EndGame Macro@onechancefreedm

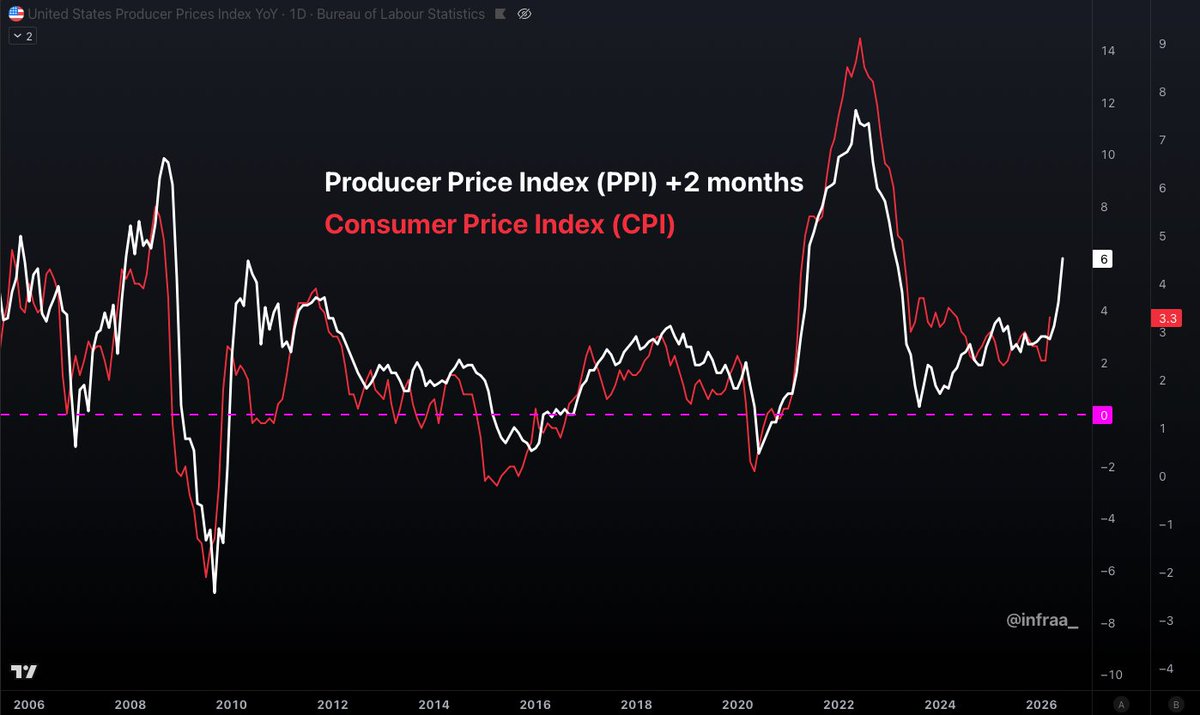

The PPI Report Is Warning About Inflation Now And Recession Later

The April Producer Price Index was not just hot.

It was structurally ugly.

Final demand PPI rose 1.4% in April, the biggest monthly increase since March 2022. On a yearly basis, producer prices rose 6.0%, the fastest pace since December 2022. That alone is bad enough, but the real warning is underneath the headline.

This was not one isolated category.

It was energy, freight, services, trade margins, processed goods, unprocessed goods, and intermediate inputs all moving together.

The Inflation Pipeline Is Reopening

Final demand goods rose 2.0%. Final demand services rose 1.2%. Energy jumped 7.8%. Gasoline rose 15.6%. Transportation and warehousing services rose 5.0%. Truck transportation of freight rose 8.1%.

That is the key.

Energy does not stay in energy.

Diesel hits trucking. Trucking hits food distribution. Freight hits retail. Retailers and wholesalers protect margins. Then the pressure shows up later in consumer prices.

The so called cleaner measure was not comforting either. Final demand less food, energy, and trade services still rose 0.6% in April and 4.4% from last year. That means even after stripping out the usual volatile categories, the underlying producer side pressure is still too hot.

The Scary Part Is Intermediate Demand

The real danger is not just final demand.

It is the pipeline.

Processed goods for intermediate demand rose 2.7%, the sixth straight increase. Unprocessed goods rose 4.1%, also the sixth straight increase. Intermediate services rose 1.1%, the largest monthly increase since March 2022.

That means businesses are not just seeing higher prices at the final point of sale. They are being hit earlier in the production chain.

Stage 2 intermediate demand rose 2.8% in April and 11.1% from last year. Stage 3 rose 2.3%. Stage 1 rose 2.1%. Stage 4 rose 0.9%.

The upstream system is lighting up.

That matters because today’s intermediate cost pressure can become tomorrow’s consumer inflation, or tomorrow’s margin compression.

Either outcome is bad.

The Corporate Margin Trap

This is where the report becomes more than an inflation story.

If businesses have pricing power, they pass these costs forward and CPI stays hot.

If businesses do not have pricing power, they eat the costs, margins compress, earnings weaken, hiring slows, and recession risk rises.

That is the late cycle trap.

Producer costs are rising at the same time consumers are already getting squeezed. Real wages are under pressure. Credit is tightening. Housing is frozen. Small businesses are stressed. Delinquencies are rising. The consumer is paying more for necessities and cutting back on discretionary spending.

So this is not healthy demand inflation.

It is cost pressure colliding with weakening demand.

What This Means For The Fed

The Fed is stuck.

If it cuts too soon, markets may fear inflation is not under control.

If it stays tight too long, higher input costs, higher freight costs, higher energy costs, and weaker real wages can turn the inflation shock into demand destruction.

That is why this PPI report matters.

It gives the Fed an inflation problem on paper.

But it gives the real economy a recession problem underneath.

My Take

This report is not saying the economy is booming.

It is saying the cost structure of the economy is getting squeezed again.

The most important takeaway is simple.

Inflation is reaccelerating at the producer level while the consumer is losing the ability to absorb it.

That creates two paths.

• Higher CPI if companies pass costs through

• Lower margins, weaker earnings, and layoffs if they cannot

This is why the April PPI report is so dangerous.

It is not just inflation now.

It is recession risk later.