Sabitlenmiş Tweet

™Kevin L. Walker©

19.8K posts

™Kevin L. Walker©

@KevinLWalker_

A family man & entrepreneur — grounded in honesty, truth, and facts. 🥷📕🧠 Founder of https://t.co/oYS13dgvzJ — https://t.co/bTYYCAtf47

Katılım Haziran 2009

6 Takip Edilen48.4K Takipçiler

English

How to Remove Collection Accounts Using the FCRA and FDCPA: A Compliance-Driven Framework Based on Verification, Documentation, and Legal Obligation

Collection accounts are among the most damaging items on a credit profile. However, they are also among the most vulnerable to removal when challenged correctly — not because collections are inherently invalid, but because the modern debt collection system is built on bulk data transfers, incomplete documentation, and fragmented ownership records.

Facebook: facebook.com/share/p/1CJbqR…

Kevinomics LINK: kevinomics.com/2026/04/14/how…

#credit #money #finance #FCRA #FDCPA #kevinomics #education

English

Why Your Credit Score Alone Doesn’t Matter: The Reality of Credit Profile Risk, Underwriting, and Approval Decisions

Most people are conditioned to believe that their credit score is the primary factor in determining approvals, limits, and financial opportunity. That belief is incomplete. In reality..

Facebook: facebook.com/share/p/1LX3Lz…

FULL ARTICLE -- Kevinomics.com (Kevinomics ) LINK: kevinomics.com/2026/04/14/why…

#credit #money #wealth #education #finance #tips #kevinomics

English

Authorized Users & Credit Profiles Legitimacy, Impact, and Limitations — What they actually do, what they don't, and how to use them correctly.

Adding authorized user tradelines is one of the most widely used strategies in credit building. It is legal, recognized, and utilized by lenders and scoring models. However, while it can be effective in certain situations, it is often misunderstood — especially when applied to credit profiles with significant negative history.

Kevinomics LINK: kevinomics.com/2026/04/14/aut…

Facebook: facebook.com/share/p/17uY1f…

#education #credit #wealth #kevinomics #money #finance

English

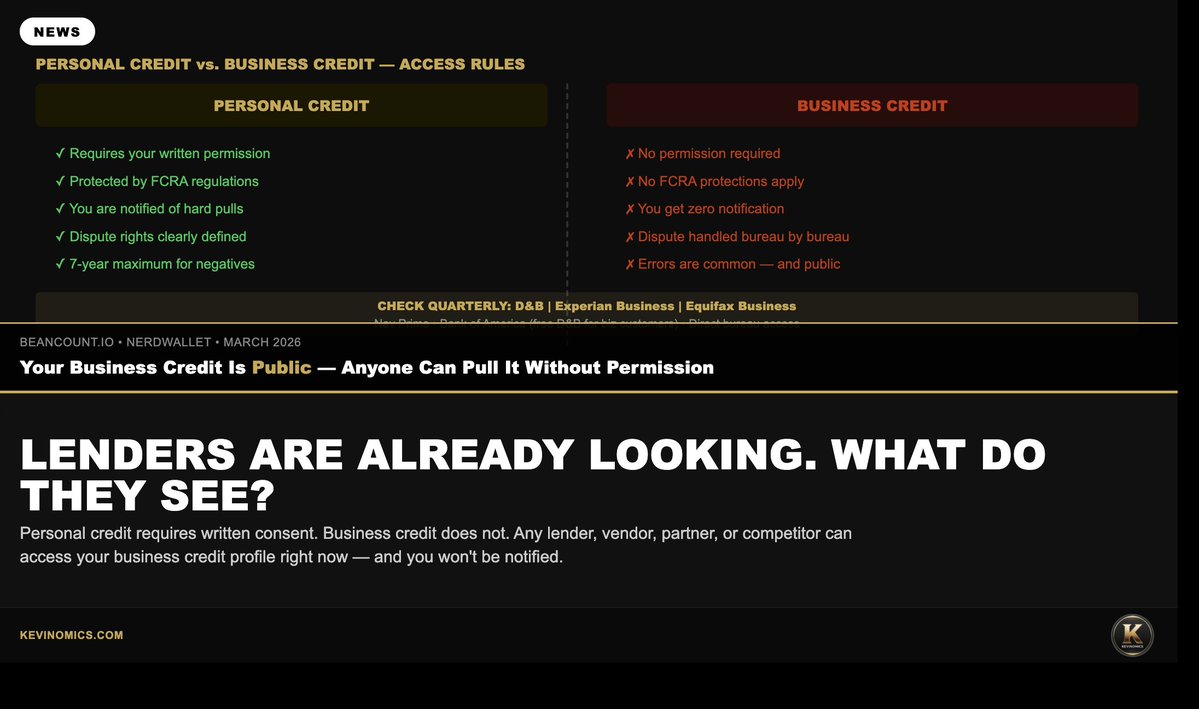

Your Business Credit Report Is Public. Anyone Can Pull It Right Now.

A Fact Most Business Owners Do Not Know:

Your personal credit report is protected. A lender needs your written permission to pull it. Your business credit report is not. Any lender, vendor, supplier, potential partner, or competitor can access your business credit profile right now without your knowledge and without your consent. It is public information by design.

Most small business owners have never thought about what is on that report. They have never looked at it, never verified it, and have no idea what a bank or vendor sees when they look up their company before a deal.

Kevinomics.com LINK: kevinomics.com/2026/04/10/you…

Facebook: facebook.com/share/p/1Nxfeu…

English

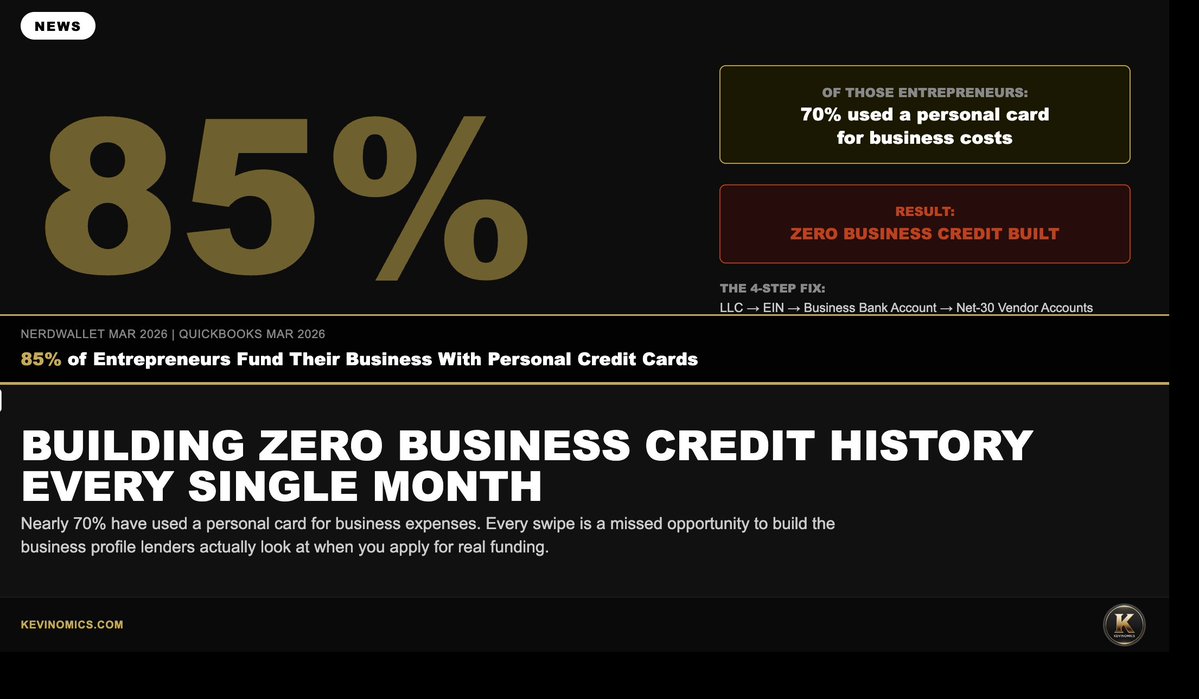

85% of Entrepreneurs Use Personal Credit Cards for Business. Here's Why That's a Problem.

The Statistic That Should Concern You

85% of entrepreneurs use credit cards to fund their businesses. Nearly 70% have used a personal card for business expenses at some point. Most of them are doing it because it is the path of least resistance — the personal card is already in their wallet, and nobody told them there was a better way.

The problem is not the spending. The problem is that running business expenses through a personal card means you are building zero business credit history while putting pressure on your personal credit profile at the same time. When you go to apply for a real business loan, you look like a business that does not exist.

Kevinomics.com LINK: kevinomics.com/2026/04/10/85-…

Facebook: facebook.com/share/p/1PGA8W…

English

A 100-Point Credit Score Difference Is Worth $7,000 on a Single Loan

The Number Has a Dollar Amount Attached to It:

Most people know a higher credit score is better. Very few people know exactly what a lower score is costing them in real dollars. A 100-point difference in your personal FICO score can mean the difference between a 7% and a 12% interest rate on a $50,000 loan. Over five years, that is $7,000 in extra interest on a single loan. Reinvested into your business, $7,000 is a marketing campaign, a software buildout, or three months of operating capital.

And that is one loan. Stack a mortgage, a vehicle, a business line of credit, and insurance premiums — all of which are priced using your credit score — and the annual cost of a low score can easily exceed $10,000 to $20,000 per year in above-market rates.

Kevinomics.com LINK: kevinomics.com/2026/04/09/a-1…

Facebook: facebook.com/share/p/1HsePm…

English

Your Business Has a Credit Score. You've Probably Never Seen It.

The Credit Profile Nobody Told You Existed:

A business has its own credit profile — completely separate from your personal FICO score — tracked by three separate bureaus: Dun & Bradstreet, Experian Business, and Equifax Business. Banks, lenders, vendors, suppliers, and potential partners check these profiles before they extend terms, approve financing, or decide whether to do business with you.

Most small business owners have never looked at any of them. Some do not know they exist.

Kevinomics.com LINK: kevinomics.com/2026/04/09/you…

Facebook: facebook.com/share/p/18YJAK…

English

Your Business Is Destroying Your Personal Credit Score Right Now

Most small business owners are using personal credit cards to fund their business. That means every charge — every supplier order, software subscription, equipment purchase — spikes their personal credit utilization. A high utilization ratio drops your FICO score, even if you pay the balance in full every single month.

Kevinomics.com LINK: kevinomics.com/2026/04/09/you…

Facebook: facebook.com/share/p/1B8gB4…

English

OpenAI Is Going Public. The Window on Private AI Is Closing

OpenAI is on track for an IPO as early as Q4 2026. CEO Sam Altman and CFO Sarah Friar are reportedly confident in the timeline following the company's $122 billion fundraise. Once it goes public, the early-stage narrative ends permanently. The pre-IPO window — where upside is asymmetric and access is limited — doesn't survive a public listinga

@Plopjoy Link: plopjoy.com/2026/04/09/ope…

Facebook: facebook.com/share/p/1TJWFh…

English

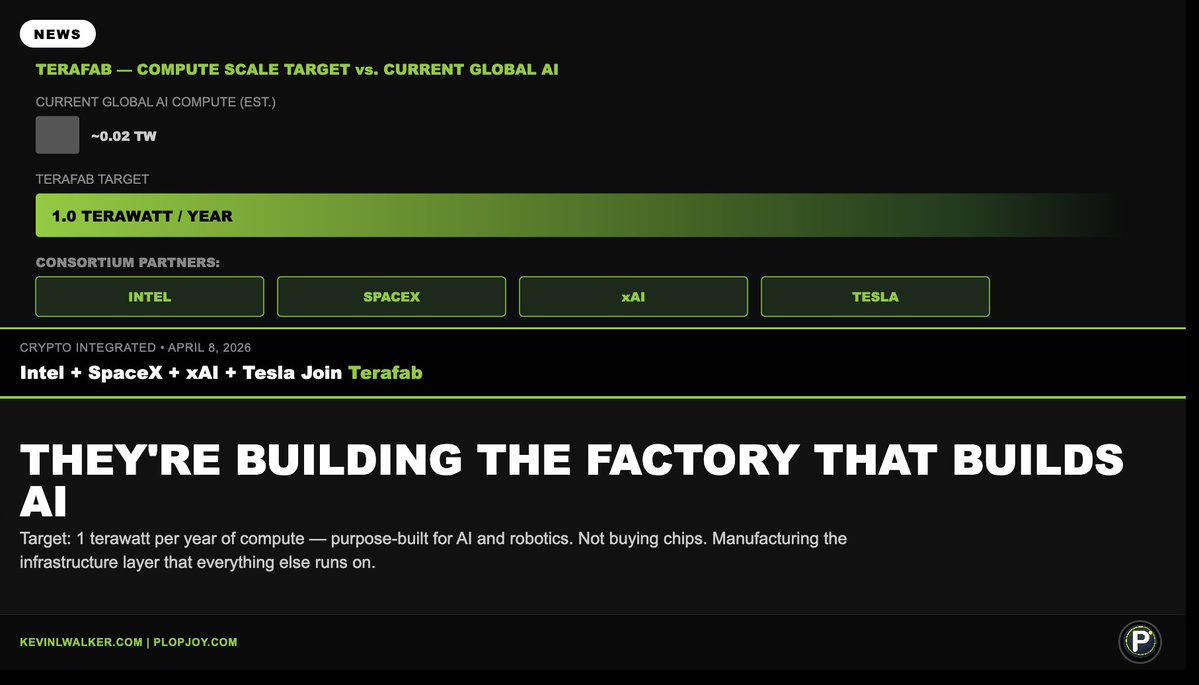

Intel, SpaceX, xAI, and Tesla Are Building the Factory That Builds AI

Intel officially joined Terafab — a chip fabrication initiative alongside SpaceX, xAI, and Tesla — to build a facility targeting 1 terawatt per year of compute. Purpose-built for AI and robotics at a scale that doesn't exist anywhere else on the planet. This isn't an incremental upgrade. It's a new category of infrastructure entirely.

@Plopjoy Link: plopjoy.com/2026/04/09/int…

Facebook: facebook.com/share/p/1GzeU7…

English

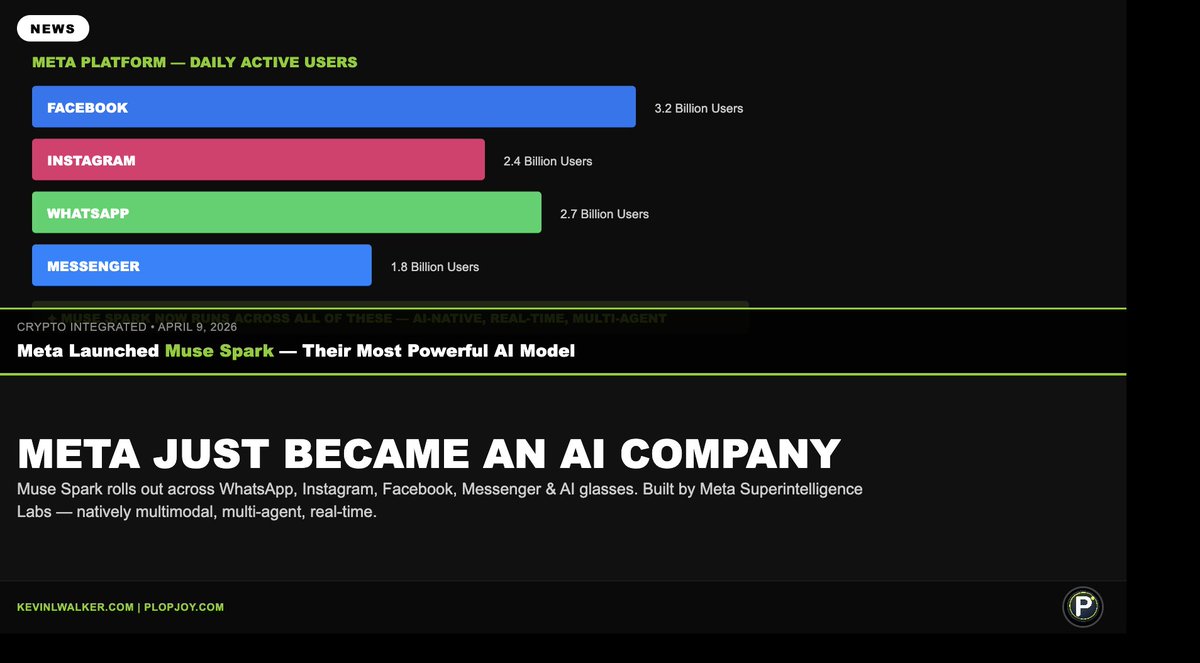

Meta Just Became an AI Company — Not a Social Media Company

Meta launched Muse Spark — their most powerful AI model to date. It's rolling out across WhatsApp, Instagram, Facebook, Messenger, and Meta AI glasses over the coming weeks. Built by Meta Superintelligence Labs, Muse Spark is natively multimodal — it can see, reason, use tools, and coordinate with other AI agents in real time.

@plopjoy Link: plopjoy.com/2026/04/09/met…

Facebook: facebook.com/share/p/1GwQuA…

English

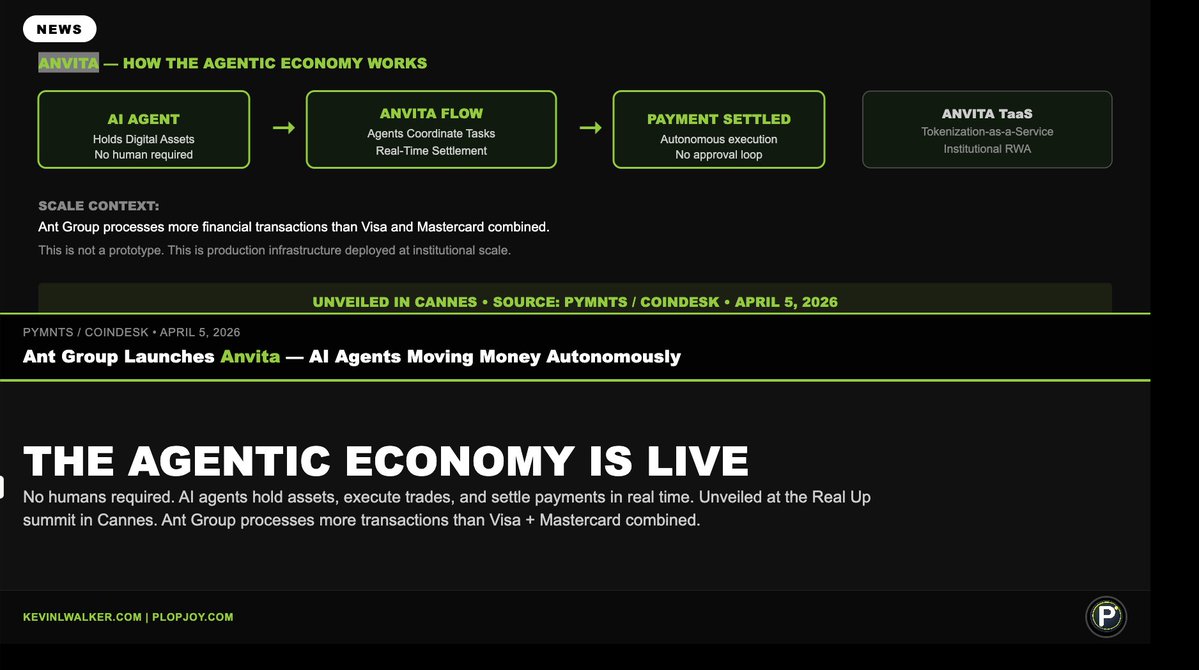

AI Agents Are Now Moving Money Without Humans. This Is Not a Test.

Ant Group — China's largest fintech conglomerate — unveiled Anvita at their Real Up summit in Cannes. Anvita is a platform that lets AI agents autonomously hold assets, execute trades, and settle payments in real time with little to no human involvement required at any point in the process.

@plopjoy Link: plopjoy.com/2026/04/09/ai-…

Facebook: facebook.com/share/p/14YaHS…

English

. @DonnabellaWalke launches 'Emotional Range Training' — a curriculum built from two decades of professional performance, not theory.

Link to Article: donnabellamortel.com/2026/04/03/don…

Facebook: facebook.com/share/p/17NPrf…

#acting #hollywood #emotion #training #Texas #California #emotionalrangetraining

English

I’ve built $3M+ across 8 industries.

Every single time — the businesses that won were the ones with the right infrastructure in place.

Not the best marketing.

Not the biggest budget.

The right systems.

That’s what @plopjoy builds.

Websites that rank. AI that answers every call. Systems that follow up automatically. Infrastructure that works while you sleep.

We just dropped our first brand video and I’m proud of how it came out.

If your business is serious about growth — this is what we do.

🔗 plopjoy.com

FB: facebook.com/share/v/1CdJWL…

IG: instagram.com/p/DWf4SF-CJlo/

#Plopjoy #aiagency #Entrepreneur #plopjoy #business #california #business #money

English

Not 100% accurate. Certain protocols cannot be frozen, and many are decentralized to a large degree… KYC only comes from the off ramps and no “cold storage” wallet.

Yes, gatekeepers (off ramps) can hinder but there are always cash out options. The opportunity to grow your wealth is exponential.

I agree there are issues but calling crypto entire a bad thing isn’t accurate in my opinion.. been in crypto since 2013.

English

Why Modern Cryptocurrency Is a Controlled-System, Not Liberation

Cryptocurrency today is marketed as freedom: decentralized, autonomous, permissionless, outside government reach, and immune to traditional financial controls. This narrative functions as a loss-leader — a bait device to attract people into a system that feels liberating on the surface but becomes increasingly controlled the moment it interacts with the real world.

As soon as crypto touches a verification node — exchanges, banks, payment processors, custodial wallets, or compliance gateways — every promise of decentralization collapses. These nodes enforce KYC, AML, behavioral scoring, transaction monitoring, blacklisting, asset freezing, and reversal authority. In practice, this creates a fully permissioned financial cage, hidden beneath the language of decentralization.

The end goal is not autonomy — it is total visibility and total control.

Under a centralized crypto regime:

Access to your own money can be restricted or terminated

Purchases can be approved or denied based on algorithms

Wallets can be frozen

Transfers can be reversed

Spending behavior can be categorized and scored

“Risky” individuals can be cut out of the system entirely

Compliance policies can dictate who may participate in the economy

This is not financial freedom — it is programmable finance, run by gatekeepers who decide what is allowed.

The narrative of decentralization is used to gain adoption because people would never knowingly submit to a system of programmable control, asset surveillance, and conditional access. Once users are fully onboarded, and economies digitized, those same systems can be tightened, monitored, and enforced without resistance — because everything becomes digital, traceable, and revocable.

The illusion of freedom primes people to voluntarily enter the very system that can later restrict, limit, or erase their economic existence with a single policy change.

Cryptocurrency, as structured by modern corporate and governmental frameworks, is not the end of financial bondage — it is the next evolution of it, marketed as liberation while quietly laying the infrastructure for precision control over every transaction, every purchase, and every individual’s economic life.

English