Audit The Herd@AuditTheHerd

With respect to the $HIMS community, I've been following the company for years, longer than a lot of folks here (see below for proof).

A few big decisions over the past year have raised real red flags for me, especially the Novo Nordisk partnership blowing up so quickly and the ongoing reliance on compounding GLP-1s.

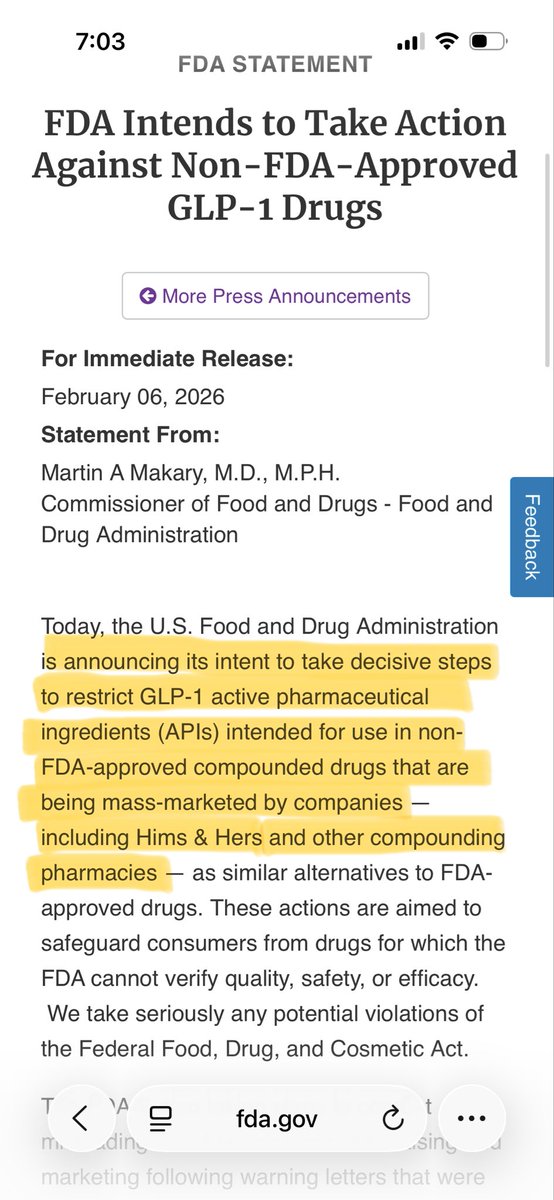

The Novo deal was announced in April 2025 as this big credibility win, branded Wegovy on the platform, better access, all that. Then just two months later in June, Novo pulled the plug, accusing Hims of illegal mass compounding (calling compounded versions "knockoffs" under the personalization label), deceptive marketing, and putting patient safety at risk with potentially sketchy ingredients. Hims obviously fought back, saying Novo was just trying to lock patients into branded stuff and limit clinician choices. Either way, a lot of trust was lost for me then,

On top of that, the FDA had already ended the semaglutide shortage earlier in 2025 (around Feb), which basically took away the main legal cover for large scale compounding. Hims kept pushing personalized doses and formulations, but that invited more regulatory heat, potential lawsuits, and tougher competition once branded supply caught up.

Beyond the GLP-1 mess, there are other execution concerns piling up:

- The push into peptides (with the California facility acquisition back in Feb 2025 and talk of longevity offerings rolling out in) but there's still a real lack of clarity on what exactly they'll offer, how regulated/safe it'll be post FDA scrutiny on compounding, and when we'll see meaningful revenue from it.

- The lab testing expansion (Labs launch in late 2025, plus acquisitions like Trybe Labs and the recent YourBio deal ) shows early feedback with rollout issues that point to blood testing being slower than expected, delays in results, appointment wait times at partner sites like Quest, and questions about scaling at home draws without contamination risks. It's promising for personalization, but execution has felt clunky so far.

- And overall, the string of acquisitions (peptide facility, at home lab stuff, ZAVA for Europe, YourBio just recently) is aggressive, but it starts to look like spreading too thin without enough concentration. Each one adds complexity, integration risks, and capital burn in the near term, while core areas like subscriber retention and weight loss margins are still under pressure.

These are real issues….lost pharma credibility, questions about how sustainable the compounding/peptides model is long term, margin pressure from personalization efforts, execution hiccups in new verticals, and a lot of uncertainty hanging over the obesity/longevity verticals that drove so much of the recent hype.

The conversation around $HIMS has gotten pretty one sided in a lot of places. It's turned into this super bullish echo chamber where balanced takes or legit concerns get shouted down fast.

I'm not here to bash the company. I might end up buying back in at some point. I just think we need more straight talk about the risks alongside the upside.

I see way too many $100+ and $0 PTs on here. A little bit of balance is needed.

I will always audit the herd, even if im in that herd.