramp is already proven, when bitcoin mining still made up the majority of last quarter’s revenue. A $1.14 billion pay packet reads like excess until you notice it’s the same bet Volozh made on Nebius: get paid in shares, get locked in for years, let the buildout do the talking. The Roberts brothers just wagered four years of their own net worth on hitting numbers they haven’t hit yet. I’m still long. But I also want the next earning to show results for the path forward. And based on recent activities and lack of PR I think @danroberts0101 owes retail some clarity. -BP Not financial advice.

English

$IREN is a $150 stock

$CRWV is a $300 stock

If a 10% pullback makes you forget a 200% opportunity,

you're focusing on the wrong number.

English

It's ridiculous neocloud is still selling off...

$NBIS, $IREN, $CRWV, and more are still taking a hit because $META is planning to sell "excess" compute capacity.

What excess? Lol

If $META had any additional capacity, they wouldn't be paying neoclouds billions for compute...

Anyway, combine that false narrative with an uncertain macro, you'll get a pretty bad overreaction from the market.

On the bright side, this makes for pretty good dips to buy across the board?

English

Send $IREN to $100 immediately, Kambiz!

IREN@IREN_Ltd

“IREN is building a differentiated full stack AI platform spanning data centers, compute and software. I’m excited to help expand the product capabilities of that platform and support our customers in deploying and managing AI workloads at scale.” - Kambiz Aghili, Chief Product Officer of IREN

English

@ohiain Also the reason $HOOD went up today is all the news from their European trading app.

Not from the charts.

English

1 of my favorite places to initiate a position isn't the breakout itself... It's the first pullback after the b/o.

That's exactly why I bought $HOOD yesterday.

The first pullback after a Stage 1 breakout is often where institutions remind you why they bought it in the first place.

$HOOD spent roughly 130 days building a Stage 1 base. That's months of price moving sideways while buyers and sellers battled for control. Eventually, buyers won + price broke above the range, volume expanded on up days, and the stock officially transitioned into what I would consider a Stage 2 uptrend.

Now the name gets my attention.

Most traders see the breakout and think they missed the move. I actually became more interested after the breakout because I know stocks don't move in a straight line forever. Healthy leaders expand, digest, and then give you another opportunity if you're patient enough to wait.

The first pullback after a Stage 1 breakout is one of the highest-probability areas I know to get involved.

But why?

Because the stock has already answered the hardest question.

It has already proven institutions are willing to accumulate shares aggressively enough to push price out of a months-long base. Now I'm simply watching to see if those same institutions are willing to defend the first test of support.

That's why I pay so much attention to the 9EMA and 21EMA combo.

Not because moving averages magically hold price... but because they tend to become areas where strong stocks naturally pause, reset, and reveal whether demand is still present.

When $HOOD started pulling back into the 9/21EMA cluster, I wasn't rushing to buy it.

I was watching it, because I wanted to see the character of the pullback.

> Was volume drying up?

> Were sellers becoming less aggressive?

> Was the stock holding tighter than the market?

> Was $HOOD showing relative strength still?

> Were buyers beginning to defend the area instead of allowing price to completely lose structure?

Those are the questions running through my head.

I'm not buying the moving average, but I'm buying the buyers, who are pushing the stock higher.

Once I start seeing buyers step back in, I immediately drop down to my execution timeframe. This is where my 15/30-minute pivots become so valuable. They allow me to react to what buyers are doing intraday.

Instead of trying to catch the exact low, I'm waiting for momentum to actually begin shifting back in my favor.

That gives me something every trader should be looking for:

1) A clearly defined risk level.

If the pivot fails, I know I'm wrong.

But if buyers continue defending the pullback, I'm positioned near the beginning of the next expansion leg.

That's what I call an asymmetric opportunity.

The strongest stocks almost always make you uncomfortable before they reward you. They rarely go straight up forever because they pull back just enough to shake out weak hands, create doubt, and make everyone wonder if the move is over.

Then they quickly reclaim support and continue higher.

That's why I love these setups so much. I'm trying to identify where institutions are likely defending the trend.

Will every first pullback work? Of course not.

Some will stop me out, and some will need another week or two of tightening. Some will undercut the moving averages before reclaiming them... but that's just part of trading.

But after years of studying leaders and countless others, this behavior keeps showing up over and over again.

- Large base.

- Strong breakout.

- Healthy digestion.

- First pullback into the 9/21EMAs.

- Buyers step in.

- Momentum returns.

It's a pattern I've built a tremendous amount of confidence in because I've seen it repeat across so many different leaders and market cycles.

At the end of the day, my goal is 2 position myself where the trend has already proven itself, buyers are beginning to take back control, my risk is clearly defined, and the upside is still heavily skewed in my favor.

That's exactly what I saw in $HOOD.

And that's exactly the type of opportunity I'll continue looking for as long as the market keeps giving it to me.

Chart: $HOOD.

iain@ohiain

"How long do you usually hold your trades?" My answer is always the same: It depends on what the stock is actually trying to do. I don't go into a trade saying, "I'm holding this for 3 days," or "I'm swinging this for 1 month." The chart usually tells me that long before I ever enter. For example, if I'm buying a stock that's already been trending higher and is simply breaking out of a short-term continuation pattern, I'm usually expecting a relatively quick move. Maybe it's been consolidating for 1 week, volatility has tightened, and buyers are stepping back in. Those are often the types of trades I'm looking to hold for 3-5 days because momentum names don't move vertically forever. Stocks expand, they rest, they expand again. If I get the expansion I was looking for, I'm perfectly happy taking partials and managing risk. On the other hand, if I'm buying a stock coming out of a large Stage 1 base that's been building for 5-10 weeks, my mindset is completely different. Especially if the overall market is coming off a healthy correction and leadership is just beginning to strengthen. Those are the situations where I'm willing to think in terms of weeks instead of days because I know the bigger the base, the bigger the potential move! That's why you'll sometimes see me hold names (ex, $ARM) for months while another position only lasts 3-4 days. In a sense... the setup determines the expectation. I believe every pattern has its own personality. A 5-day flag shouldn't be managed the same way as a 6-month Stage 1 base breakout. They represent completely different phases of a stock's lifecycle, so it makes sense that my holding period changes too. This is also something that's incredibly difficult to teach because it mostly comes from experience. The more leaders you study, the more you begin to develop an intuition for how different structures tend to behave. Eventually, you stop asking, "How long should I hold this?" and start asking, "What is this pattern likely capable of?" That subtle realization changed the way I manage almost every trade. Instead of forcing every position into the same holding period, I simply let the structure, the market environment, and the stock's behavior dictate my expectations. The longer I trade, the more I realize that holding time is a reflection of the opportunity the chart is presenting. My 2 cents!

English

@BlackPantherCap You joining the BB team.

Better to take profits and put it somewhere else.

English

I’ve been holding $IREN since August 2025. Entered at $19. Accumulated since.

My average is now around $32.

I can’t wait for $IREN to be above $100, EOY.

So much FUD against $IREN. No patience around it. Can’t wait for it to play out.

And if it doesn’t play out I’ll gladly be the first to admit I was wrong.

-BP

Not financial advice.

English